DXY was soft last night. EUR rebounded and CNY is flat:

The Australian dollar was universally smashed but managed to rebound again versus USD:

Advertisement

Gold jumped:

Oil is deep trouble:

Metals were soft:

Advertisement

Big miners crashed:

EM stocks ugly:

US junk was bashed with oil. EM held up when it shouldn’t:

Advertisement

Treasuries were gold:

Bunds not so:

Advertisement

Aussie bonds were bid with the belly of the curve at records:

Stocks were hit hard:

Advertisement

Westpac has the wrap:

Event Wrap

US ADP private sector employment rose 135k in Sep, less than the 140k expected, while August’s previously abnormally high 195k was revised lower to 157k.

FOMC member Barkin said his policy stance is “very balanced”. He acknowledged the impact of various uncertainties on business confidence but didn’t expect a recession.

The German Institute (a combination of economic research bodies) lowered its German 2019 and 2020 growth forecasts to +0.5%y/y (from +0.8%y/y) and +1.1%y/y (from 1.8%) respectively. They affirmed that Germany was now in recession, and that it was only the retail/consumer sector that remained positive.

The WTO ruled that the US can impose tariffs on up to $7.5bn of European exports annually, after Airbus was found to have received illegal government aid.

Brexit: UK PM Boris Johnson presented a letter to EU on changes to Irish border proposals that the UK see as sufficient to push towards a potential deal prior to the Queens’ Speech (14Oct.) and the EU Summit. Media and Irish responses were somewhat dismissive, though Junker and even Barnier suggested that they were encouraging for progress even if more work is needed. UK’s DUP and the Conservative’s ERG stated approval. The UK Govt. intends to prorogue Parliament on 8 Oct. in advance of the Queen’s Speech (note that this is much more in line with usual Queen’s Speech practice).

Event Outlook

US: Sep ISM non-manufacturing is expected to remain solid at 55.2 in contrast to weakness seen in manufacturing. Aug factory orders are anticipated to decline 0.2% with the soft trend in durables persisting. Fedspeak involves Evans in Madrid, Quarles at a banking conference in Brussels, Mester on a panel about inflation and Kaplan at a community event.

Markets are worried about US growth. More worried than data suggest that they should be. The ADP employment reported spooked as it came in a little below consensus:

Private sector employment increased by 135,000 jobs from August to September according to the September ADP National Employment Report®. … The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.

…“The job market has shown signs of a slowdown,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “The average monthly job growth for the past three months is 145,000, down from 214,000 for the same time period last year.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Businesses have turned more cautious in their hiring. Small businesses have become especially hesitant. If businesses pull back any further, unemployment will begin to rise.”

