Markets are in a mixed mood as we head into the European session as Brexit, Itali-exit and Tianneman Square Part Deux demonstrations put a damper on risk appetite, with most stock markets off while the USD remains firm against most of the majors.

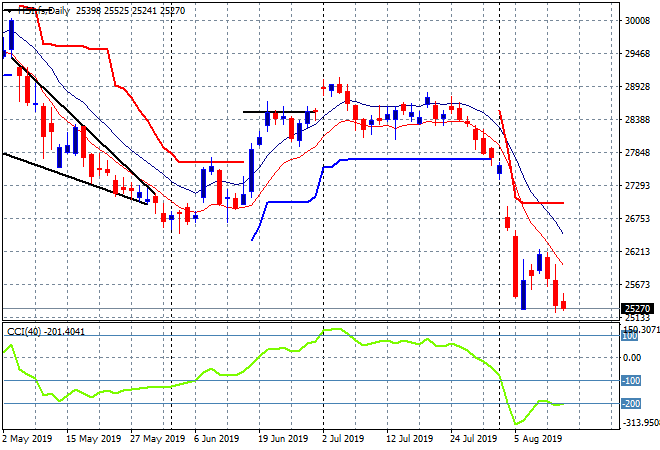

The Shanghai Composite has given up after its initial good start to the week yesterday, retracing half of those gains to fall 0.6% to 2796 points while the Hang Seng Index is no longer hanging on but selling in earnest as domestic risks outweigh all else, down 1.8% to 25365 points. This put below the January lows at 25000 and matches the previous daily lows from last week, with the daily chart spelling a lot of trouble ahead with very poor momentum:

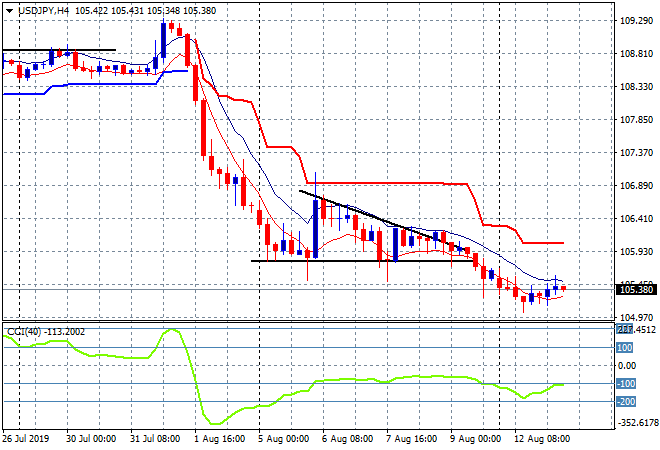

Japanese share markets have reopened from their holiday with the Nikkei 225 playing catchup to close 1.1% lower at 20455 points. The USDJPY pair has finally firmed a little, remaining just above the 105.30 level after teasing a break below the 105 handle proper. The bearish descending triangle pattern on the four hourly chart that broke on Friday night is still in play with the next target at the longer term level nearer 104:

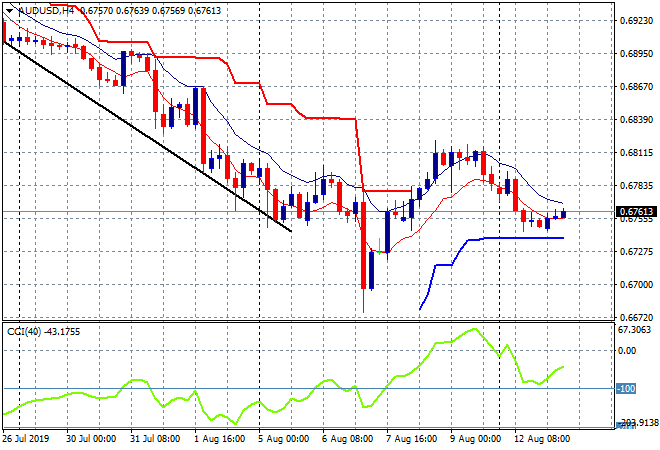

The ASX200 is the best in the region, relatively speaking, falling only 0.3% to close at 6568 points, still unable to breach the 6600 barrier. The Australian dollar is steady against USD but remains elevated versus NZD while firming against Yen, with the AUDUSD pair looking to trundle along here below the 68 handle:

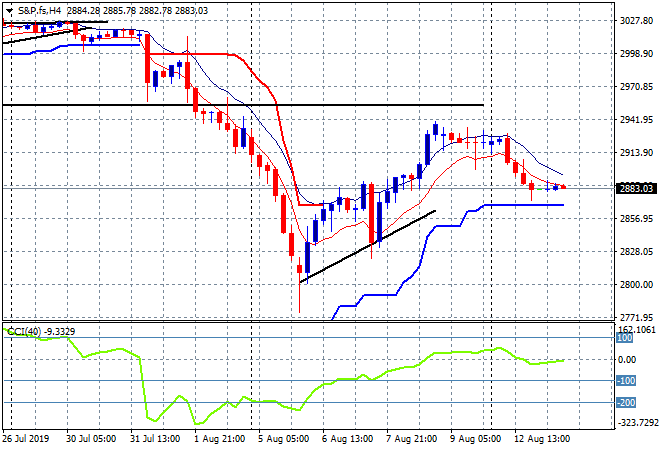

S&P futures are up 0.2% or so while Eurostoxx futures are down 0.1% with the S&P500 four hourly chart still showing a potential slowdown just above trailing support at the 2860 point level that must hold tonight otherwise more dead cats:

The economic calendar continues with two big ones tonight: the closely watched German ZEW survey and US CPI for July