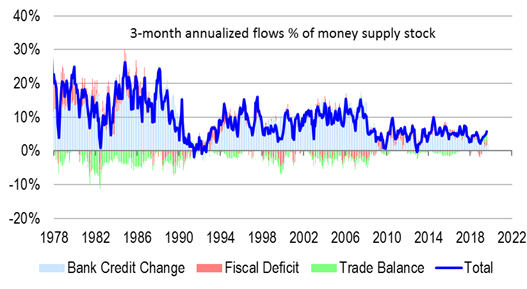

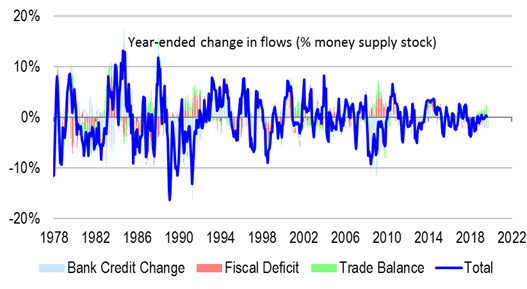

Our proprietary measure of the Australian credit impulse has picked up to 5.6% annualized in August, from 4.9% in July, and 4.6% in June. Importantly, the credit impulse is well off the lows we saw at the end of 2018. Indeed, the impulse is running at its fastest pace since 2017. The implication is that financial conditions are genuinely easing, partly because the Federal government has sharply turned around its spending position from surplus at the end of 2018, to deficit in 2H 2019. The government is printing money again. Anyone waiting for the terms of trade boom to filter through to the real economy finally has something to cheer about. And from an investment perspective, the way to play this is via curve steepening in the fixed income space, and value investing within equities.

First, a re-cap of how we measure the credit impulse. Modern monetary theory (MMT) teaches us that bank loans create deposits – not the other way around. Similarly, Federal government deficit spending creates deposits. Governments spend currency into existence before raising it via taxes. From a stock perspective, money supply (deposits) should equal the sum of bank credit, and Federal government debt. There is of course, the issue of shadow money – securities that have money-like properties, but let us exclude consideration of these for the moment.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.