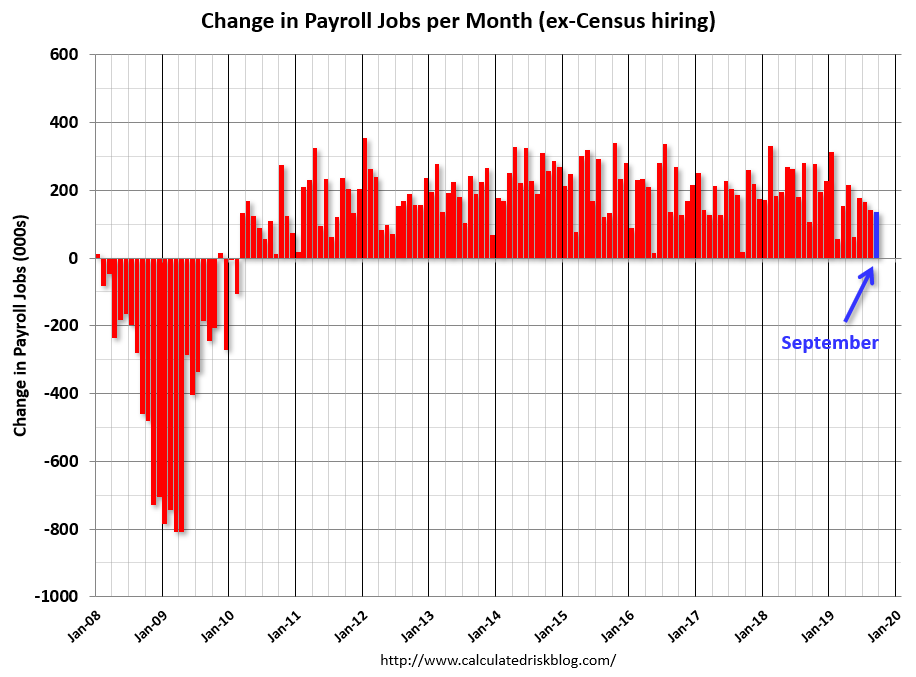

US non-farm payrolls were not as weak as markets had feared. While the Sep outcome of +136k jobs was below the median estimate of 145k, Aug was revised +45k and July +7k.

