Last week, Labor’s policy thinktank, the McKell Institute, released highly dubious ‘research’ claiming that there is no evidence that previous compulsory superannuation increases eroded workers’ pay rises, and arguing that cancelling scheduled increases in the superannuation guarantee “will only harm workers’ overall wealth and income” (Here’s MB post demolishing these claims).

Below is the Grattan Institute’s response to McKell, which also comprehensively demolishes its flaky claims:

For 25 years successive Australian governments have concluded that higher compulsory super contributions come at the expense of lower wages for workers.

The Henry Tax Review in 2010 acknowledged higher super was paid for by lower wages when it explicitly recommended against increasing compulsory super above 9 per cent:

“Although employers are required to make superannuation guarantee contributions, employees bear the cost of these contributions through lower wage growth. This means the increase in the employee’s retirement income is achieved by reducing their standard of living before retirement…

The retirement income report recommended that the superannuation guarantee rate remain at 9 per cent. In coming to this recommendation the Review took into the account the effect that the superannuation guarantee has on the pre-retirement income of low-income earners.”

Even Paul Keating acknowledges that past increases in compulsory superannuation came out of wages, not from the pockets of employers:

“The cost of superannuation was never borne by employers. It was absorbed into the overall wage cost… In other words, had employers not paid 9 percentage points of wages, as superannuation contributions, they would have paid it in cash as wages.”

And in documents recently released under freedom of information today the Treasury was clear that higher compulsory superannuation contributions would mean lower wages for workers:

“Though compulsory SG contributions are paid by employees, wage setting generally takes into account all labour costs. It is widely accepted that employees bear the cost of higher SG in the form of lower take-home pay. This means there will be a trade-off between people’s income during their working lives and their income during their retirement.”

In fact compulsory super was explicitly designed at its inception to forestall wage rises. Concerned about a wages breakout in 1985, then Treasurer Paul Keating and ACTU Secretary Bill Kelty struck a deal to defer wage rises in exchange for super contributions.

The Government paper announcing the establishment of compulsory superannuation in 1992, Security in Retirement: Planning for Tomorrow Today was even more explicit that compulsory superannuation was intended to be paid by workers via lower growth in their wages:

“A major challenge for retirement incomes policy is the need for current consumption to be deferred in favour of future income in retirement … No loss of remuneration is involved in meeting this national challenge. What is involved, rather, is forgoing a faster increase in real take‑home pay in return for a higher standard of living in retirement.”

Of course the full impact of higher compulsory super might not be felt fully via lower wages, or immediately. For example, firms could respond to higher compulsory super contributions by raising prices, but this would raise the cost of living, so the impact would be largely the same as reducing workers’ nominal wages.

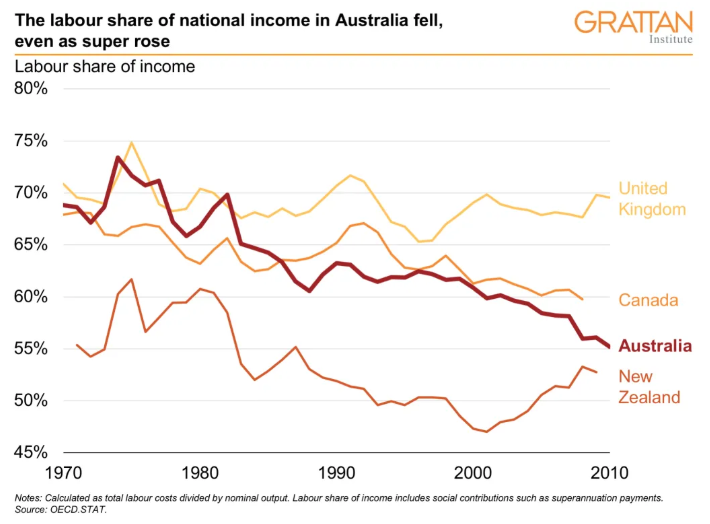

Similarly firms could respond to higher compulsory super contributions by absorbing them, but there is scant evidence business has done this to date. In fact, the trend over the past three decades is the opposite. Profits are up, and labour’s share of income (including superannuation) has gone down in Australia in line with other countries.

When compulsory super was introduced via awards in 1986, workers’ total remuneration (excluding super) made up 63.3 per cent of national income. By 2002, when the phase-in was complete, it made up 60.1 per cent. Out of the 26 countries for which the Organisation for Economic Co-operation and Development has data, Australia recorded the 10th largest slide in the labour share of national income during the period compulsory super contributions were ramped up.

Fast forward to today and there is growing concern about low wages growth in Australia. But if employers aren’t willing to give wage rises, why would they absorb an increase in compulsory super contributions? Nominal wages are still rising by more than 2 per cent a year, so employers have lots of scope to slow the pace of growth in nominal wages — even by cutting real wages — if compulsory super contributions are increased.

McKell’s modelling suffers from fatal flaws

McKell attempts to model the relationship between increases in compulsory super in the past and higher wages. But their approach is fatally flawed, for several reasons.

McKell’s approach takes the average of Average Earnings in the National Accounts (AENA) and Average Weekly Ordinary Time Earnings (AWOTE) to ‘reduce volatility’ in their model. The resulting number is not economically meaningful: it is the average of two overlapping but structurally different measures of wage growth. AENA includes all kinds of wages for all kinds of employees. The number of people working part-time has increased substantially since 1992, and this puts downward pressure on wages as measured by AENA. Greater employee bonuses or increased overtime will put upward pressure on AENA wages. But these changes in the composition of AENA have little to do with the Superannuation Guarantee (SG). The RBA acknowledges the difficulty in ‘separating out noise from signal’ when using AENA. AWOTE – which measures ‘full-time adult ordinary time earnings‘ – is more compositionally stable over the 1992-2016 period and should be the focus of analysis in this area.

