The gap between male and female superannuation savings have once again been labelled one of Australia’s greatest inequalities:

Almost three out of four “Millennial” women – those born between 1980 and 2000 – told a survey of 1000 people the super system was not designed to support women.

Only 25 per cent of women this age believe they will be able to retire comfortably, compared with 44 per cent of Millennial men…

Hobbs, an economist with a financial-services background who has worked for the United Nations as an expert on the financial inclusion of women, says the results of the survey should be a “clarion call for our federal politicians to elevate womens’ retirement outcomes to the forefront of the superannuation reform agenda”.

For those approaching retirement, aged 55 to 64, the median super balance for women in 2015-16 was $96,000, compared with $166,000 for men, Australian Bureau of Statistics figures say.

“The super system magnifies a lifetime of financial discrimination and inequality for women…

“The super system needs to take women more seriously,” Hawker says. She would like to see carer roles compensated in some way – perhaps with the payment of the superannuation guarantee on the Commonwealth parenting payment.

Hobbs says women continue to undertake the majority of unpaid care work and this includes domestic work and taking care of children, the elderly, or a family member with a long-term health condition or disability. When women are engaging in unpaid work, they do not earn superannuation.

Let’s get one thing straight. The inherent bias against women’s superannuation stems from the inequitable way that concessions are distributed, which disadvantages lower paid workers irrespective of gender.

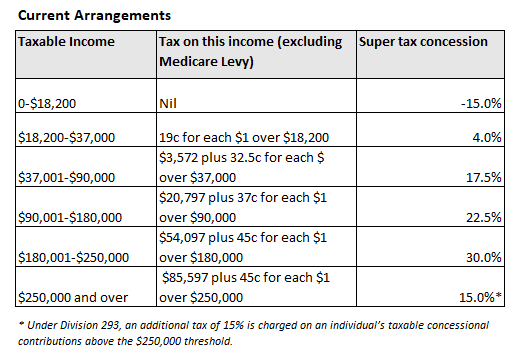

Under current arrangements, superannuation contributions/earnings are taxed at a flat rate of 15%. Accordingly, those on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions:

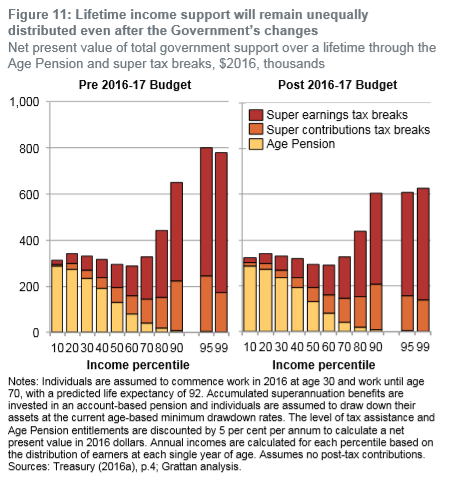

Division 293 remedies the situation for those very high income earners above $250,000. But even then, the lion’s share of superannuation concessions still flow to the highest income earners, whereas the lower income earners continue to be disadvantaged by the system, as shown in the next chart from the Grattan Institute:

Since women typically earn less then men – because they tend to work in lower paid professions (e.g. nursing and teaching), work part-time, or take time off from working to raise children – they accumulate much lower superannuation balances.

The first best solution to this problem is to reform the superannuation system to make concessions more equitable and sustainable.

In particular, the 15% flat tax on contributions/earnings should be replaced with a flat-rate refundable tax offset (e.g. 15%). This way, everyone that contributes to superannuation would receive the same concession, the system would be made progressive, and lower income earners – be they male or female – would get a better deal.

The 30-year old rule that stops earnings under $450 from an employer in a month from attracting superannuation should also be removed.

One thing we definitely do not want to see is band-aid solutions like raising the superannuation guarantee (compulsory super) from its current 9.5% to 12% without first reforming the way that contributions/earnings are taxed. All this would do is heighten inequities already present in the system. It would also rob lower paid workers (and women in particular) of much-needed disposable income and worsen the long-term sustainability of the Budget.

As an aside, the growing concerns over the disparity between male/female superannuation and earnings is largely a non-issue. We are family units whereby husbands/wives pool their financial resources – both incomes and savings – and share workloads, be it paid or domestic.

Moreover, when couples divorce, financial resources are split-up and distributed among the spouses, including superannuation savings.

Instead of fighting fake gender wars, policy makers should focus on eliminating poverty, irrespective of gender.