DXY rebounded last night as EUR fell:

The Australian dollar rolled over against DMs:

EMs were even weaker:

Gold has formed a downtrend:

Oil reversed:

And metals:

Plus miners:

And EM stocks:

Junk did better:

Bonds were mostly sold:

Not Australia:

Stocks held on grimly:

Westpac has the evetn wrap:

Event Wrap

US NY (Empire) manufacturing survey rose 4.0% (vs 1.0% expected), although the components were mixed. New orders were flat, while employment, prices paid, and prices received all fell. The six-month outlook rose.

Eurozone August industrial production was weak, despite beating m/m estimates (0.4% vs 0.3%) it contracted -2.8%y/y (est. -2.5%y/y). The y/y weakness underscored the basis of ECB’s accommodation. .

Event Outlook

NZ: REINZ house sales for Oct will be closely watched for signs of a pickup following large declines in mortgage rates. Sep migration is also out today.

Australia: The RBA minutes will provide further detail around the decision to cut interest rates at the October meeting and offer clues on the Board’s willingness to act at upcoming meetings.

Japan: BOJ Governor Kuroda speaks at the Branch Managers’ Meeting.

China: Sep CPI has been drifting higher.

Europe: Oct ZEW survey of expectations were last at -22.4, having continued to deteriorate over recent months.

UK: Aug ILO unemployment rate is expected to hold at 3.8%. BOE Governor Carney testifies at the Treasury Committee session on the Financial Stability report.

US: Fedspeak involves Bullard in London, Bostic at a community event, George at a payments event and Daly in LA.

Bloomie reported on trade jitters:

China wants to hold more talks this month to hammer out the details of the “phase one” trade deal touted by Donald Trump before Xi Jinping agrees to sign it, according to people familiar with the matter.

Beijing may send a delegation led by Vice Premier Liu He, China’s top negotiator, to finalize a written deal that could be signed by the presidents at the Asia-Pacific Economic Cooperation summit next month in Chile, one of the people said. Another person said China also wants Trump to scrap a planned tariff hike in December in addition to the hike scheduled for this week, something the administration hasn’t yet endorsed. The people asked not to be named discussing the private negotiations.

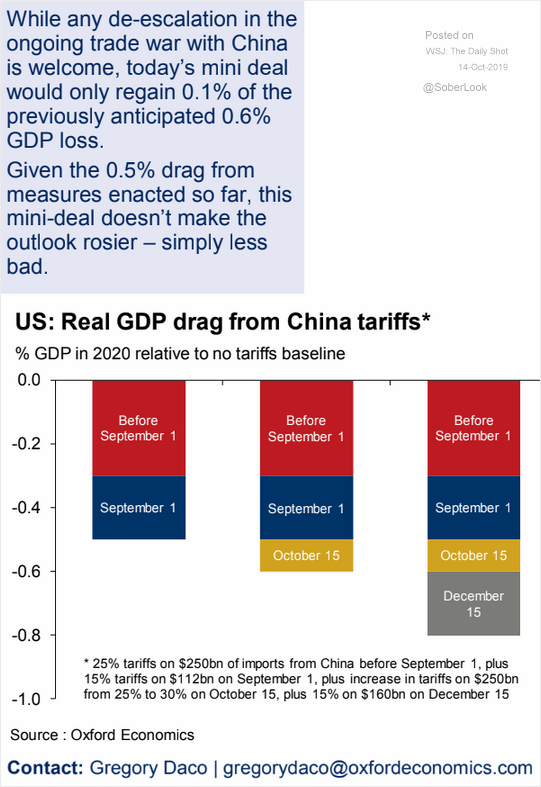

But the real issue is that “phase one” does nothing for global growth anyway, and phase two is impossible. For the US:

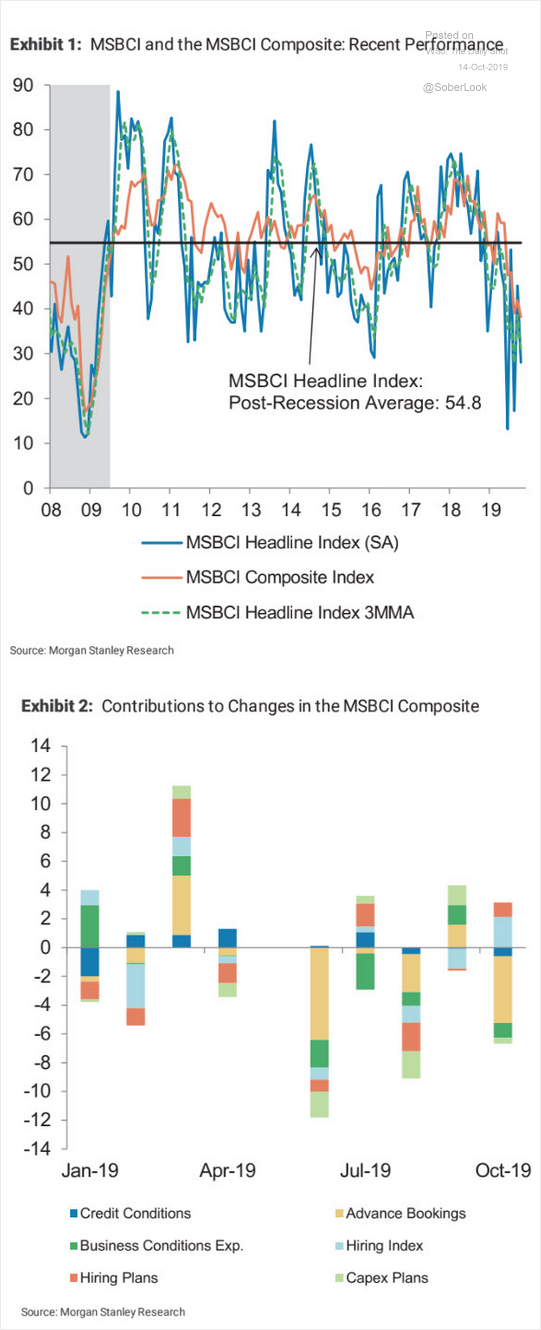

Which hits business investment:

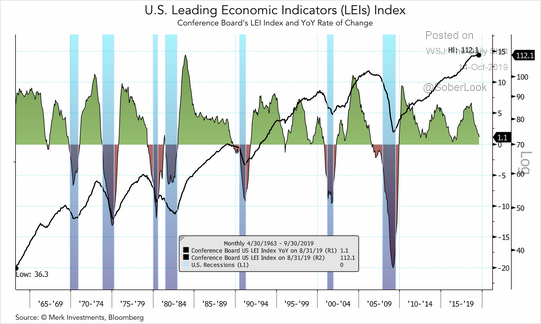

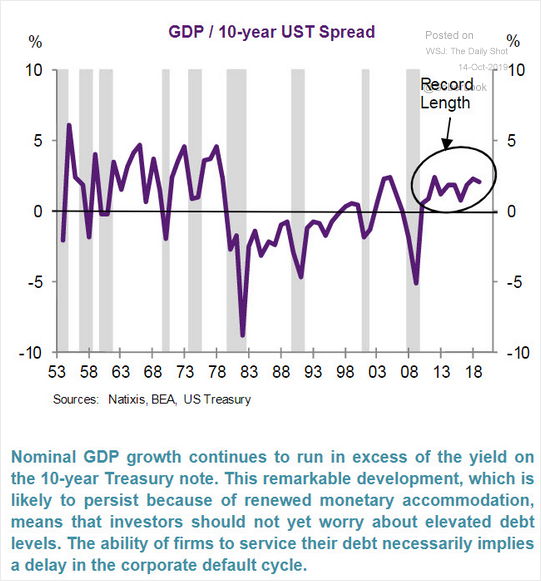

The economy can hang on thanks to low interest rates but that’s about all:

