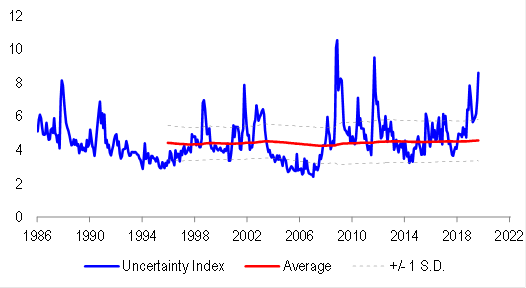

Via Damien Boey at Credit Suisse:

Equities are selling aggressively and bonds are rallying on the back of recent escalation of trade wars. Investors are behaving as if the end of the world is nigh. But is this really the case?

Via Damien Boey at Credit Suisse:

Equities are selling aggressively and bonds are rallying on the back of recent escalation of trade wars. Investors are behaving as if the end of the world is nigh. But is this really the case?

The full text of this article is available to MacroBusiness subscribers