DXY was firm last night despite a rising EUR and CNY:

The Australian dollar was weak versus DMs:

And EMs:

Gold rose:

Oil hung on:

Copper too:

Big miners struggled:

EM stocks did better:

EM junk rolled:

All bonds were sold:

As stocks rebounded:

Westpac has the event wrap:

The FOMC minutes reflected a generally positive outlook from policymakers, although “many” thought that low inflation plus the risks from trade wars and the global slowdown justified September’s rate cut. A “few” worried that the market was pricing too much easing, and “several” wanted the statement to have more clarity on when the easing would likely end.

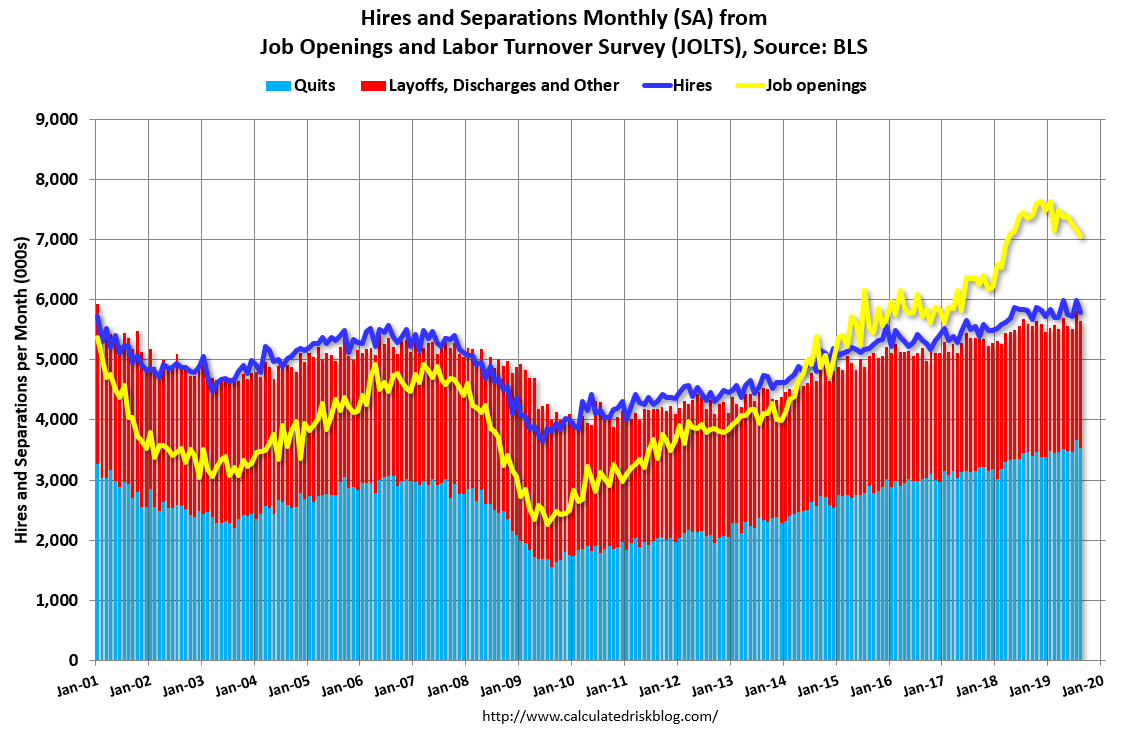

US Aug. JOLTS job openings data showed a drop to 7.05mn (est. 7.25mn, prior revised to 7.17mn from 7.22mn). Although a clear pullback from recent high levels, the BLS point out that the slide is relatively small (openings remain 2mn above than the peaks seen in 2001 and 2007). US final Aug. wholesale inventories were scaled back to +0.2% (initially +0.4%).

Chinese negotiators arrived in the US for trade talks and said they remain open to a partial deal despite the US blacklist on Chinese tech firms.

Turkey launched a military offensive against Kurdish militants in northeast Syria.

Event Outlook

NZ: Food prices for Sep will inform estimates for Q3 CPI.

Australia: Aug housing finance is expected to show the number of owner occupier approvals up 2.3% (Westpac fcs 2.5%).

Europe: the ECB minutes will provide details of the discussion around September’s stimulus package.

US: Sep CPI is anticipated to show headline inflation edging up to 1.8%yr while the core measure maintains a 2.4%yr pace. Fedspeak involves Daly at a community event and Bullard on a panel in Washington.

The Australian dollar fell despite a doving Fed in the minutes:

Participants generally viewed the baseline economic outlook as positive and indicated that their views of the most likely outcomes for economic activity and inflation had changed little since the July meeting. However, for most participants, that economic outlook was premised on a somewhat more accommodative path for policy than in July. Participants generally had become more concerned about risks associated with trade tensions and adverse developments in the geopolitical and global economic spheres. In addition, inflation pressures continued to be muted. Many participants expected that real GDP growth would moderate to around its potential rate in the second half of the year.

