Markets are in a much better mood as the Christmas tariff surprise by Trump is alleviating shorter term concerns over the US/China trade war. Tonight however, the focus will be on Europe as the latest GDP print for the EZ will follow last night’s dreadful German ZEW Survey. In Asia today, the slump in Chinese industrial production figures saw the Aussie dollar drop lower while gold and other undollars hung on following the recent return to strength for King Dollar.

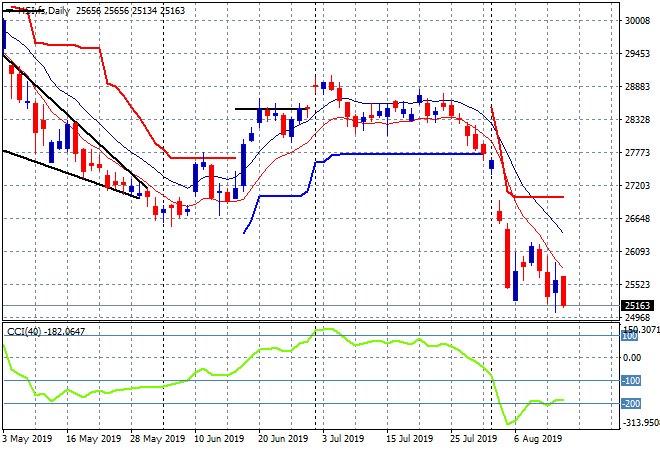

The Shanghai Composite has rebounded following the tariff abatement, closing 0.4% higher to 2808 points while the Hang Seng Index is putting in a scratch session, although is selling off going into the close, currently down 0.1% to 25265 points. This keeps it near the recent daily lows from last week, with the daily chart spelling a lot of trouble ahead if it breaks below 25000 points proper:

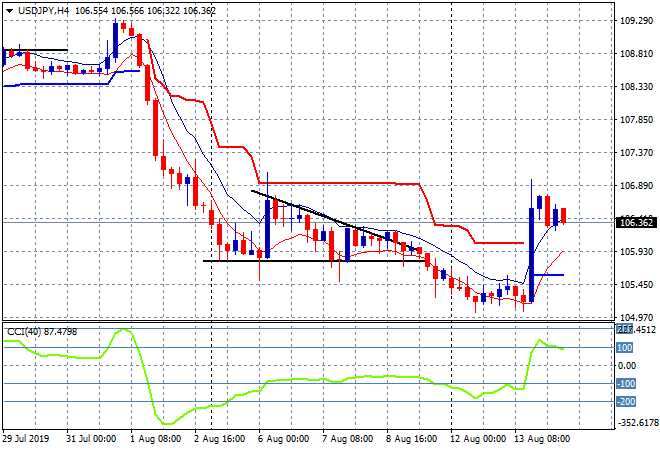

Japanese share markets did much better as expected as Yen sold off sharply overnight with the Nikkei 225 clawing back its previous losses to close 1% higher at 20655 points. The USDJPY pair is remaining firm here after last night’s breakout, still just above the 106.30 level but not advancing any further:

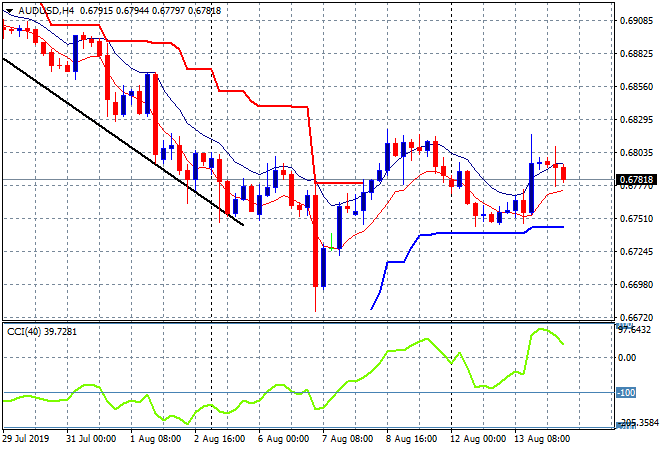

The ASX200 had a solid session, closing 0.4% higher at 6595 points, not quite able to breach the 6600 barrier. The Australian dollar has fallen back below the 68 handle after absorbing the latest Chinese industrial production figures, as the pair remains unable to breach last Friday’s highs:

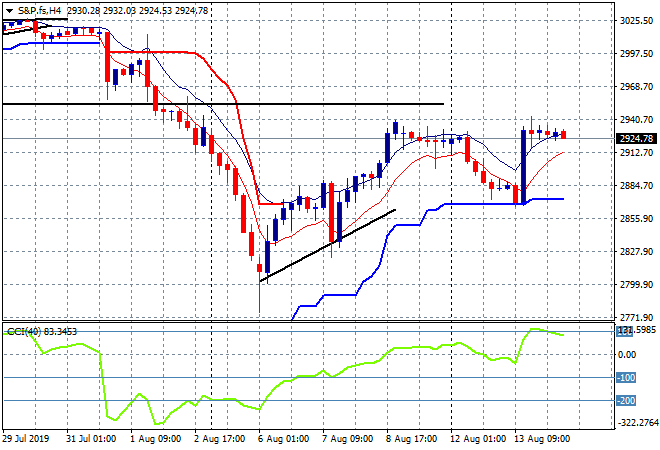

S&P and Eurostoxx futures are up only 0.1% or so with not much confidence translated from the firmer Asian session with the S&P500 four hourly chart still showing significant resistance at the 2930 point level to clear to turn this dead cat bounce into something sustainable:

The economic calendar continues tonight with more big releases to watch, namely the UK CPI print for July, plus the 2Q GDP print for the Eurozone, plus we get the latest DOE oil inventory report.