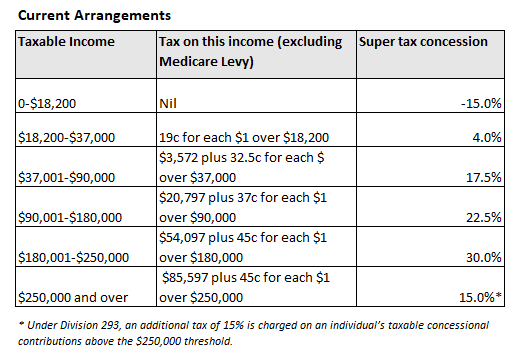

One of the biggest knocks on Australia’s compulsory superannuation system is that because of Australia’s flat 15% tax on contributions, those on lower incomes receive minimal concessions (or are penalised), whereas those on higher incomes receive the biggest tax concessions on contributions:

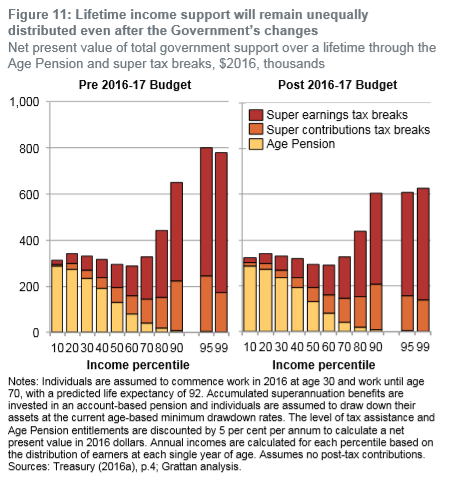

Division 293 remedies the situation for those very high income earners above $250,000. But even then, the lion’s share of superannuation concessions still flow to the highest income earners, whereas the lower income earners continue to be disadvantaged by the system:

Reflecting the above inequities, Fairfax today reports that wealthy postcodes like Palm Beach have far higher average superannuation balances than poorer postcodes:

Palm Beach residents have some of the largest nest eggs in the country, with average retirement savings worth more than $850,000 each. That’s equivalent to the combined average superannuation balances of 22 less wealthy areas…

Sydney’s largest stashes of super are in Palm Beach ($859,572), Darling Point ($647,555), Vaucluse ($488,436), Hunters Hill ($481,387), Mosman ($469,867) and Northbridge ($468,423).

In 2016/17 the average super balance for a man sat at $146,420 and for a woman at $114,350…

Palm Beach was Sydney’s highest average income area in 2016/17…

Grattan Institute Household Finances Program Director Brendan Coates said… “Half of all the [super] tax breaks go to the top 20 per cent of Australians by income… We know wealthier people put in more and those tax breaks need to be wound back.”

Superannuation is reducing the age pension bill but it is a net cost to the federal budget because the tax breaks reduce government revenue and are a larger drain on the budget than the age pension savings, Mr Coates said.

“That was the view of the Henry Tax review when it said no to raising compulsory super beyond 9 per cent,” Mr Coates said.

An obvious solution to improve both equity and Budget sustainability would be to abandon raising the compulsory superannuation guarantee and instead replace the 15% flat tax on contributions/earnings with a flat-rate refundable tax offset (e.g. 15%). This way, everyone that contributes to superannuation would receive the same tax concession, the system would be made progressive, and lower income earners would get a better deal.

It’s a no-brainer.