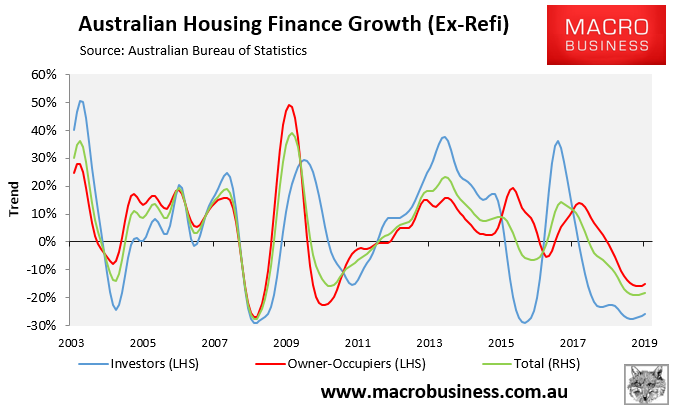

Yesterday’s Lending to households and businesses release from the ABS revealed that total mortgage lending (excluding refinancings) began to rebound in June; albeit it was still down a hefty 18% over the year in trend terms, driven by an epic 26% crash in investor commitments, whereas owner-occupied commitments also fell by 15%:

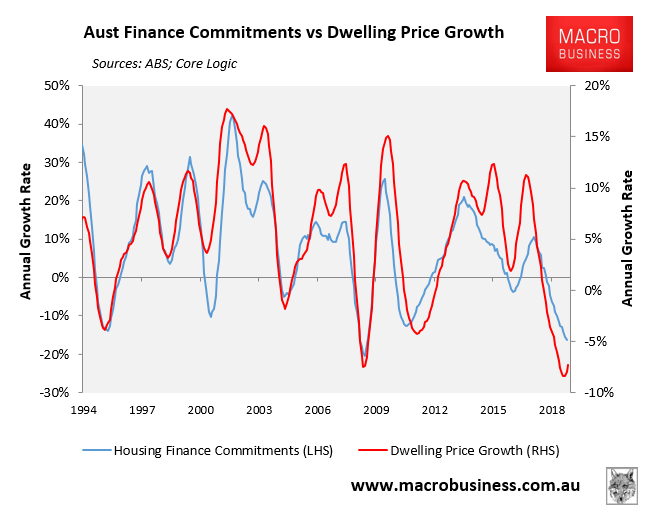

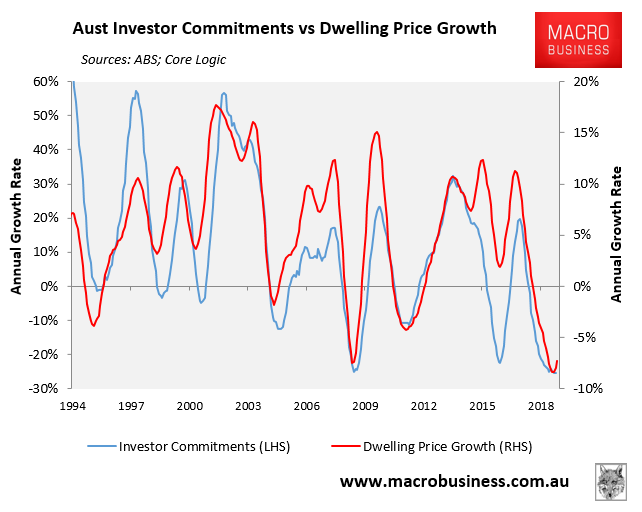

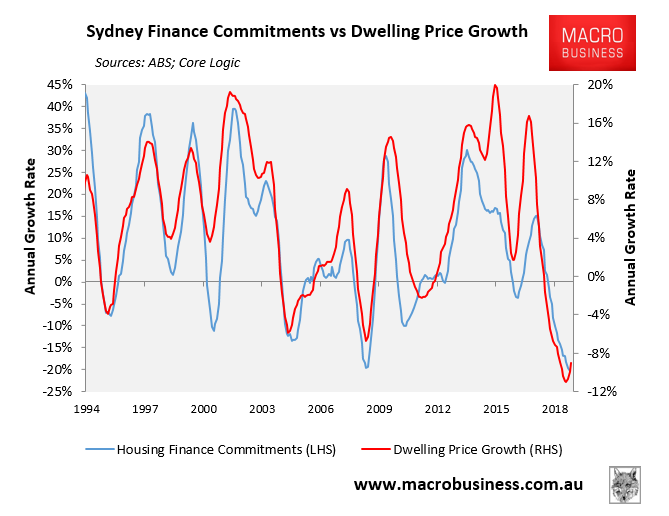

