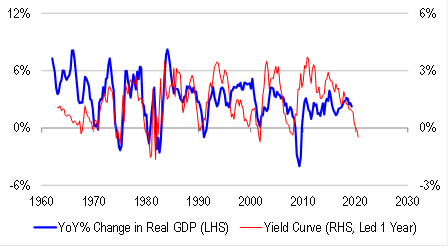

Most people focus on the recession risk embedded in an inverted yield curve. And this makes sense, because eight out of ten times when the curve inverts, a recession follows within the next year or so.

However, we suggest a better way of interpreting curve inversions – via the lens of correlation risk in one’s portfolio. Ten out of ten times when the curve inverts, we see:

Central bankers at a loss to explain why the curve is foreshadowing monetary easing because financial conditions have become too tight. But although financial conditions might not appear tight from a real economy perspective, they may have already become tight from a financial market perspective, with the latter often leading the former. What we mean is that cash rates and bond yields have already risen above levels able to sustain elevated valuations on alternative asset classes, creating the risk of a bubble or two bursting.

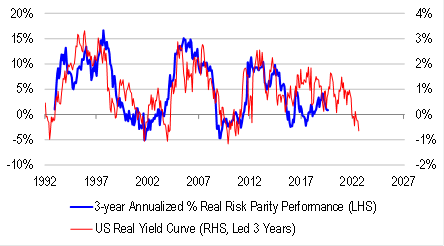

Passive investing strategies underperform in the subsequent two-to-three years. This is because passive strategies are dependent on low correlation between asset classes to work. But in an inverted curve environment, the batting order of expected returns across asset classes has changed meaningfully from historical norms, meaning that correlations between them have also changed. Indeed, if there are several bubbles out there, the risk is that correlations have risen from zero or negative towards one, consistent with loss of diversification.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.