There is no science to it. But there’s common sense. Jason Murphy at News kicks us off:

Australia’s economy is in a spot of bother. Let us count the ways:

• A trade war threatening the economies of our two biggest trading partners.

• Monstrous levels of household debt combined with pitiful wages growth.

• Unemployment and underemployment stuck too high to generate wages growth.

• A Reserve Bank slashing interest rates to record lows and talking about bringing in quantitative easing.

What we need from the government is a bit of oomph. A spending push to keep the cycle of earning and spending going. Instead we’re going to get … a surplus? How can that possibly be a good idea?

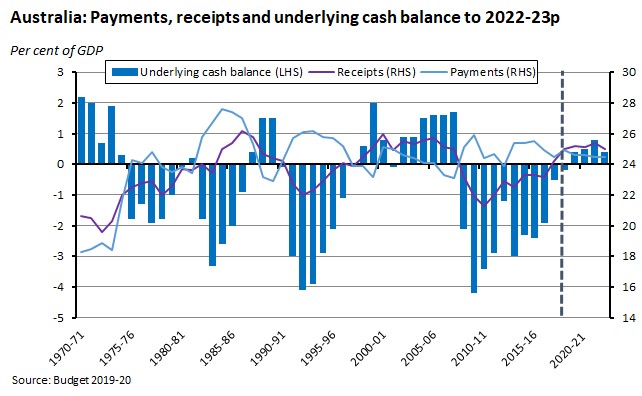

Australia has an absurd surplus obsession based on a misreading of what former Treasurer Peter Costello did in the 2000s. Costello was Treasurer during a time when money was coming in hand over fist. So much money that Treasury was continually surprised how much there was.

…Peter Costello and his Prime Minister John Howard were not stupid. They did not run a surplus in the bad times. That would be insane. They ran a surplus because the times were bountiful. They presided over a giant and unforeseen run of economic good fortune.

In the most recent Budget, though, Australia’s Treasurer announced a surplus. The 2019-20 surplus is projected to be $7.1 billion, and with the recent high price of iron ore, it could be even more.

Let’s just say it. This is the wrong time for a surplus. The wrong time for the government to be taking money out of the economy and using it to pay down debt. The economy needs all the money going around it can get. This is the worst surplus ever.

That is about right but a few points leaven things:

- There are benefits of running said surplus when things are weak. Such as sinking the currency. The question is how weak do want to be and how much juice do you want to feed into asset prices?

- Howard and Costello did run surpluses in bad times. See the Asian crisis and Millennium recessions:

That said, they did so as domestic demand boomed with a gale of household debt accumulation underway.

Moving on, Kevin Rudd also puts the boot into Recessionberg at the AFR:

The risk of recession in Australia next year is therefore real. The question for government is, are they prepared to prevent it?

Australia should reflect carefully on the lessons from a decade ago when we last faced such a challenge: which of those conditions still exist, which are different, and what new approaches may be necessary. In 2008-2009, we faced the reality of a global financial crisis, collapsing financial institutions, global recession and the possibility of a second global depression.

…The government will claim it’s introduced significant tax cuts, the Reserve Bank of Australia has reduced rates and the Australian Prudential Regulation Authority has relaxed the criteria for bank lending. These, however, are already factored in. The government will require much greater policy dexterity to anticipate and respond to the recession risk.

It’s all about Kevin as usual but he does have one point. Recessionberg will be blamed if he overcooks the surplus as growth crashes, and that is where we’re at.

So, how do we measure Josh Recesionberg’s ineptitude? I’ve drawn up a handy chart based upon next week’s GDP numbers:

The chart can be read this way:

- If we see a Q2 growth number of 0.2 then we’ll see annual GDP meet the slowest level since 2000, almost twenty years, an impressive achievement I’ve labeled “oaf”.

- If we see a Q2 growth number of 0 then we’ll see the lowest annual GDP since 1992, almost forty years, a startling achievement I’ve labeled “idiot”.

- If we see a Q2 growth number of -0.2 then we’ll see the lowest annual GDP since 1992, almost forty years, as well growth deep into stall speed at 0.7%, a spectacular achievement I’ve labeled “imbecile”.

- Finally, we see if we see a Q2 growth number of -0.4 (where it is currently tracking) then we’ll see the lowest annual GDP since 1992, almost forty years, as well annual growth at the verge of recession at 0.5%, a singular achievement I’ve labeled “simpleton”.

It must be remembered that Recessionberg is managing an economy enjoying an outrageous external boom, literally flooding the economy with a river of cash, as the global business cycle tilts very precariously towards recession itself. This sets us for a an external shock of huge proportions landing on an economy already at stall speed and losing altitude.

Why would Recessionberg act in this manner? John Hewson rounds us out:

The echoes of Trump’s triumphant rhetoric in our government’s insistence that our economy is strong and our economic fundamentals are good are particularly eerie. Both are essentially running a marketing, rather than a well-defined policy, strategy. As economic circumstances begin to run against them, exposing the hubris in their rhetoric, they see their challenge as to how best to embrace and explain reality?

…Our growth has collapsed over the past three quarters. Wages are flat, job insecurity is mounting, house prices are falling, mortgage stress is significant. We have one of the highest levels of household debt in the world and a majority of households are living payday to payday.

Our economy is one of the most exposed in the world to another global financial shock, a sustained trade war, a collapse in global trade and commodity prices, and/or a global drift into recession. Yet, the government has legislated tax cuts through to almost the mid-2020s, while inconsistently committing to deliver budget surpluses and the repayment of debts for a decade or so, and the RBA has admitted to little capacity to respond.

Not quite. Like Howard and Costello, the Recesionberg has a clear strategy. The problem is it hopelessly wrong for the times. The Morrison Government’s clear objective is to crash interest rates as fast as possible to drive a new house price boom and damn the lifeboats!

That’s what you get when you elect a real estate agent prime minister and a card board cut out as treasurer.