The unsackable chairman of Australia’s single most important regulator has done it again. APRA released its monthly credit data late Friday and the results are very much sackworthy.

To wit, it’s not that growth is suddenly off the hook. Rather, it is that the key data set for understanding the entire previous boom and bust cycle just collapsed into opacity and farce.

Here are the raw numbers:

ANZ

CBA

MQG

NAB

WBC

BOQ

BEN

SUN

Jul-19

87729

155406

16698

114311

185615

12054

13587

12355

Jun-19

76774

133761

12643

104660

153525

11340

12811

11756

May-19

77473

133400

12532

104681

153096

11320

12932

11694

Apr-19

78018

133093

12465

105036

152588

11332

12851

11697

Mar-19

78470

132904

12372

105379

152393

11333

12772

11724

Feb-19

78936

132916

12320

105645

152368

11352

12649

11755

Jan-19

79366

132960

12223

105757

152323

11364

12597

11745

Dec-18

79790

133045

12103

105869

152453

11366

12554

11784

Nov-18

80187

132812

11938

106081

152318

11534

12538

11738

Oct-18

80470

132705

11791

105982

152432

11318

12467

11700

Sep-18

80916

132539

11602

105750

152770

11346

12416

11622

Aug-18

81260

132838

11407

105688

152844

11336

12296

11579

Jul-18

81519

132764

11091

105512

153034

11347

12206

11579

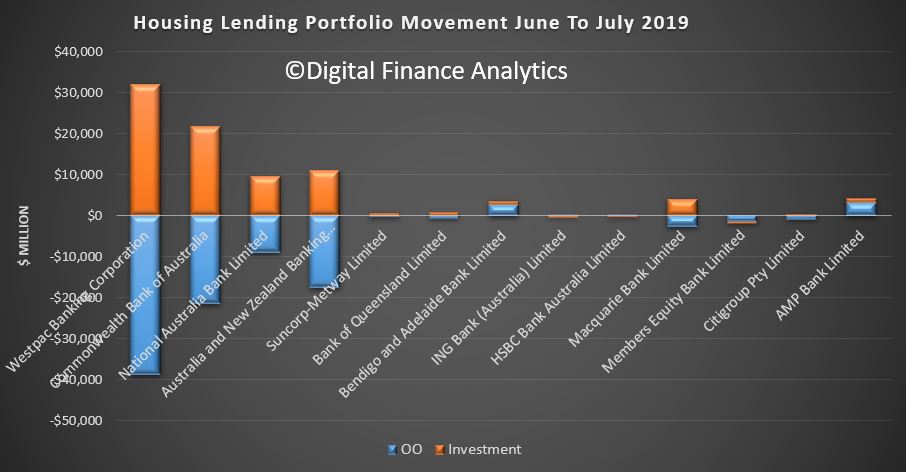

If you have a look at that top line you will notice that suddenly investor loans have skyrocketed at every major bank. It looks like this:

Advertisement

And by bank:

Somehow, while Wayne Byers has been busy with whatever it is that he does, he failed to teach his staff, or their charges in the banks, how to tick the box that read “investor mortgage”.

Advertisement

As a result, WBC has just seen its investor loan book skyrocket by 20% and system stock is 13.5% higher than previously thought, for instance.

This lost $80bn in high risk, highly rehypothecated lending fundamentally alters the risk profile of the banking system and effectively adds two years worth of frenzied investor lending growth to the last cycle.

Had this data previously been correct, the pressure on APRA to act on the bubble over the last cycle would have been overwhelming. The disgraced Wayne Byer’s has essentially just confessed that he had no idea what he was doing and was wearing a blindfold when he did it.

Advertisement

Martin North suspects conspiracy:

