DXY continued its recovery Friday night as EUR sank:

The Australian dollar was soft against the USD:

Weak against EMs:

Gold tried but failed:

Oil lifted as the US rig count tumbled:

Metals were mixed:

Big miners were firm:

EM stocks too:

And US junk, EM not so much:

All bonds eased:

As stocks galloped to within inches of a record high:

Westpac has the wrap:

Event Wrap

US negotiators said that US-China talks have progressed very well and suggested that a deal was close. Treasury Secretary Mnuchin and USTR Lighthizer spoke with with China’s VP Liu He on Friday, and the statement from the U.S. side said “They made headway on specific issues and the two sides are close to finalizing some sections of the agreement. Discussions will go on continuously at the deputy level, and the principals will have another call in the near future.” Trump called for Congress to pass the USCMA (US-Canada-Mexico) trade pact and said that China wants a trade deal.

US Univ. Michigan consumer sentiment was finalised at 95.5, marginally below its preliminary release of 96.0, but confirmed the rise seen since August’s sub 90 print.

Germany’s IFO sentiment survey was close to estimates with a minor rise to 94.6 due to slightly better, though still weak, expectations of 91.5 (est. 91.0).

Brexit: EU deferred on providing a new Brexit deadline date until Monday or even Tuesday. Although the majority agreed to 31st Jan, France apparently wanted to impose an earlier 30th Nov. end date.

Event Outlook

NZ: Observes a national holiday for Labour Day.

Europe: Sep lending data is released.

US: Oct Dallas Fed index will be of interest ahead of the ISM manufacturing survey on Friday.

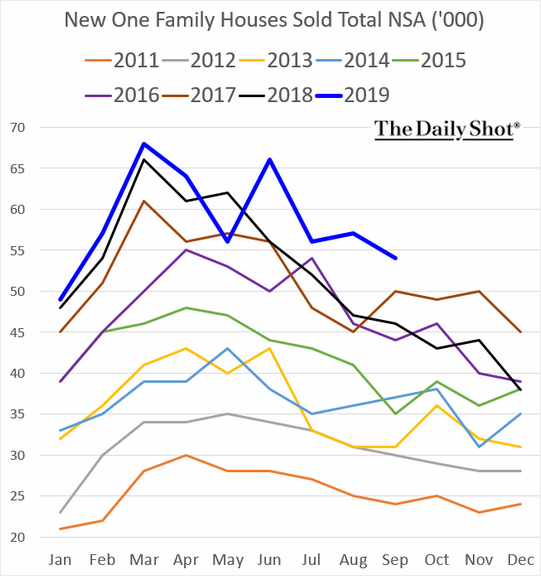

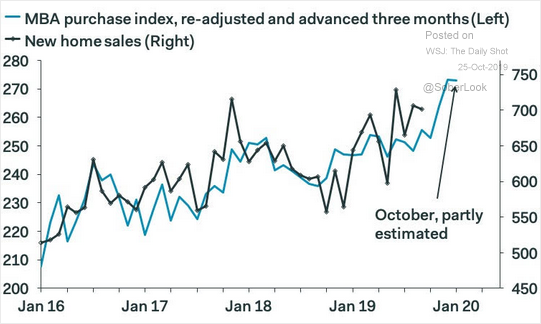

So, there the US has slowed but is still not in danger of recession. There is one chart from Calculated Risk that shows what’s missing for substantial downturn, a bust correction:

We are currently going the other way:

With more to come:

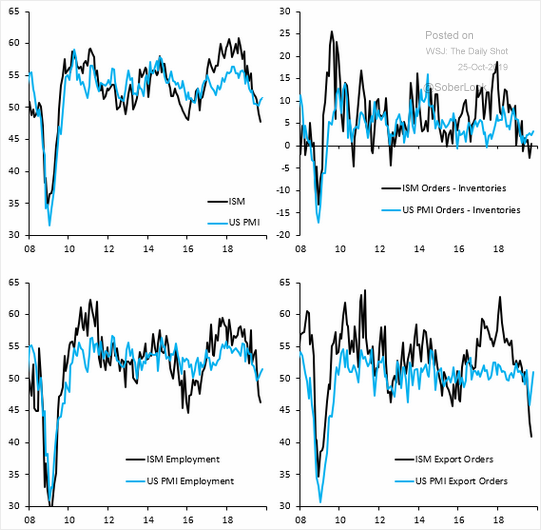

Which is already supporting regional manufacturing:

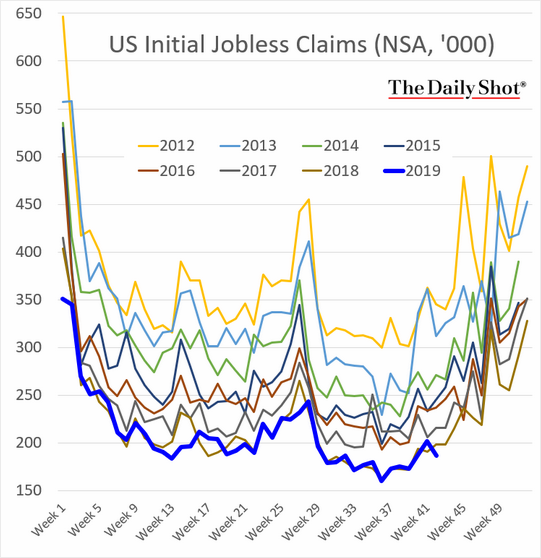

And jobs:

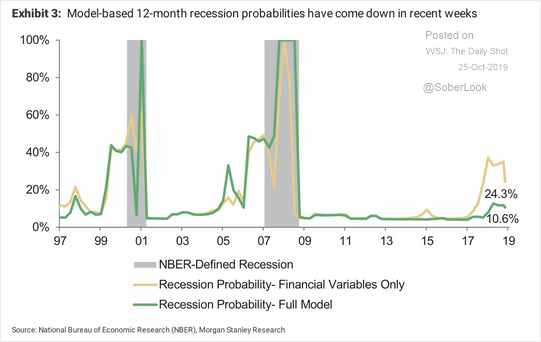

As recession fears fall away:

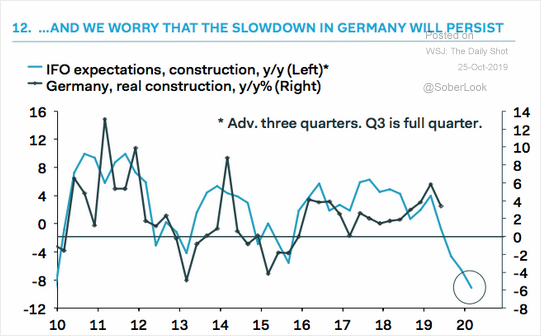

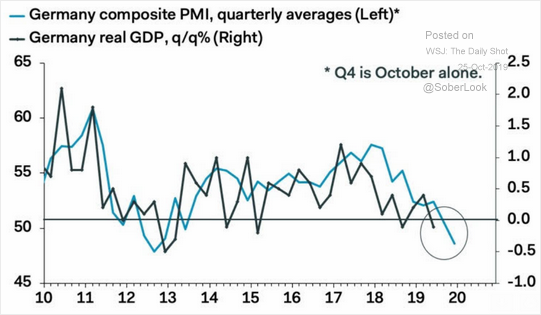

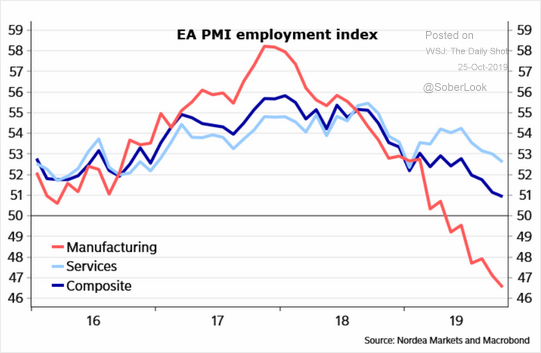

On the other hand, we do see the pre-requisite construction downturn needed to trigger recession unfolding in the Eurozone:

With growth to follow:

And employment:

The building blocks of the USD are improving while they still cracking in the EUR.

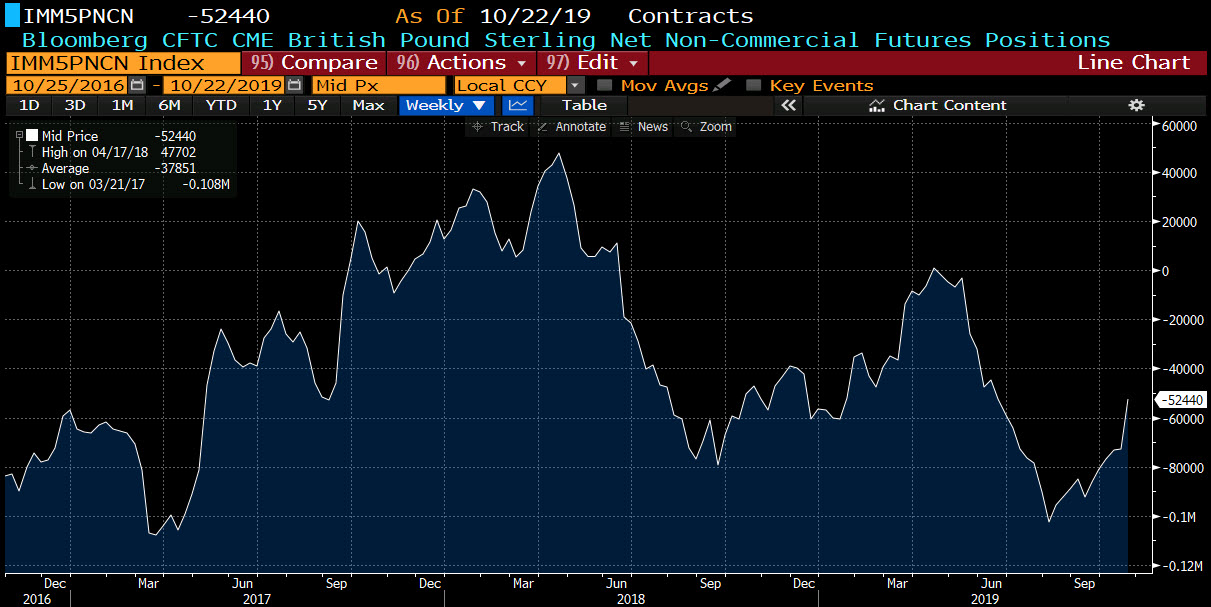

Trade non-deals have lifted hopes for improving global growth which always sinks the USD and lifts the EUR. In turn, that has lifted the very large EUR short:

But, for me, this is just another chance to get long USD and short EUR given the trade resolutions are so thin that any positive multipliers from US strength will not emanate outwards.

That means an ongoing very strong headwind for the AUD.