…Participants generally judged that downside risks to the outlook for economic activity had increased somewhat since their July meeting, particularly those stemming from trade policy uncertainty and conditions abroad. In addition, although readings on the labor market and the overall economy continued to be strong, a clearer picture of protracted weakness in investment spending, manufacturing production, and exports had emerged. Participants also noted that there continued to be a significant probability of a no-deal Brexit, and that geopolitical tensions had increased in Hong Kong and the Middle East. Several participants commented that, in the wake of this increase in downside risk, the weakness in business spending, manufacturing, and exports could give rise to slower hiring, a development that would likely weigh on consumption and the overall economic outlook.

…Participants judged that conditions in the labor market remained strong, with the unemployment rate near historical lows and continued solid job gains, on average, in recent months. The labor force participation rate of prime-age individuals, especially of prime-age women, moved up in August, continuing its upward trajectory, and the unemployment rate of African Americans fell to its lowest rate on record. However, a number of participants noted that, although the labor market was clearly in a strong position, the preliminary benchmark revision by the Bureau of Labor Statistics indicated that payroll employment gains would likely show less momentum coming into this year when the revisions are incorporated in published data early next year. A few participants observed that it would be important to be vigilant in monitoring incoming data for any sign of softening in labor market conditions.

The number of job openings was little changed at 7.1 million on the last business day of August, the U.S. Bureau of Labor Statistics reported today. Over the month, hires edged down to 5.8 million and separations were little changed at 5.6 million. Within separations, the quits rate was little changed at 2.3 percent, and the layoffs and discharges rate was unchanged at 1.2 percent.

…The number of quits decreased in August to 3.5 million (-142,000). The quits rate was 2.3 percent. The quits level decreased for total private (-144,000) and was little changed for government. Quits decreased in professional and business services (-76,000) and in other services (-67,000).

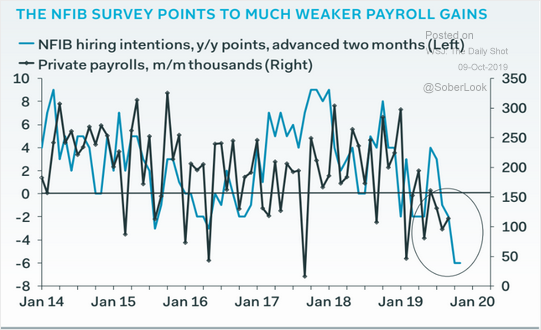

There’s more slowing ahead suggests the NFIB:

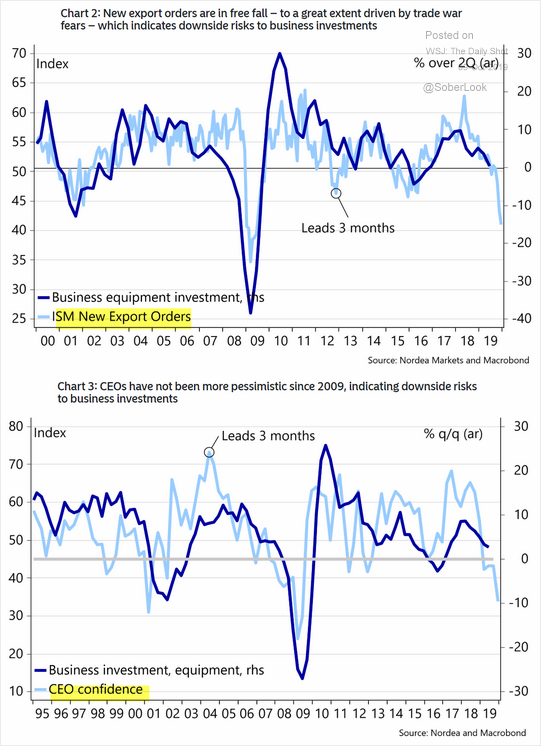

And capex:

There was also more positive scuttlebutt on a trade deal, via Bloomie:

China is still open to reaching a partial trade deal with the U.S., an official with direct knowledge of the talks said, signaling that Beijing is focused on limiting the damage to the world’s second-largest economy.

Negotiators heading to Washington for talks starting Thursday aren’t optimistic about securing a broad agreement that would end the trade war between the two nations, said the official, who asked not to be named as the discussions are private.

But China would accept a limited deal — like those it has sought since 2017 — as long as no more tariffs are imposed by President Donald Trump, including two rounds of higher duties set to take effect this month and in December, the official said. In return, Beijing would offer non-core concessions like purchases of agricultural products without giving in on major sticking points, the official said, without offering further details.

But the AUD could find no solace. One night does not a summer make but the AUD is not hinting at any other than going lower.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.