Advertisement

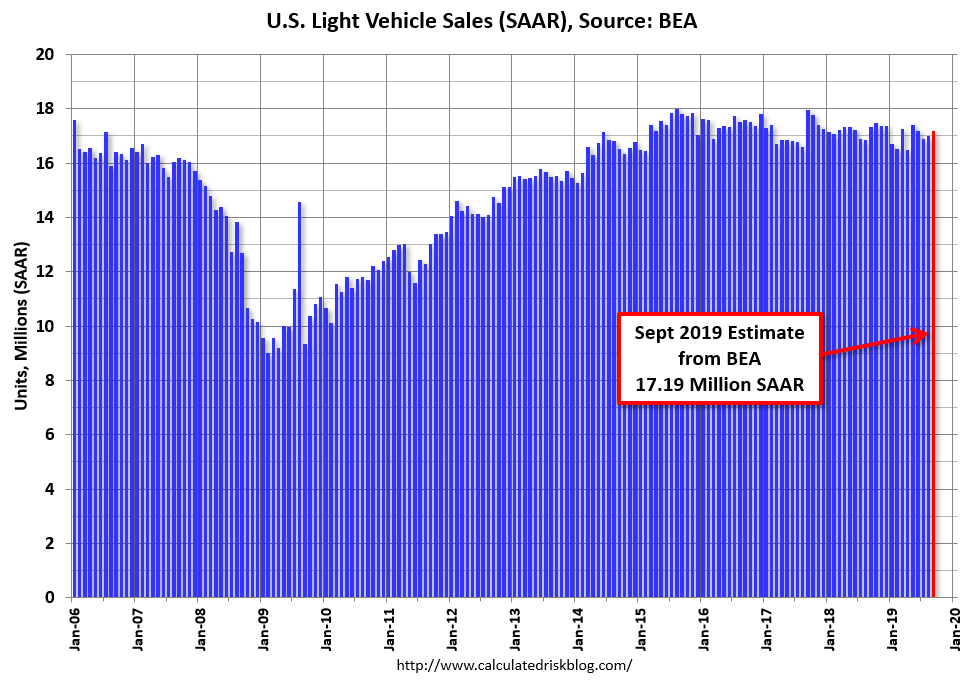

Hardly the end of the world. And car sales were better than feared:

The BEA released their estimate of September vehicle sales this morning. The BEA estimated sales of 17.19 million SAAR in September 2019 (Seasonally Adjusted Annual Rate), up 1.1% from the August sales rate, and down 0.7% from September 2019.

Sales in 2019 are averaging 16.96 million (average of seasonally adjusted rate), down 1.1% compared to the same period in 2018.

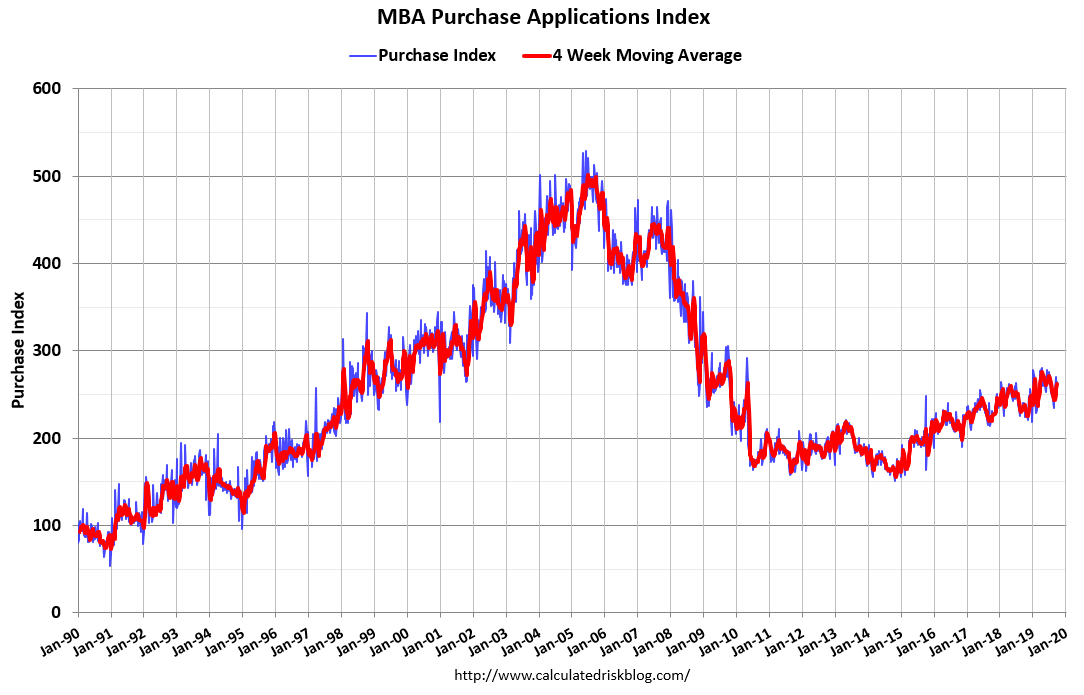

Mortgage applications increased 8.1 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 27, 2019.

… The Refinance Index increased 14 percent from the previous week and was 133 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 1 percent compared with the previous week and was 10 percent higher than the same week one year ago.

