DXY fell last night as EUR bounced. CNY is closed:

The Australian dollar rebounded against DMs:

Not so much against EMs:

Advertisement

Gold firmed:

Oil fell:

Copper too:

Advertisement

Big miners edged up:

EM stocks too:

Junk did better:

Advertisement

Treasuries were golden:

And bunds:

Plus Aussie bonds:

Advertisement

Stocks bounced:

Westpac has the wrap:

Event Wrap

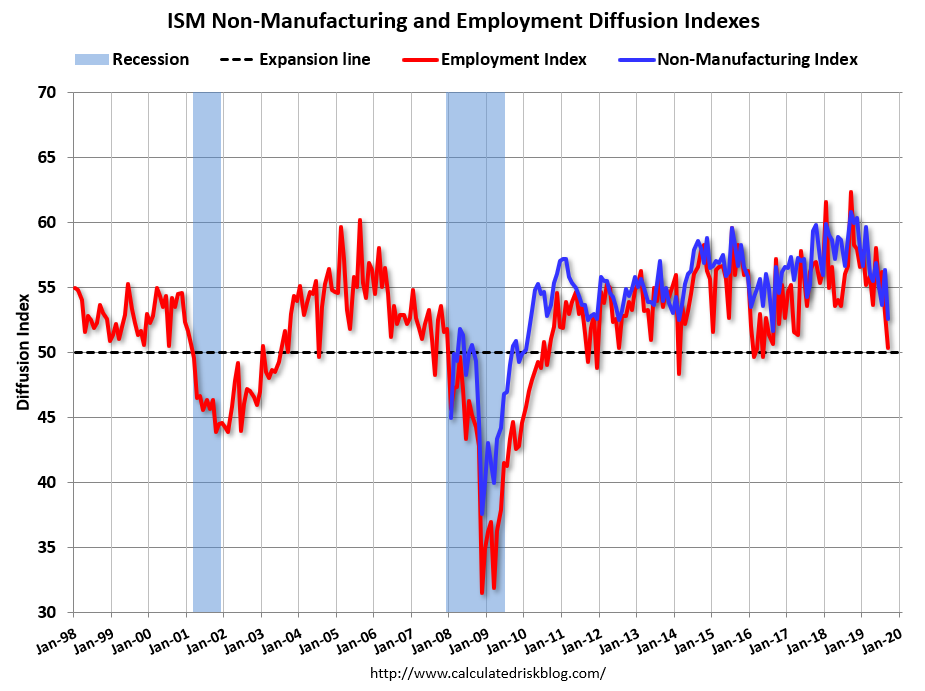

Following the disappointing US ISM manufacturing survey released yesterday, services ISM fell to 52.6 (est. 55.0, prior 56.4) – a three year low – with notable slippage in employment (50.4, prior 53.1), new orders (53.7, prior 60.3) and business activity 55.2, prior 61.5). Trade tariffs were frequently cited by respondents as adding to uncertainty and affecting demand.

FOMC member Evans said that ISM survey weakness was a concern and that one of the main risks to the economy was a struggling manufacturing sector, adding that the Fed would be closely watching Friday’s labour data.

Eurozone final composite PMI was marked down to 50.1 from the flash release (50.4, Aug. 51.9) due to deeper deterioration in service PMIs across the region. Weakness in manufacturing was cited as pulling down services on the back of trade uncertainty. Employment notably slid along with orders, with the risk of recession spreading from Germany (composite PMI 48.5, flash 49.1) to the whole region.

UK final composite PMI fell into contractionary territory at 49.3 (est. 50.0, prior 50.2), as services fell to 49.3 (prior 50.6) while manufacturing PMI rose to 48.3 from 47.4 in Aug. Brexit uncertainty clearly was the main concern.

Brexit: EU’s influential Brexit Steering Group stated that the Johnson proposals did not offer a “serious alternative” and were just a “repackaging of old proposals” recommending that EU should not back them given on the basis of “grave concerns in their current form”. Event Outlook

Australia: Aug retail sales are expected to rise 0.5%. Westpac is forecasting a 1.0% lift with tax offset receipts to provide a boost to spending. The biannual RBA Financial Stability Review is released. RBA Assistant Governor (Economic) Ellis speaks in Geelong, 1:20 pm.

US: Sep nonfarm payrolls are anticipated to increase by 148k broadly in line with the six month average of +150k. The unemployment rate is seen to hold at 3.7% while the annual pace of average hourly earnings continues to track at 3.2%yr. Fed Chair Powell delivers opening remarks at a Fed Listens event which also includes Brainard and Quarles. Other Fedspeak involves Vice Chair Clarida on policy (8:35 am Sydney time), Rosengren at the Boston Fed conference and Bostic at Tulane University.

