Don’t Blame the Fed or Trade – It’s the Fundamentals

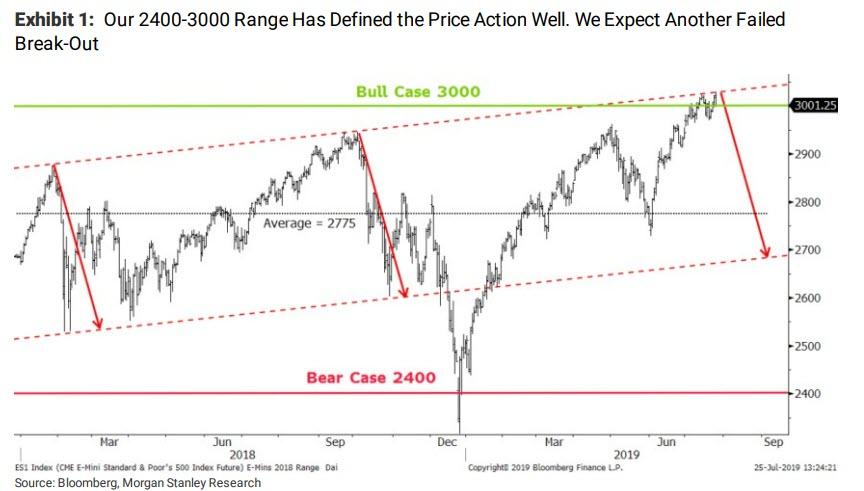

Rarely has the adage “Don’t fight the Fed” been more apropos than over the past 18 months. In 2018, the Federal Reserve’s aggressive tightening contributed to a bear market for most stocks, while this year’s equally aggressive dovish pivot has resulted in a new bull market for some. Since our call 18 months ago for a multi-year consolidation in global equities, the average global stock and index is flat to down 10%, while the leading S&P 500 Index is now barely up with a lot of intermittent ups and downs. In short, thanks to the Fed’s policy shift, we’ve seen a consolidation that leaves us at the high end of our expected range.

Advertisement

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.