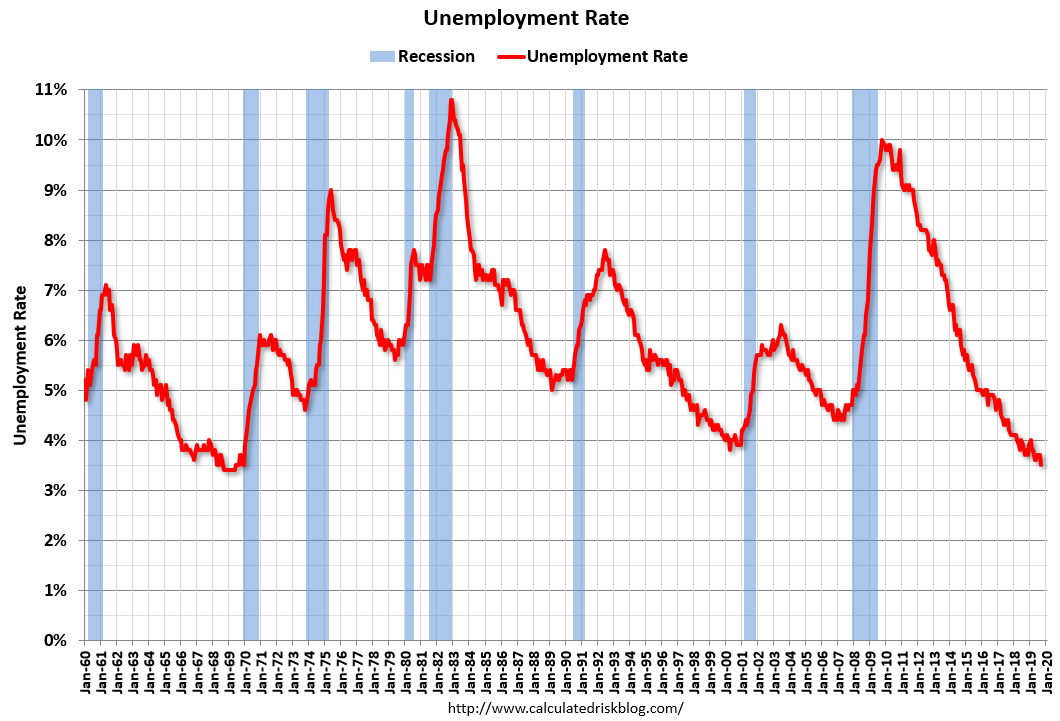

The unemployment rate fell from 3.7% to 3.5% – a 50-year low and lower than the 3.7% expected, while the participation rate remained at 63.2%. A weak spot of the fall in average hourly earnings from 3.2% yoy to 2.9% yoy.

The US administration increased trade tensions with EU, White House adviser Larry Kudlow saying that “by far the biggest problem we have regarding manufacturing and manufacturing exports is Europe”.

FOMC Chair Powell reiterated that the economy is in a “good place,” and that it is “our job to keep it there as long as possible.” He acknowledged there are risks and longer term challenges, with inflation running slightly below the 2% objective and little room to ease in a downturn. Dove Bostic raised the prospect of tariffs impacting US consumers and that it was on the Fed’s watch list, while hawk Rosengren said he’d be inclined not to cut rate further.

Event Outlook

Australia: It is the Labour Day public holiday in NSW, Qld and SA.

China: Sep foreign reserves data is released.

Europe: Oct Sentix investor confidence is expected remain pessimistic at -12.5. Aug German factory orders are expected to decline 0.7% with PMI’s suggesting manufacturing weakness is worsening.

US: Fedspeak involves George at the NABE conference and Kashkari at a community event.

The unemployment rate declined to 3.5 percent in September, and total nonfarm payroll employment rose by 136,000, the U.S. Bureau of Labor Statistics reported today. Employment in health care and in professional and business services continued to trend up.

…Employment in government continued on an upward trend in September (+22,000). Federal hiring for the 2020 Census was negligible (+1,000).

…The change in total nonfarm payroll employment for July was revised up by 7,000 from +159,000 to +166,000, and the change for August was revised up by 38,000 from +130,000 to +168,000. With these revisions, employment gains in July and August combined were 45,000 more than previously reported.

…In September, average hourly earnings for all employees on private nonfarm payrolls, at $28.09, were little changed (-1 cent), after rising by 11 cents in August. Over the past 12 months, average hourly earnings have increased by 2.9 percent.

Headline was softish:

