By Chris Becker

A bath of blood on equity markets overnight as the US/China trade war deepens with US stocks falling around 3% across the board, now wiping out all the nominal gains for the year. It was a run to safe havens instead, as gold surged alongside Yen while US Treasury yields plummeted to a near three year low with the Aussie 10 year now at a record low below the 1% mark. In economic news, the ISM Services index went to a three year low alongside the European PMI.

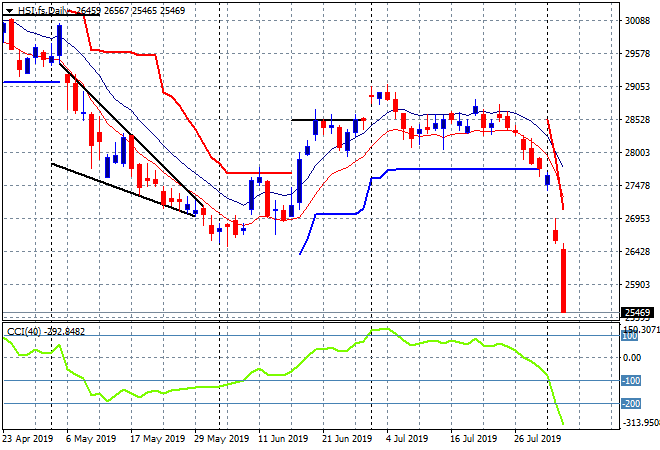

Looking at the action on Asian markets yesterday, where the Shanghai Composite fell over 1.6%, building on its woes from Friday closing 2821 points while the Hang Seng Index gapped down again, dropping a further 2.8% to 26151 points as domestic concerns over strikes and protests weighed. This is far more than expected and puts it on track to take out the January lows at 25000 points and then a possible overshoot to the September 2018 lows at 23000: