The DXY breakout continued to retrace Friday night. EUR fell too. CNY jumped on RRR cuts:

The Australian dollar roared higher against DMs:

It kept pace against EMs:

Advertisement

Gold was hit, oddly:

Oil rose:

Metals split the difference:

Advertisement

Big miners stalled:

EM stocks lifted:

Junk is rescued:

Advertisement

The Treasury curve flattened:

A daisy cutter fell on the bund curve:

Straya was a little bid:

Advertisement

Stocks too:

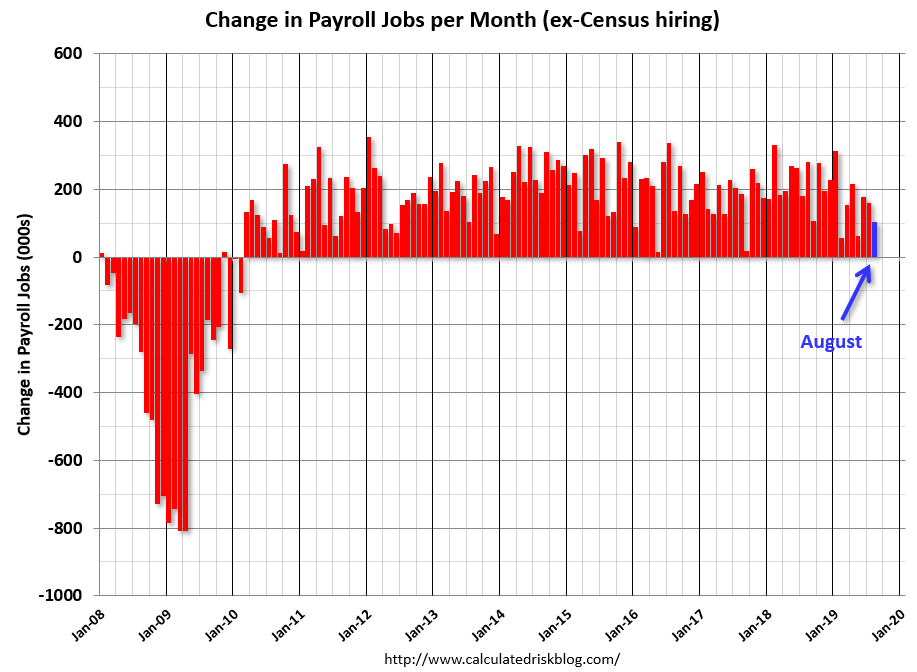

The big news was US jobs which were OK without being much else, via Calculated Risk:

Total nonfarm payroll employment rose by 130,000 in August, and the unemployment rate was unchanged at 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Employment in federal government rose, largely reflecting the hiring of temporary workers for the 2020 Census. Notable job gains also occurred in health care and financial activities, while mining lost jobs.

… In August, employment in federal government increased by 28,000. The gain was mostly due to the hiring of 25,000 temporary workers to prepare for the 2020 Census.

The change in total nonfarm payroll employment for June was revised down by 15,000 from +193,000 to +178,000, and the change for July was revised down by 5,000 from +164,000 to +159,000. With these revisions, employment gains in June and July combined were 20,000 less than previously reported.

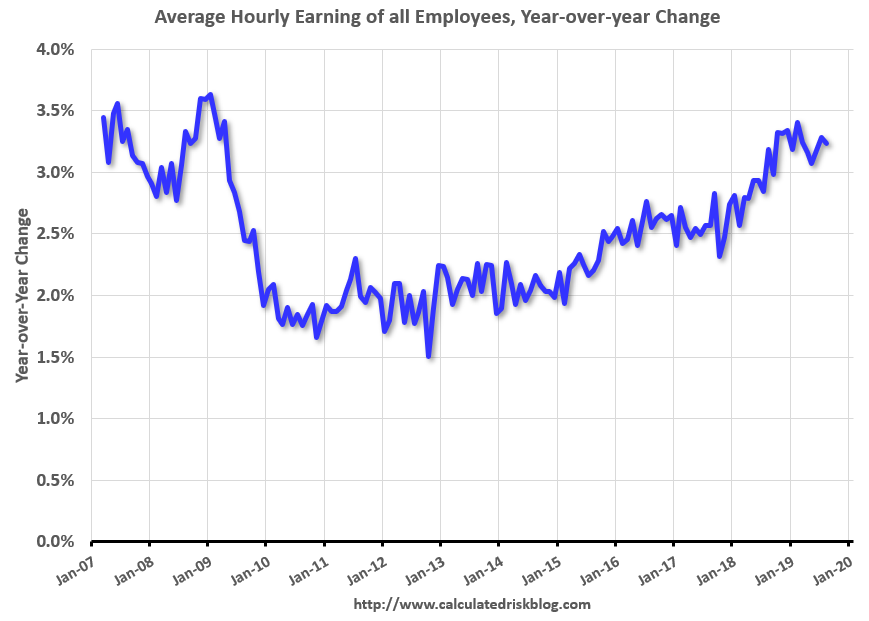

…In August, average hourly earnings for all employees on private nonfarm payrolls rose by 11 cents to $28.11, following 9-cent gains in both June and July. Over the past 12 months, average hourly earnings have increased by 3.2 percent.

Advertisement

Clearly softening. Wages will follow. And the Fed:

Federal Reserve Chairman Jerome Powell said the U.S. economy faced a favorable outlook despite significant risks from weaker global growth and trade uncertainty, and he cited the central bank’s turn toward providing more stimulus this year as an important reason for that outlook.