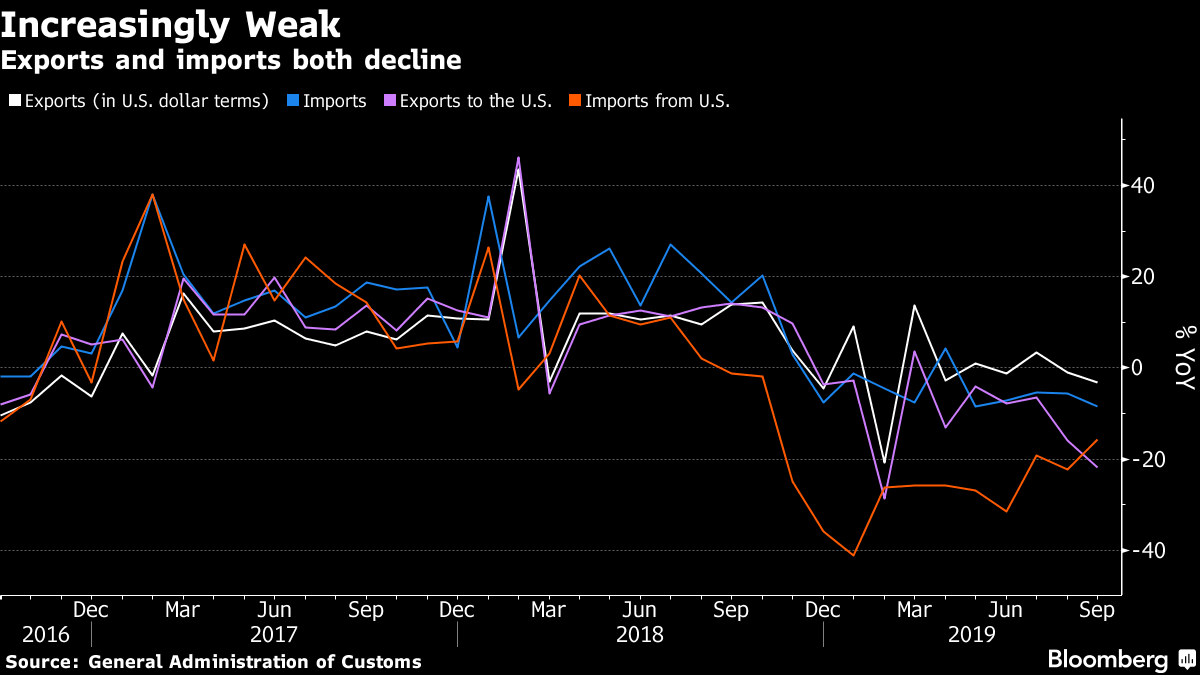

And, meanwhile, China sinks as supply chains keep pulling out:

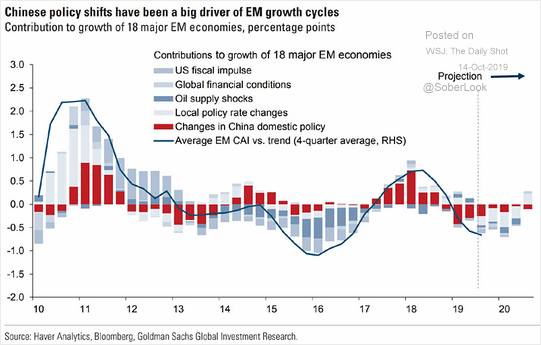

Leading EM growth lower:

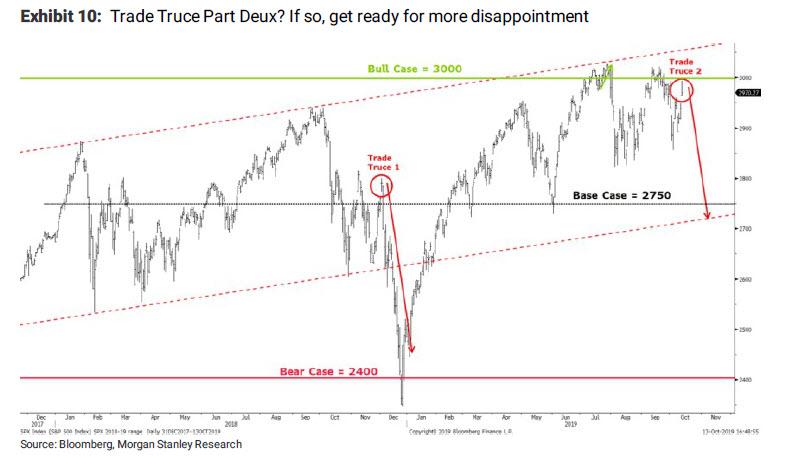

At a certain point, damage to earnings will be sufficient to trigger a stock market shakeout and we’re are as good as cooked for global recession:

Unless or until we get the full Fed and Chinese stimulus cavalry.

The Australian dollar will be torn between trade non-deal phase one hopes and the fact that it is not enough to lift global growth. I still expect the latter to win out over time.