Last month’s improved signal has been very short lived with the Index growth rate back firmly in negative territory where it has been stuck for eight of the last nine months. The major contributors to the sharp fall in the growth rate over the month came from substantial drags from the share market, commodity prices and dwelling approvals. The relapse confirms the consistent signal from most of those preceding months that the economy will continue to be operating at a below trend growth pace into late 2019 and early 2020.

Westpac expects that the economy’s growth pace will pick up from the 2% annualised pace in the first half of 2019 to 2.5% in the second half and hold at around that 2.5% pace in the first half of 2020. With trend growth rate assessed as 2.75% that forecast is broadly in line with the signal from the Leading Index.

The Leading Index growth rate has deteriorated over the last six months from –0.15% in March to –0.35% in August. The main components driving the 0.2ppt shift have been a further weakening in dwelling approvals (–0.24ppts); a sell-off in commodity prices (–0.19ppts); slower growth in monthly hours worked (–0.10ppts); and a softening in the Westpac-MI CSI expectations index (–0.08ppts).

Partially offsetting those moves were positive contributions from ASX (+0.22ppts); the yield curve (+0.18ppts) and Westpac MI Unemployment Expectations (+0.03ppts).

The Reserve Bank Board next meets on October 1. The minutes of the Board’s meeting in September highlighted the labour market; housing; and GDP growth as key factors in the decision process. That is in the context of a world where downside risks to the global economy have intensified and central banks are generally expected to continue to ease financial conditions.

The Board’s assessment of the labour market emphasised that Australia should be aiming at lower unemployment and underemployment rates while the upward trend in wages growth appears to have stalled. There were improving prospects for housing markets although the contraction in residential construction activity was likely to continue to weigh on the economy.

Markets are expecting the next rate cut from the RBA in November whereas Westpac, at this stage, continues to see no reason why the Board should delay the move with a cut in October looking to be the better option.

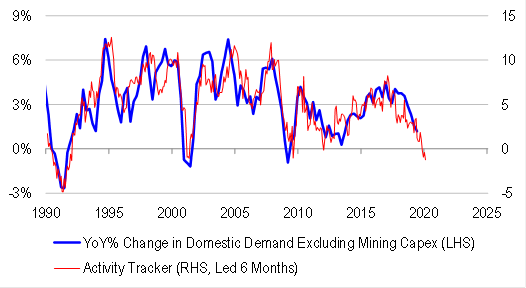

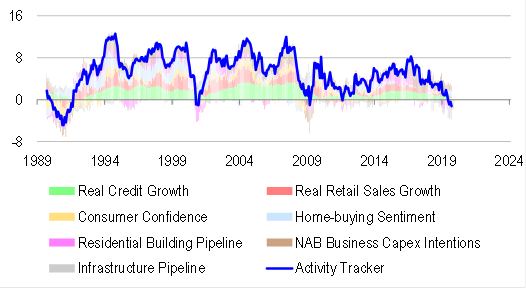

I prefer the Credit Suisse indexes which are pointing unequivocally down:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.