Advertisement

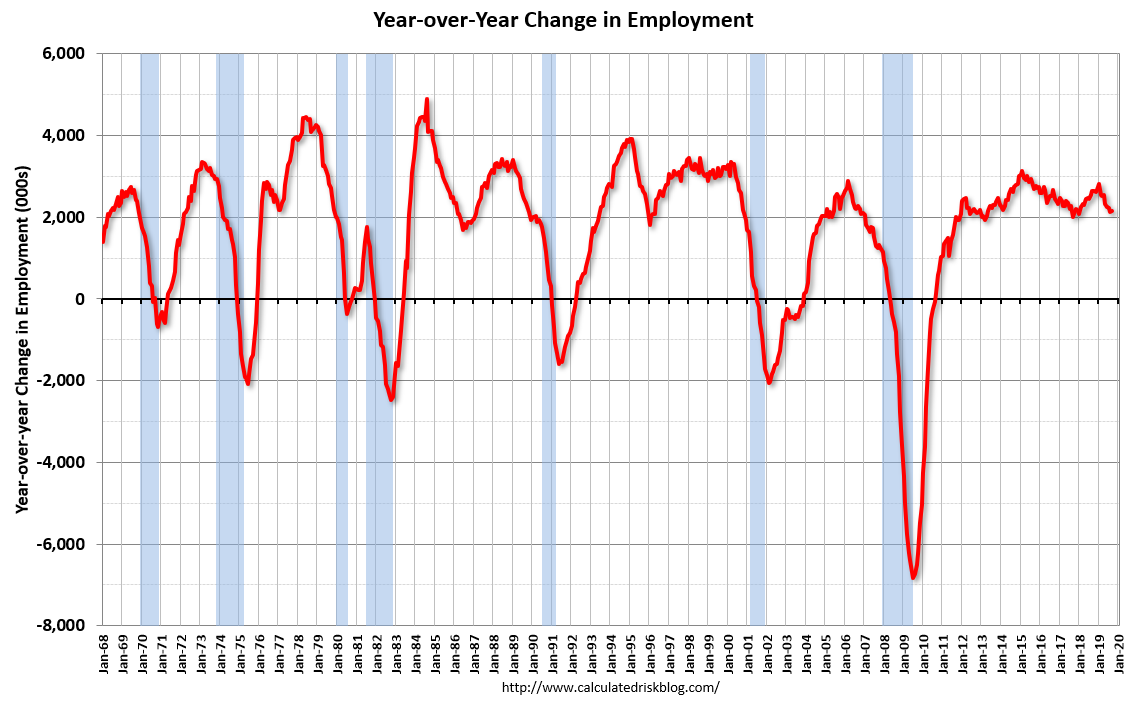

Jobs growth remains good:

The unemployment rate is at a 50 year low:

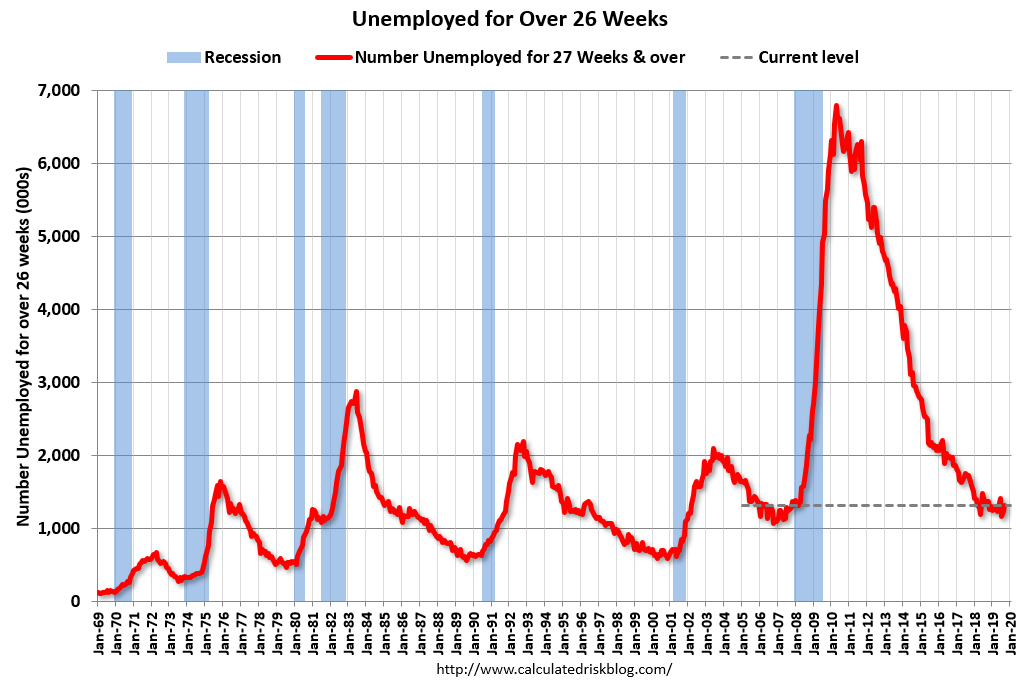

But shadow slack still remains:

Advertisement

And wages growth fell sharply:

So, just enough weakness to deliver some Fed easing but string enough to support earnings. Goldilocks. Which lifted risk trades all over, including the AUD.

