It was PMI night and it told the tale. Europe is going precisely nowhere:

Key findings:

▪ Flash Eurozone PMI Composite Output Index(1) at 50.2 (50.1 in September). 2-month high.

▪ Flash Eurozone Services PMI Activity Index(2) at 51.8 (51.6 in September). 2-month high.

▪ Flash Eurozone Manufacturing PMI Output Index(4) at 46.2 (46.1 in September). 2-month high.

▪ Flash Eurozone Manufacturing PMI(3) at 45.7 (45.7 in September). Unchanged rate of decline.

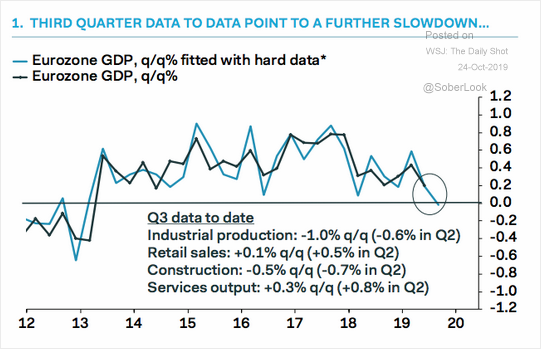

The Eurozone economy remained close to stagnation at the start of the fourth quarter, according to the latest flash PMI data, with demand for goods and services falling for a second successive month. A further steep decline in manufacturing output was accompanied by one of the weakest service sector expansions since 2014. Future expectations sank to the gloomiest since 2013 and jobs growth hit the lowest since 2014. Selling price inflation meanwhile stuck at a near three-year low amid muted cost pressures. By country, an improved performance in France helped keep the eurozone out of contraction, alongside a mild easing in the rate of decline in Germany. However, the rest of the region slowed closer to stagnation.

Germany in particular remains weak with no manufacturing bounce (41.7) and services (51.2) now falling away. There is more weakness ahead:

Advertisement

The US PMI (not ISM), on the other hand, bounced:

Key findings:

Flash U.S. Composite Output Index at 51.2 (51.0 in September). 3-month high.

Flash U.S. Services Business Activity Index at 51.0 (50.9 in September). 3-month high.

Flash U.S. Manufacturing PMI at 51.5 (51.1 in September). 6-month high.

Flash U.S. Manufacturing Output Index at 52.7 (51.8 in September). 6-month high.

Flash PMI data for October indicated a marginal increase in the rate of growth of business activity, supported by the fastest expansion of manufacturing production for six months. Growth of service sector activity also picked up, though rates of expansion in both sectors remained subdued. Adjusted for seasonal influences, the IHS Markit Flash U.S. Composite PMI Output Index reached 51.2 in October, up from 51.0 during September, to signal the sharpest increase in business activity since July. The latest reading pointed to another gradual recovery in output growth from the threeand-a-half year low seen in August.

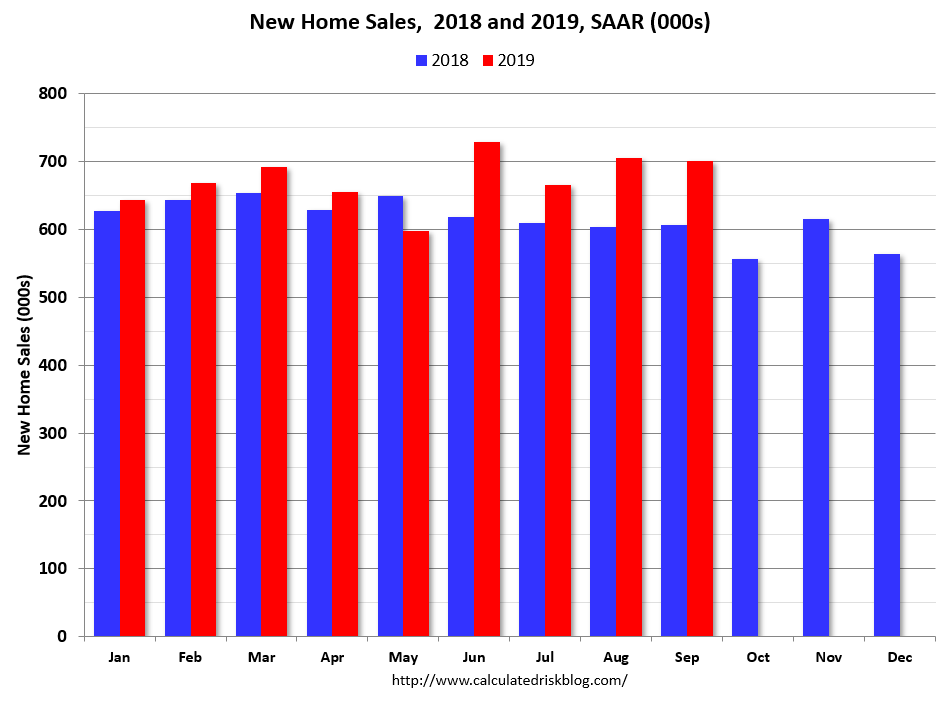

“Sales of new single‐family houses in September 2019 were at a seasonally adjusted annual rate of 701,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 0.7 percent below the revised August rate of 706,000, but is 15.5 percent above the September 2018 estimate of 607,000.”

Which will lift manufacturing in time:

Advertisement

A few points then:

US growth is now hanging on low yields at the long end of the bond curve which fixes US mortgage rates. It can’t sell-off or growth will stall so that’s bullish for bonds;

So long as US growth outperforms Europe, DXY will be strong and the AUD weak.

Europe needs to recover before the AUD can rise but it is still squashed by the trade war and Brexit while the US is shifting gear upwards faster.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.