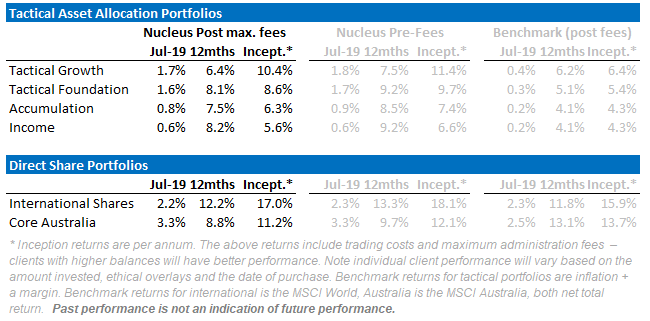

July added another month of good performance to the share and bond market rallies that have driven markets higher throughout 2019. Our tactical portfolios continue to perform well vs other super funds:

The issue we are facing in most of our portfolios is that we are positioned for negative outcomes, which means that we tend to lag the market on strong up months and then make back the returns in weaker months. Much of our performance over the last six months came from a successful trade on bonds, and most of the bond upside has already been achieved – we have switched significantly into cash which leaves us at risk of underperforming if markets rise strongly. This is not our expectation.

Assets are priced for perfection and we are expecting conditions to be far from perfect: corporate earnings are clearly weakening globally, inflation is almost nonexistent, central banks know that they are out of ammunition and are begging governments to borrow, largely governments are ignoring them. The one major exception is the US, although borrowing to give companies and the richest 1% a major tax cut is not what central bankers would have preferred.

This leaves most of the world relying on US growth to lift exports and demand enough to offset their own government’s failure to act. And with US growth now slowing after the sugar hit of tax cuts last year a range of countries, particularly in Europe, are being exposed as having no actual growth plan other than hope that someone else will do the heavy lifting.

On top of this we see four major risks in the short term that threaten a decline into global recession:

- trade war deterioration;

- the Hong Kong end game;

- a hard Brexit, and

- and oil price crash triggering a US debt and equity shakeout.

Australian Outlook

Australia is in a similar position to Europe. The economic plan in Australia seems to be aiming for a short term fillup that will be enough to keep growth ticking over until some form of economic luck strikes – maybe more Brazilian mining disasters to spike the iron ore price higher, or China to unleash another massive capex stimulus program, or more earthquakes to shut down nuclear reactors in Japan to send coal and gas prices soaring.

At the moment Australian government’s fillup plan is to try to re-ignite the housing boom by convincing the world’s most indebted consumer to borrow more – a short term win for the Australian economy at the cost of longer-term growth.

This has a number of obvious pitfalls, but we need to acknowledge it may be successful – economic luck has been on Australia’s side for the last 15 years and so maybe Australia will get lucky again.

The danger is that Australia doesn’t get lucky, or more concerning is unlucky.

Ignoring outside factors (for the moment), there are three key factors we are following that will tell us whether the government’s short term fillup is going to work:

Factor 1: Australian Credit growth:

The Royal Commission into banking reversed the credit boom and was enough to see house prices down around 10%, even while most other factors affecting house prices were still positive.

If I am too bearish (particularly in the short term) and the Morrison government manage to get the already over-levered Australian households to take on more debt, this is where you will see the effects first.

On the regulatory front, the Westpac v ASIC responsible lending court case win for Westpac is a boost for easy lending conditions. ASIC public hearings into responsible lending over the next few months will be key to how easy the lending conditions will be.

Factor 2: Unemployment

There is not enough space here to go into the detailed links between house prices and unemployment. Indicatively, during the 2012 to 2017 housing boom years, the Perth market faced largely the same factors as Sydney/Melbourne except for (a) slightly weaker population growth and (b) rising unemployment. And Perth property prices fell more than 10% while the rest of Australia boomed.

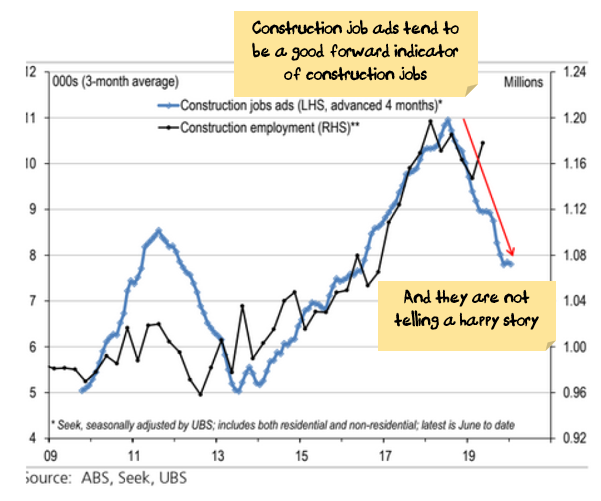

We are expecting considerable job losses in the construction sector.