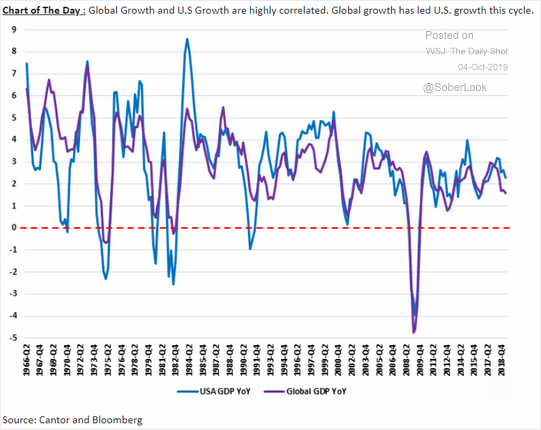

Meanwhile, the divers of the slowdown are intact so we should still expect further slowing as global growth slows more:

Advertisement

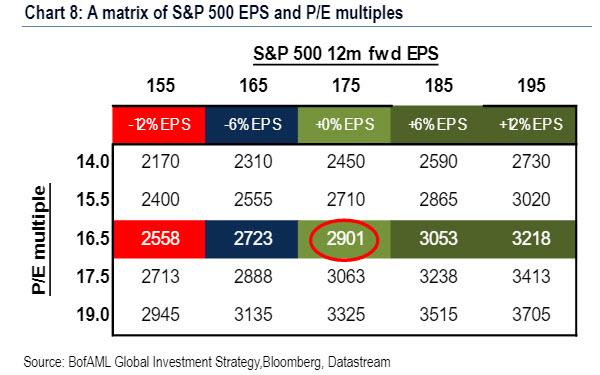

BofAML says position for the policy panic. Earnings are breaking down:

Which poses a distinct risk to stocks:

With a policy panic resulting in:

Buy Chinese equities to play Trump pivot on tariffs

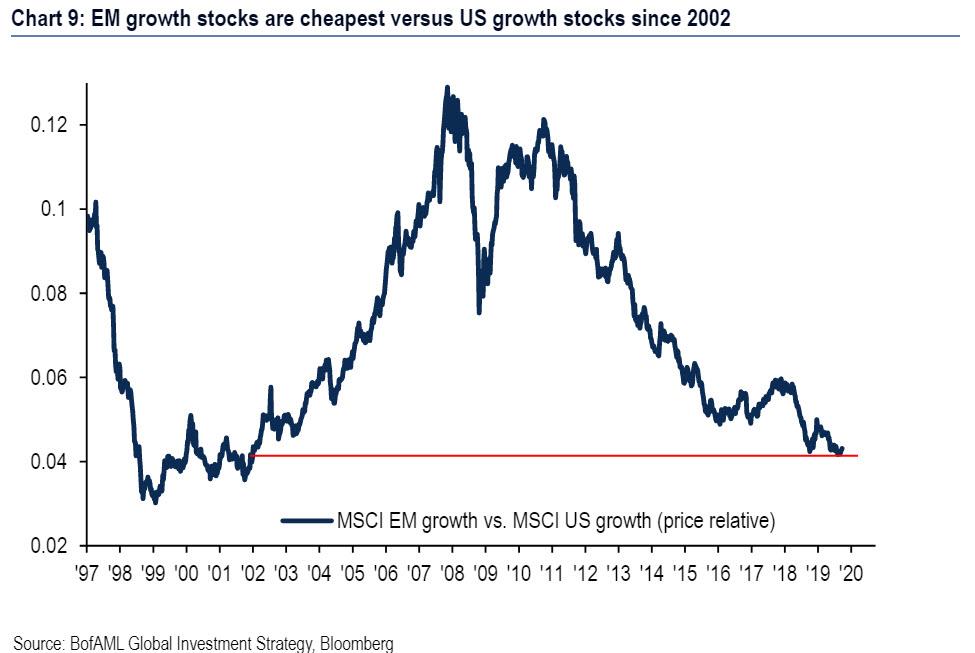

Buy EM stocks should weak payroll “top” the US dollar (EM growth stocks are cheapest versus US growth stocks since 2002)

Buy US homebuilders as Fed cuts accelerate

Buy US exporters as US$ devalues

Buy EAFE small cap as Germany bows to inevitable fiscal stimulus post-Brexit

Buy UK mid cap stocks as end to Brexit ends multi-year pessimism on UK assets

Hedge recession via long 2-year Treasuries (125bps above 2011 lows) and gold

Hedge recession via selling US consumer and global credit proxies into strength

Policy panic trades: buy China, EM, US housing, EAFE small cap, UK mid cap; hedge via long GT2, gold.

And long AUD by implication.

But why would policy-makers panic if there is no damage to markets first? These trades are for the bust. Without one they don’t happen.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.