“The NMI® registered 52.6 percent, which is 3.8 percentage points below the August reading of 56.4 percent. This represents continued growth in the non-manufacturing sector, at a slower rate. The Non-Manufacturing Business Activity Index decreased to 55.2 percent, 6.3 percentage points lower than the August reading of 61.5 percent, reflecting growth for the 122nd consecutive month. The New Orders Index registered 53.7 percent; 6.6 percentage points lower than the reading of 60.3 percent in August. The Employment Index decreased 2.7 percentage points in September to 50.4 percent from the August reading of 53.1 percent. The Prices Index increased 1.8 percentage points from the August reading of 58.2 percent to 60 percent, indicating that prices increased in September for the 28th consecutive month. According to the NMI®, 13 non-manufacturing industries reported growth. The non-manufacturing sector pulled back after reflecting strong growth in August. The respondents are mostly concerned about tariffs, labor resources and the direction of the economy.”

Markets were thrilled at such weakness given Fed cut prospects are stronger:

Advertisement

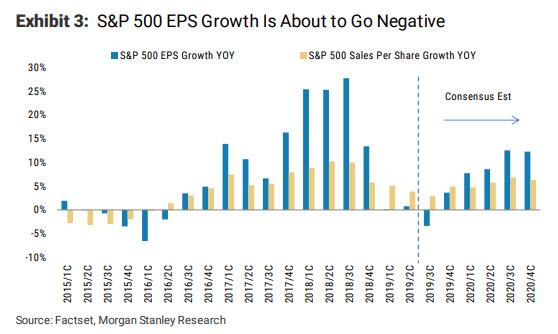

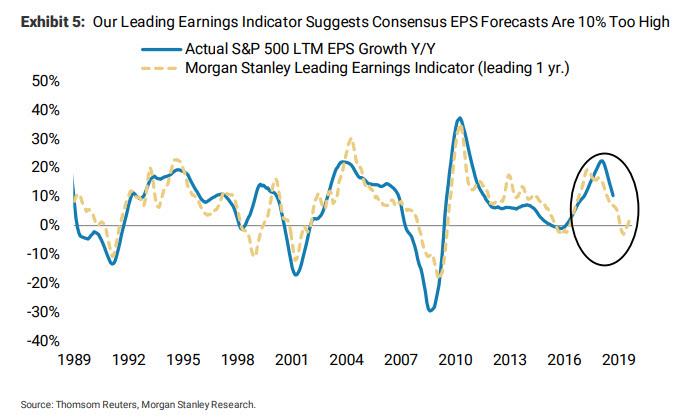

At some point we have to an impasse when falling earnings are going to matter more. Via Morgan Stanley, earnings are already turning negative:

The internals are deteriorating:

Advertisement

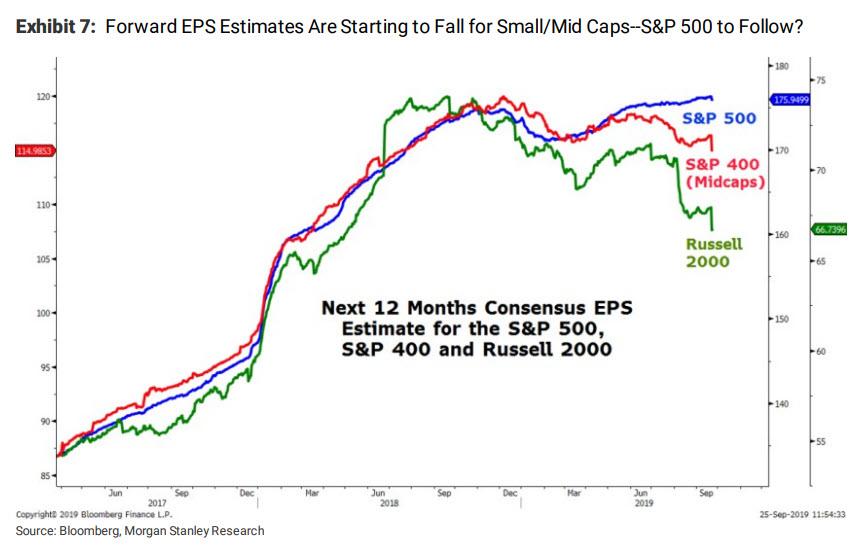

And big adjustment to estimates is ahead:

Markets are still vulnerable to a material correction based solely upon the earnings outlook, let alone the drivers of it.

This would normally be AUD bearish. That the Fed will chase the stock market lower with more cuts will provide some offset to that.

Advertisement

But not enough if it really gets moving and the USD attracts its usual safe haven bid.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.