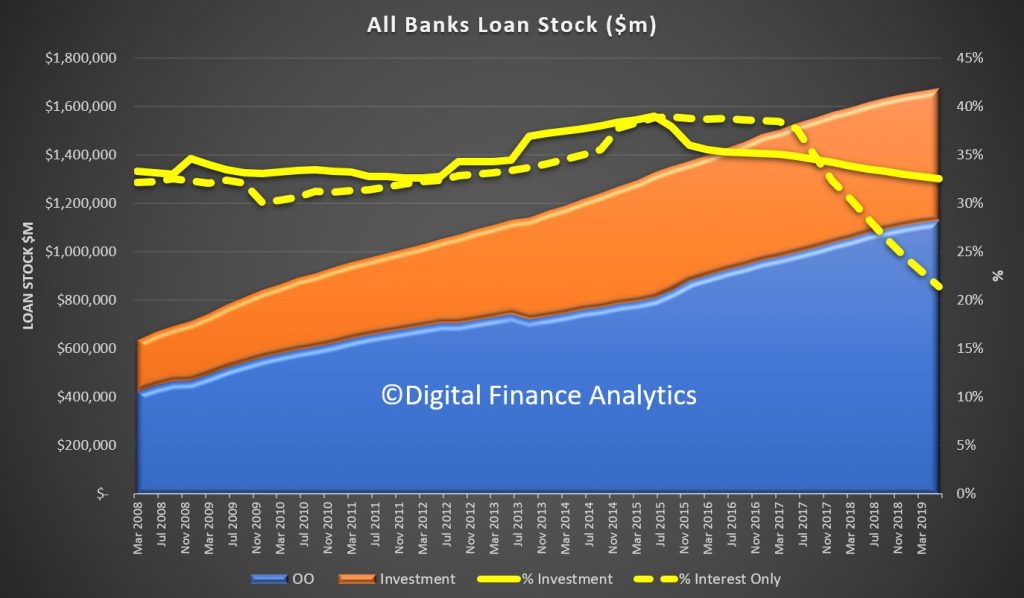

APRA released their quarterly property exposures data to Jun 2019 today. We can see some of the moving parts in the Industry, though only at an aggregated levels.

At the top level we can see the impact of APRA first imposing restrictions on investment lending in 2015, and later in 2017 on interest only loans. The subsequent loosening of standards which APRA introduced has yet to hit the statistics.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.