US existing home sales surprised to the upside, rising by 1.3% in August, taking year-ended growth higher to 2.6% from 0.6%. Housing demand was looking weak at the end of 2018, but now it seems to be turning around, largely in response to lower bond yields and mortgage rates. We think that housing demand recovery is a very encouraging sign for the US economy and value investing. In our recent articles “Tail risk or apocalypse” dated 5 September 2009, and “Uncorrelate me” dated 30 August 2019, we argued that:

Inversion of the yield curve foreshadows underperformance of passive strategies, because of lost diversification benefit, or heightened portfolio correlation risk.

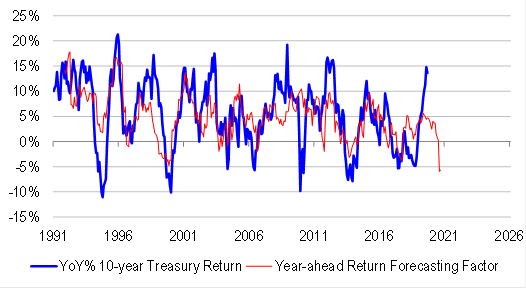

Both bonds and equities are priced for negative real returns across various horizons, making the valuation backdrop for passive investing quite poor.

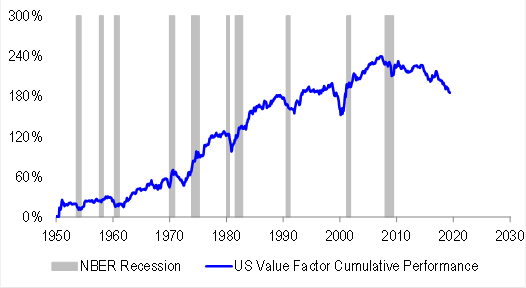

From a factor investing perspective, value investing could make a comeback, because as the laggard in recent years, it has now become diversifying factor. In contrast, momentum and quality have become incredibly highly correlated, meaning that there is no more diversification benefit between these factors.

Value investing could do well, even in a hard landing scenario, if this cycle follows two recessionary paths in the 1970s, or the 2001 tech-bubble bust. What made these episodes unique was the absence of widespread de-leveraging pressure.

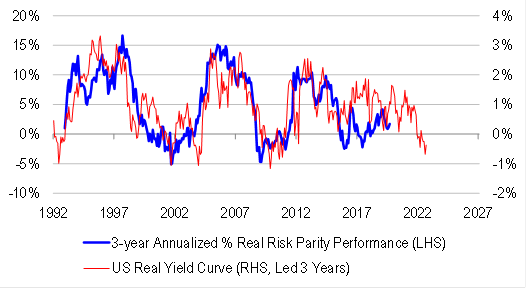

Value investing could do well in a reflationary scenario, because value factor performance has become incredibly highly correlated with the slope of the yield curve.

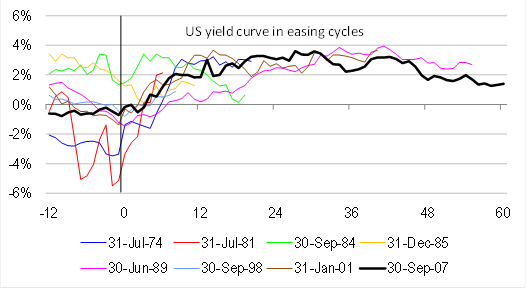

Curve steepening is very likely as the Fed cuts rates, and as bonds sell off. Bonds are vulnerable to selling off given that term risk premia are negative (ie the compensation for getting one’s rate forecast wrong is negative), and that reflation is coming into view, as evidenced by recovery in mortgage demand.

With all of these arguments in mind, we are encouraged by the fact that US home sales are now corroborating the green shoots we saw in the Fed’s Senior Loan Officers’ Survey with respect to mortgage demand. We are encouraged by the recent strength of US retail sales, despite slowing labour income growth, because it reflects stronger wealth and credit effects. We are encouraged by the fact that widespread de-leveraging on behalf of the household sector is unlikely, because mortgagees are happy to take on more credit at low rates. Recovering credit demand and home sales support the narrative that bond yields need to rise as a result of positive news. It is consistent with curve steepening. Also, the absence of de-leveraging pressure is favourable for value, because it allows us to say that fundamentals are able to drive asset prices, rather than the other way around.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.