Source: ABS, Seek, UBS

Add to this job losses from Victorian and NSW state government austerity.

Any global shock (trade wars, recessions, debt crises) is likely to be transmitted to the housing market through higher unemployment.

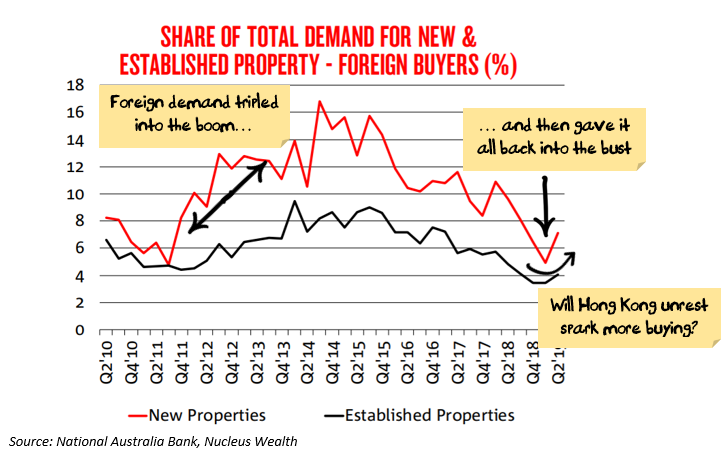

Factor 3: Foreign Buyers

Foreign demand was key to both the boom and the bust:

China cracking down on its capital account and deteriorating relations between Australia and China suggests foreign investment will remain low.

The key upside question is whether Hong Kong unrest sees increased demand in Australian property.

Asset Allocation

The real question for asset allocation is what to do in the meantime. The current government has at least three years in power, plenty of scope to increase government debt to support the housing sector in novel ways and no compunctions about trying to convince Australian consumers to borrow even more.

Blowing the property bubble meaningfully larger is probably beyond the Australian government, but arresting the fall in prices seems likely.

The risk is some sort of global shock or broader economic downturn. Australia has already “broken glass in case of emergency” to prop up the housing market and many of the policies that could be employed in a crisis have already been employed – meaning that in the event of a genuine crisis the downside is going to be more pronounced.

Which leaves a measure of conflict in asset allocation – do you try to ride a short term stabilisation in the Australian economy and run the risk that any global crisis is likely to be devastating? Valuations have made part of the decision with the Australian market looking increasingly expensive.

So where does an asset allocator turn? In 2018 with a slowing Australian economy, stagnant wage growth and ten-year government bond yields of 2.8% we felt being overweight bonds was an easy decision (investors make money on bonds when yields fall).

At the time we were one of the only voices expecting rate cuts in Australia. Now the first two rate cuts have occurred and further cuts are a consensus opinion.

While we were expecting Australian ten-year bond yields to fall to these levels (1%), we weren’t expecting them to fall so quickly – the last 8 months have been dramatic.

Keep in mind that the Reserve Bank of Australia has an inflation target of 2-3%. At current yields, the bond market is suggesting that it will not meet that mandate for the next ten years. Which, in the context of the European and Japanese examples, anemic wage growth, world-leading private indebtedness and an overvalued housing market, is probably a reasonable assumption – unless something changes.

We are of the view that stagnant growth is going to be on the menu until we see governments spending money. And probably “helicopter” money. Given the current state of economics, that will probably take some sort of reasonably large economic crisis. Until then we expect more of the same – slow growth and a grind lower.

As the bond yields have fallen we have been taking profits, although we remain overweight.

The low yields present an asset allocation quandary. I was hoping that by this stage we would have seen equity prices that were more reasonable, giving us the opportunity to switch out of our bonds and into equities. But equities are looking expensive. Not irrationally expensive, but certainly more expensive than we would have thought given the uncertain and low growth outlook. So are now holding lots of cash, looking for the right opportunity.

July Performance

While our portfolios were similar in performance for July to market portfolios, over the last four months they have been showing the signs of being overly defensive, underperforming. We are comfortable with the view that the defensive position is warranted – if markets shoot higher then we will underperform but we think the trade-off is warranted given that downside protection is more important at this point in the cycle than chasing stock markets higher:

Outlook

Australian shares are still considerably more expensive than most international comparisons with poorer growth expected. We retain large cash and bond balances to hedge against volatility and in the expectation that capital protection will be important during 2019.

Our key focus is on:

- Chinese growth, gauging the extent of the slow down and the policy response to the trade war, as well as Hong Kong

- Gauging the damage that a Boris Johnson led hard Brexit might cause

- Trying to work out how sustainable the effect of the Australian election will be on house prices

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.