Via Damien Boey at Credit Suisse:

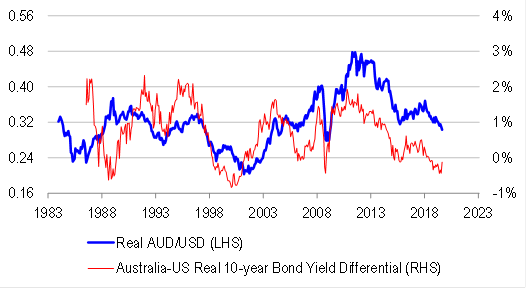

As bonds have rallied furiously in recent weeks, an interesting development to note is that Australian real yields have remained flat, while US real yields have fallen sharply to negative from positive. As a result, the Australian-US real 10-year bond yield differential has closed to -0.1% from -0.4% in late July. The real yield differential has improved in Australia’s favour, supporting the AUD/USD.