DXY was sot last night:

But the Australian dollar was even softer:

It was mixed versus EMs:

Gold was hit:

Oil too:

And metals:

Plus miners:

EM stocks bounced:

And junk:

Treasury’s were hosed:

And Bunds:

Aussie bonds did better:

Stocks flew and are forming a bullish ascending triangle pattern:

Westpac has the wrap:

Event Wrap

Brexit: there were various reports that UK and EU negotiators were close to agreement and that the legal text of a Brexit deal could be ready before the EU Summit on Thursday, a Bloomberg report citing two unnamed EU officials who said a draft could be ready by the end of Tuesday.

UK Aug unemployment rose to 3.9% (est. unch. at 3.8%), the 3m/3m employment change fell 56k (est. +26k, prior +31k), and average weekly earnings rose 3.8% (as expected, but down from 3.9%).

The IMF released its updated World Economic Outlook in which the impact of US-China trade dispute (having a cumulative effect of -0.8%) took 2019 growth to 3.0% (from 3.3% in April) and 2020 growth to 3.4% (from 3.6% in April).

Eurozone ZEW surveys stabilised below long-term averages and continue to signal further deterioration of the German and Eurozone economies.

The GDT dairy auction resulted in prices rising 0.5% overall, with key product whole milk powder unchanged, skimmed milk powder up 2.4%, and butter down 0.4%.

Event Outlook

NZ: Q3 CPI is expected to rise 0.6%, for an annual gain of 1.4% (vs 1.7% in Q2).

Australia: Westpac-MI Leading Index is released.

Europe: ECB Chief Economist Lane speaks in Washington.

UK: BOE Governor Carney speaks on a panel at the IMF annual meeting.

US: Sep retail sales are anticipated to rise 0.3% following a 0.4% gain in Aug. Fedspeak involves Evans on policy and Brainard at a Crypto Currency Conference. The Federal Reserve Beige Book is released.

Not much good news for earnings there but, as usual, politics trumped with hope for Brexit, via Bloomie:

U.K. and European Union negotiators in Brussels are closing in on a draft Brexit deal with optimism there will be a breakthrough before the end of the day Tuesday, two EU officials said.

Any draft legal text will hinge on whether Prime Minister Boris Johnson believes he has the support of the U.K. Parliament, with the backing of the Northern Irish Democratic Unionist Party crucial. Officials cautioned talks haven’t finished yet and there’s work still to do.

Even overriding this:

Beijing wants a rollback in tariffs in its trade war with the U.S. before China can feasibly agree to buy as much as $50 billion of American agriculture products that President Donald Trump claims are part of an initial deal, people familiar with the matter said.

Chinese officials are willing to start purchasing more U.S. agricultural products as part of the “phase one” trade deal, but it is not likely to reach the $40 billion to $50 billion touted by Trump under current circumstances, the people said. The people asked not to be identified discussing the private negotiations.

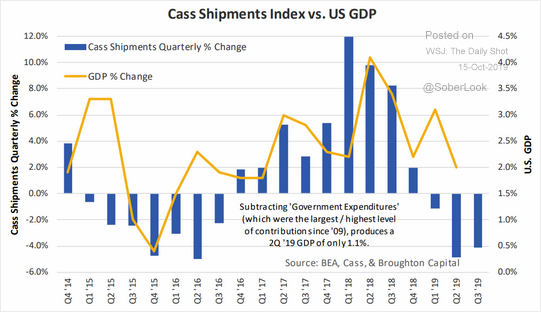

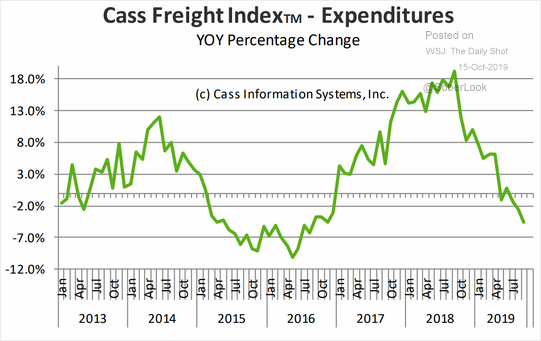

Underneath the equities joy, all signs still point to further trade slowing (charts view Daily Shot). In the US:

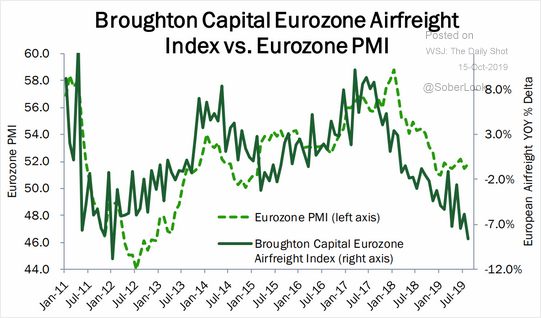

In Europe:

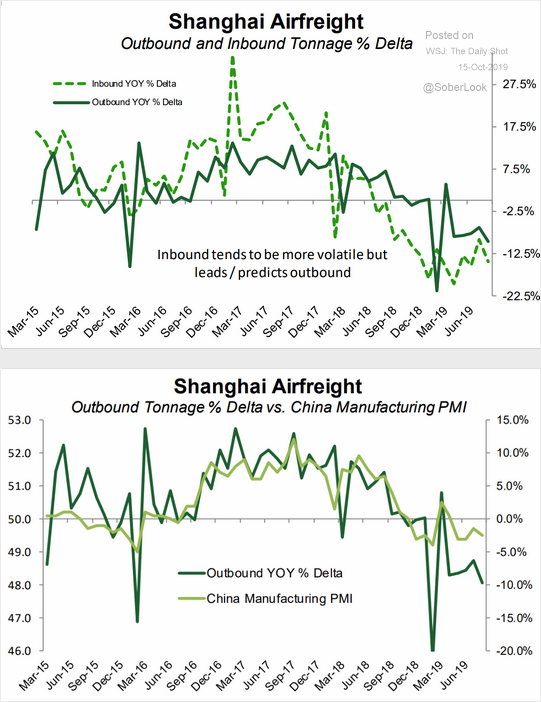

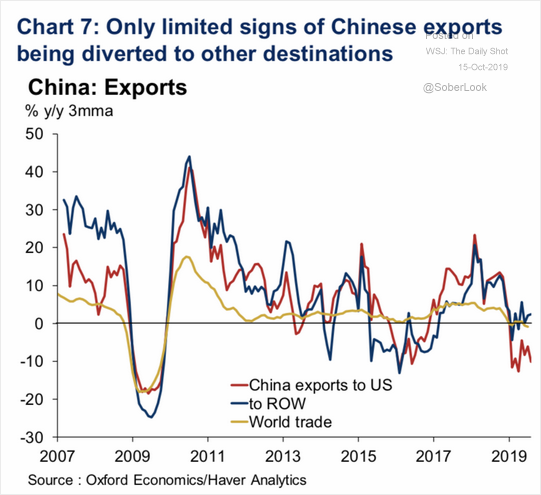

And in China:

And that has commodities falling away still even as stocks party on the political relief rally helping explain the unusual split of the AUD from risk.

I still can’t see the AUD getting much relief.