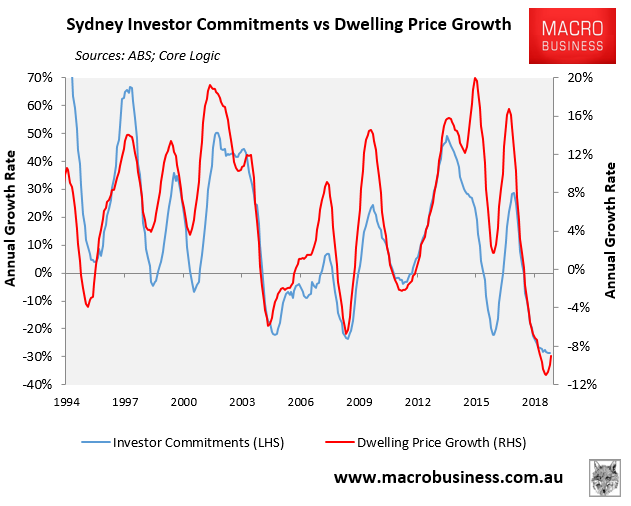

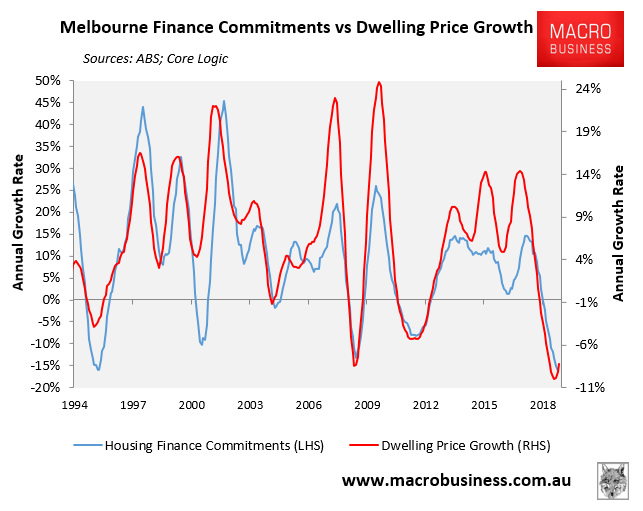

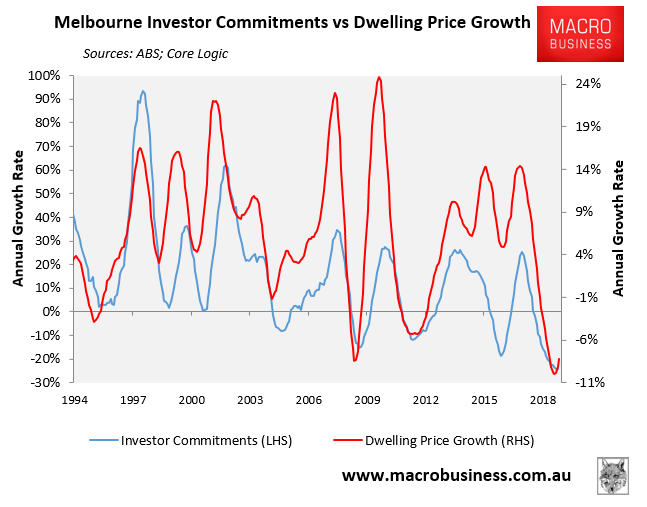

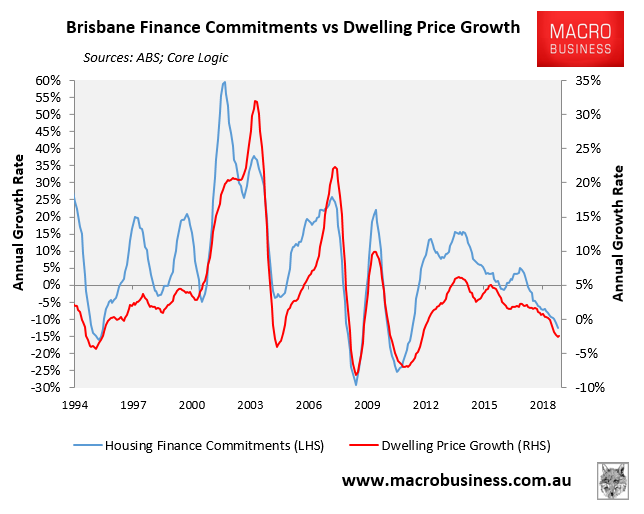

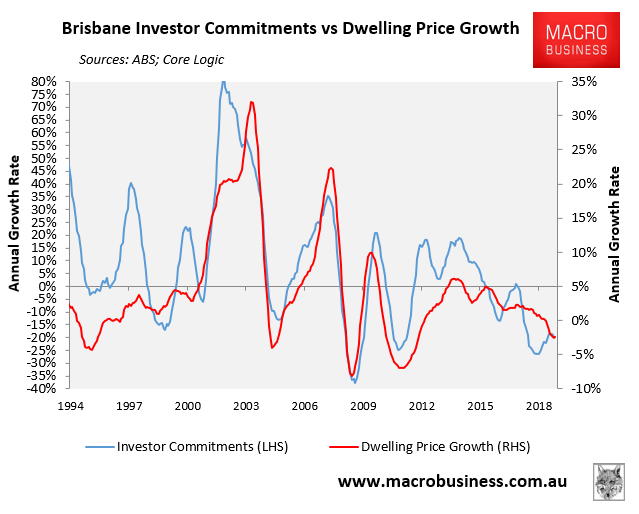

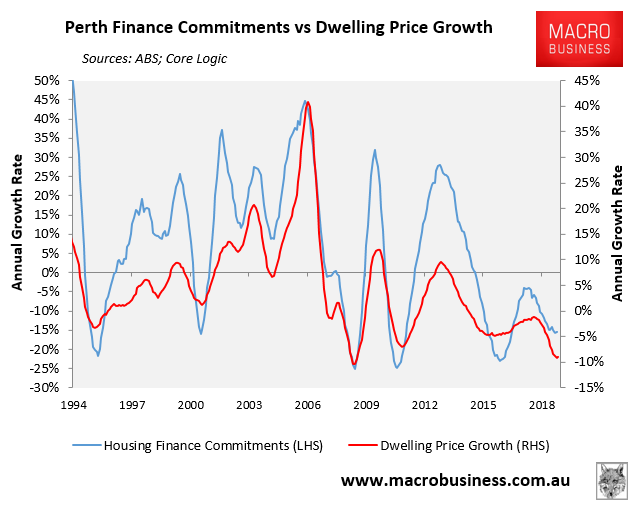

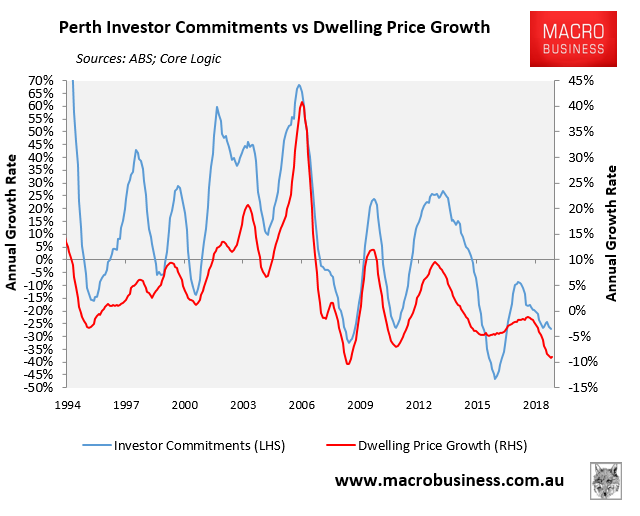

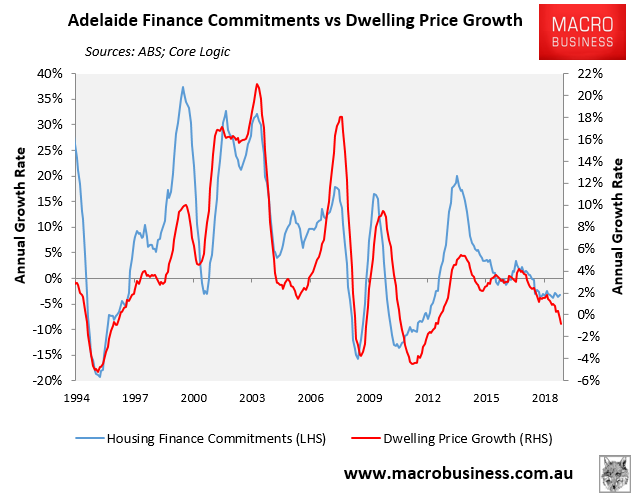

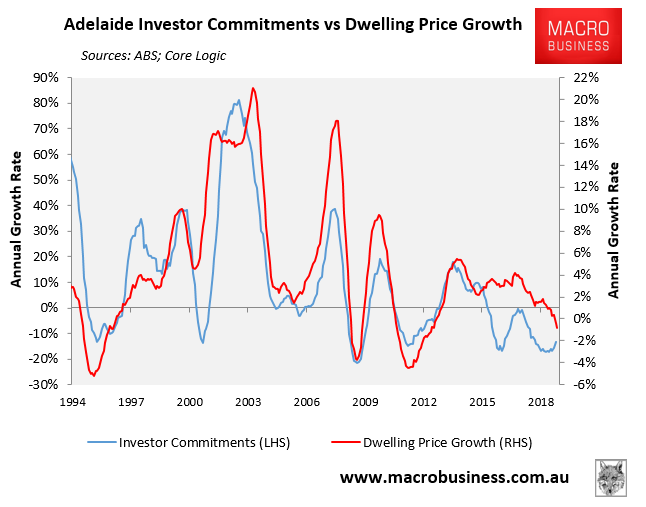

As regular readers of MB will know, we consider the flow of housing and investor finance commitments to be premier indicators for dwelling value growth. This view is based on the incredibly strong historical correlation between finance and prices, as illustrated by the next charts:

As you can see from the above charts, investor and housing finance growth as well as dwelling price growth has crashed particularly hard across Sydney and Melbourne, but is also weak across the other major capitals. However, there are early signs of improvement, at least on a national level, as shown by the first chart.