The timing of SG increases was complex in the 1990s. It appears that McKell only considers scheduled SG increases for large firms (more than $1 million in annual payroll). But through the 1990s compulsory super contributions rose at various different times for small and large firms. In addition, the timing of 1993 SG changes for large firms was different for firms that were employers for the entire 1991-92 financial year than for employers that were not. Pinpointing the legislated changes to the SG is crucial.

McKell assumes that before the introduction of the SG in 1992, there was no superannuation. But in 1991, 78 per cent of employees were already covered by superannuation.

McKell uses a prediction model for causal analysis, without adjusting the model to an appropriate structure. In fact, McKell removes without justification a key variable used by the RBA to ‘capture persistent factors affecting wage growth’. As a consequence, the McKell model explains much less of the variation in wages over time than the original RBA model.

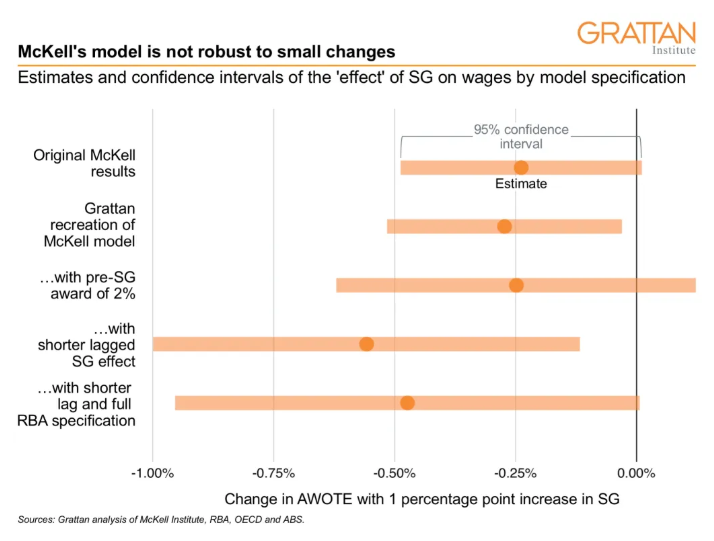

All of these problems mean that McKell’s model is not robust to small changes in the model structure or underlying data. Grattan has recreated McKell’s model, and we find that even minor changes to the approach generate very different conclusions.

McKell finds that increasing the Super Guarantee by one percentage point is associated with a 0.24 percentage point decrease in AWOTE wage growth, and a 0.37 per cent increase based AENA wage growth. But the chart below shows what happens when we change the model slightly.

The original McKell results and Grattan’s recreation are plotted first. Then, a pre-SG rate of 2 per cent is added to reflect the majority super coverage in 1991 (this is a conservative estimate). The next model varies how the SG enters the model: it now lasts for three months and is lagged by half a year (allowing time for wages to adjust). This specification suggests the largest relationship between wages and the SG. The RBA’s full specification is added to the last model, which produces substantial variance.

In each case the model finds that a rise to the SG is associated with a reduction in AWOTE wages — the best wage measure McKell uses — but only under particular specifications is this finding significant. Econometric time-series modelling of this type is notoriously hard to do well, and easy to get badly wrong. McKell’s approach should leave us sceptical of their findings.

Higher compulsory super contributions are neither helpful nor necessary

The McKell research also sidesteps the fact that higher compulsory super contributions won’t actually translate into higher retirement incomes for many Australians. Middle-income workers would give up wages of close to 2.5 per cent while working, in exchange for less than a 1 per cent boost to their retirement incomes.

Just about all of the extra income from a higher super balance at retirement would be offset by lower pension payments, due to the pension assets test. And pension payments themselves would be lower under a 12 per cent superannuation regime, because pension payments are benchmarked to wages, which would be lower if employers had to put more into super. We calculate it could cost today’s typical (median) 30-year-old Australian worker $30,000 over their lifetime.

Lifting compulsory super to 12 per cent of wages from the present 9.5 per cent would cost the federal budget at least $2 billion a year. These budgetary estimates are not based on some theoretical treatment of tax breaks; they are based on how Treasury expected actual changes in compulsory super to hit previous budgets. It’s true that compulsory super today has lowered pension spending. But Treasury projections have also shown that the tax breaks from 12 per cent compulsory super would dwarf any budget savings on the Age Pension as far out as 2060.

Nor are higher compulsory super contributions needed. The average Australian worker can expect a retirement income of at least 89 per cent of their pre-retirement income – well above the 70 per cent benchmark endorsed by the OECD, and more than enough to maintain pre-retirement living standards. Grattan’s research aligns closely with previous Treasury research, including that done for the Henry Tax Review, which also concluded that retirement incomes will be adequate for most Australians.

Clearly, McKell’s ‘research’ has been manipulated to support Labor’s compulsory superannuation policy, rather than being based on an objective analysis of the evidence.

Advertisement

In any event, the Productivity Commission’s recently recommended holding a public inquiry into whether the superannuation guarantee should be lifted:

RECOMMENDATION 30: INDEPENDENT INQUIRY INTO THE RETIREMENT INCOMES SYSTEM

The Australian Government should commission an independent public inquiry into the role of compulsory superannuation in the broader retirement incomes system, including the net impact of compulsory super on private and public savings, distributional impacts across the population and over time, interactions between superannuation and other sources of retirement income, the impact of superannuation on public finances, and the economic and distributional impacts of the non-indexed $450 a month contributions threshold. This inquiry should be completed in advance of any increase in the Superannuation Guarantee rate.

Why not put McKell’s claims to the test and let the Productivity Commission settle the compulsory superannuation debate once and for all?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.