…

“Mortgage rates mostly decreased last week, with the 30-year fixed rate dropping below 4 percent for the sixth time in the past nine weeks. Borrowers responded to these lower rates, leading to a 14 percent increase in refinance applications,” said Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting. “Although refinance activity slowed in September compared to August, the months together were the strongest since October 2016. The slight changes in rates are still causing large swings in refinance volume, and we expect this sensitivity to persist.”

Added Kan, “Purchase applications also increased and remained more than 9 percent higher than a year ago. Low rates and healthy housing market fundamentals continue to support solid levels of purchase activity.”

The US is slowing as expected but not falling off any cliffs. The problem is that, in context, the US is the last growth standout so as it slows the problems everywhere become worse.

And MB’s four horsemen of the end-of-cycle shock are pulling into a gallop. Brexit is accelerating again, at the FT:

Advertisement

The prime minister’s allies said Mr Johnson would negotiate with Brussels, but if his plan was rejected outright he would break off all talks and start preparing for a no-deal exit…The plan is highly contentious, replacing Theresa May’s “backstop” plan — intended to maintain an open border in Ireland — with the creation of two new borders: a customs frontier in Ireland and a new regulatory frontier between Northern Ireland and the rest of the UK.

Northern Ireland’s Democratic Unionist party signalled it could accept the new system — which would see the region adopt EU regulations for goods, agriculture and food — provided the Northern Ireland assembly gives its consent every four years.

…Mr Johnson can now reassure the EU that he has united his party and its Northern Irish supporters in parliament and stands a reasonable chance of passing a rewritten Brexit treaty through the House of Commons. The big problem is that his proposals fall far short of satisfying the EU’s demands to protect the all-island economy, north-south co-operation and the Good Friday Agreement.

Politics is the latest obstacle, with the White House weighing a ban on Chinese companies listing in the US. Peter Navarro, White House trade adviser, may have dismissed the reports as “highly inaccurate” but he stopped short of specific rebuttals and American angst over China continues to manifest itself from trade to Silicon Valley to Wall Street, driven by the likes of Republican senator Marco Rubio.

US exchanges and regulators are similarly antsy. Nasdaq, waking up to the low trading volumes and high volatility of smaller Chinese stocks, is seeking to impose stricter rules, according to Reuters. The Public Company Accounting Oversight Board has again sounded the alert on China’s refusal to allow it to inspect the audits of Chinese companies listed in the US.

Not everyone is so leery. Hong Kong regulators have been far more willing to play ball. The stock exchange last year introduced dual-class shares, the absence of which cost it Alibaba’s record-breaking $25bn initial public offering in 2014. The only problem there is sentiment: markets are disturbed by the protesters’ clashes in the streets; the benchmark Hang Seng index is down 10 per cent since July 1.

…The doors may be closing. US shareholders are not dashing to prop them open.

Driven by anger and grief, thousands of people came on to the streets of Hong Kong on Wednesday to denounce the shooting of a teenage student by police, an escalation of force that has intensified the standoff between protesters and authorities.

In the daytime the protesters marched through the city centre, organised sit-ins at schools and gathered at a courtroom where other demonstrators faced rioting charges. In the evening thousands more joined largely peaceful rallies across Hong Kong, denouncing police brutality. Some called for the police force to be disbanded.

Many at the demonstrations held their hands over the left side of their chests in tribute to 18-year-old Tsang Chi-kin, who was shot at point-blank range on Tuesday, with the bullet narrowly missing his heart. Tsang was in hospital in stable but critical condition after surgery to remove the bullet.

The shooting shocked many in the city; despite copious use of teargas, water cannon, beanbags and other less lethal forms of violence over nearly four months of protests, officers had previously only fired their guns in warning.

And there’s too much damn oil as we enter the low demand season:

Advertisement

Which is compounding US growth worries:

We’re closer than ever to a break in earnings and the stock market. One shock away.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.