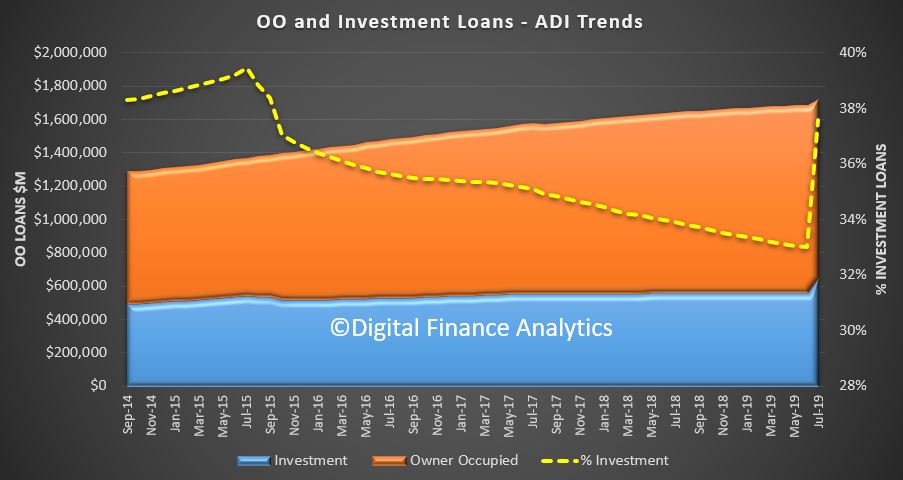

APRA released their monthly statistics to end July 2019. They are rubbish, in terms of trend tracking because thanks to a revised method of data capturing the value of investment lending rose considerably, offset by a fall in owner occupied loans.

The RBA said that there were reclassifications of loans between owner occupied and investment, plus off shore and onshore borrowers.

The changes from last month are therefore considerable. Westpac made the largest switch with $40 billion dropping from the owner occupied side of the house.

The overall portfolio mix by lender changed less.

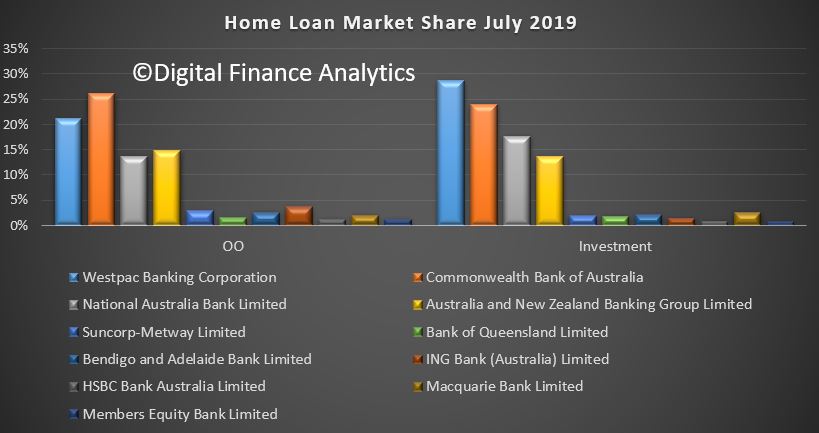

But the proportion of investment loans jumped to 37.6%, compared with 33% the previous month. This means that banks ARE EVEN MORE EXPOSED to investment lending than had been previously reported!

Given the size of the changes, it is impossible to tell what is happening within individual lenders (which is convenient?). So we will have to start from this point as a series break.

For the record, the value of owner occupied loans fell 5% from $1.13 trillion to $1.10 trillion, while investment loans rose by 16% from $557.3 billion to $647.4 billion.

Total lending rose from $1.68 trillion to $1.72 trillion, up more than 2%. But this is meaningless.

Frankly this is a joke, and I feel it is designed to hide, not inform. The investment debt bomb just got bigger!

I doubt its deliberate. This is typical of the titanic blundering that MB has come to expect as the norm across Australia’s entire governance system, let alone an arm that is required to use basic arithmetic.

The good news is that some pressure is being brought to bear upon Byers over the new rebound in mortgage lending that he unleashed when he rashly slashed macroprudential and interest rate buffers under pressure from Treasurer Josh Recessionberg, banking oligarchs and the Australian Financial Review. Via that discombobulated organ on the weekend:

Advertisement

Alex Joiner, chief economist at IFM Investors, said a weak economic growth figure on Wednesday for the June quarter would force the RBA to consider “bringing forward” another rate cut, at a time when he had witnessed more buyer exuberance at auctions.

“The early housing trends we’ve seen are concerning and if the momentum continues through spring when there are more listings, the Council of Financial Regulators [CFR] would need to talk about reimposing macroprudential controls as mortgage rates fall towards 2 per cent,” Dr Joiner said.

AMP Capital chief economist Shane Oliver said…”Housing started to stabilise after the election, and in Sydney and Melbourne it feels like some of the months we saw through the property boom.

…”I suspect they may have to toughen up the macroprudential controls again if Sydney and Melbourne get out of hand.”

Alas MB holds little hope for any imminent move by APRA towards tightening. After being napalmed by the Hayne Royal Commission, Wayne Byers only continues in his position thanks to the patronage of Josh Recessionberg who has clearly set about reflation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.