“The Fed has through the course of the year seen fit to lower the expected path of interest rates. That has supported the economy,” Mr. Powell said during a moderated discussion in Zurich on Friday.

China’s central bank announced on Friday that it will cut the required reserve ratio for all commercial banks, freeing up long-term funding of around 900 billion yuan (US$126 billion) that banks can use to increase lending and support government efforts to shore up the real economy.

The 0.50 percentage point cut in the amount of reserves banks are required to hold at the central bank will be effective from September 16, the People’s Bank of China (PBOC) said.

The required reserve ratio cut would boost bank’s lending capacity and more importantly lower their cost of capital received from the central bank.

The PBOC also cut the reserve requirement by an additional full percentage point for city commercial banks operating in Chinese provinces. The first half will take effect from October 15, with the second taking place a month later, China’s central bank added.

The European Central Bank is all but certain to approve new stimulus measures on Sept. 12 to boost an ailing economy, but the composition of its package is far from clear as a rift has opened between hawkish northern European policymakers and doves from the south.

Reducing the rate at which banks park excess cash at the ECB automatically lowers borrowing costs on a whole range of instruments, giving firms access to cheaper cash. This should then induce them to borrow more to invest, giving the economy a lift, with the ultimate hope that this would boost inflation.

Markets are positioned for a cut to -0.6% from -0.4%, but some policymakers in private are arguing for a smaller move so they can maintain some room to cut again, if needed. Deep in negative territory, rates are nearing their effective lower limit, where it’s cheaper for banks to hold cash in a vault. So there is only space for a few more cuts before further reductions cease to make economic sense.

Advertisement

So, we have:

a slowing US and modestly cutting Fed;

China chasing its slowdown with overly slow easing;

a dithering ECB as its economy enters recession.

In short, all three central banks are behind the curve. But China and Europe are further behind. The sum total of this is not bullish for the Australian dollar given Europe and China leading the slowdown is commodity bearish and USD bullish, and having all central banks at once behind the curve is also a negative risk off scenario for the AUD.

Meanwhile, we had better trade war news in no news, but that’s not going to stop this:

Advertisement

It doesn’t appear there’s anything the Trump administration has done to improve this sentiment. Right now, it’s the more encouraging news and messaging from China that’s the cause of that optimism.

But what forced this sudden change in the rhetoric from Beijing?

It’s not the new round of tariffs that went into effect; we’ve been playing the tit-for-tat tariff war for more than a year. It’s not the economic reports; they’ve been a little too mixed lately to force any dramatic moves. It’s not even the decision by Hong Kong administrator Carrie Lam to fully withdraw the controversial mainland extradition bill; it’s still not clear that the Hong Kong unrest would be affected in any way by a trade deal.

Given the timing of the change in tone, it seems more likely that what’s making the difference is a realization on both sides that there’s another way this trade war could end – and that possible ending is one the U.S. is very unlikely to lose.

That alternate ending is summed up in one word: decoupling.

The decoupling push is quite different than any U.S. efforts to get China to open up more of its economy to American companies. Instead, it focuses on reducing America’s extremely heavy reliance on China for so much of its manufacturing needs.

That is precisely the hegemonic struggle that MB sees underway and exactly what US hawks hope to achieve. We think it is already unstoppable given it is an unacceptable risk to global supply chains.

So any cessation in trade conflict will be brief and unhelpful anyway. Not Australian dollar bullish.

Advertisement

Then we have Hong Kong. Removal of the extradition bill was a breakthrough but the following from Geoff Raby sums up the problem:

Xi Jinping will want the demonstrators off the streets well before the October 1 celebrations of the 70th anniversary of the establishment of the People’s Republic of China. This was to be his grand moment, and a burning Hong Kong would entail an intolerable loss of face. The resilience of the people on the streets of Hong Kong may finally have convinced Beijing that compromise would be a better outcome than tanks at Hong Kong’s major intersections during the 70th anniversary.

However all of this is resolved, following this summer of discontent, Hong Kong will never be the same again; 2046 has collapsed into the present. Beijing will do whatever is necessary through political interference, media and digital control, and undermining Hong Kong’s independent judiciary and academia to ensure this never happens again.

Everybody in Hong Kong knows this so it’s not good enough to withdraw the bill. Those who have protested have all been photographed and logged. If the protester’s other demands for exoneration for rioting are not met then they are basically signing their own death warrants by stopping now. Not Australian dollar bullish.

The semi-prorogation didn’t “backfire”: it flushed out his hardcore opponents and allowed him to expel them. He knew he would have to do something drastic at some stage and there was no way that those committed to derailing his plans would ever have been allowed to stand under Tory colours at the election. His party was already split de facto, if not de jure; he was always leading a minority government in all but name. The sackings merely formalised this.

…In any case, the Prime Minister needs a party with a single message: every candidate will have to sign up to his plans. This will be the only way that he can fight off the Brexit Party. If he wins, perhaps with a slender majority, Johnson will need to be able to count on every one of his MPs.

In the first few hours after Johnson called for an election, when it became clear that MPs would seize control of Parliament, Remainers were elated: they thought they had crippled their enemy.

But they are now realising, to their horror, that their victory may be ephemeral. The MPs’ vote may not really matter; the PM is ready for an election, and he has in fact guaranteed one by making it clear that he doesn’t have a technical majority any longer. Paradoxically, weakness is strength for Boris. He might have preferred to go to the polls after Brexit, but the present path comes with its own advantages.

In short, three of the four horsemen of MB’s end of cycle apocalypse are still in play. The fourth, oil, is simply the trigger as growth slows.

Advertisement

Nothing I see above prevents that from continuing and, no, the Australian dollar has not bottomed, in my view.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.