Analysis released today by Digital Finance Analytics reveals that in the coming 12 months around 124,000 interest only loans will need to be switched to principal and interest loans. This is drawing data from our rolling household surveys. This translates to an estimated value of $47 billion, and represents a significant proportion of all IO loans coming up for review. Of these 97.5% are for investment properties.

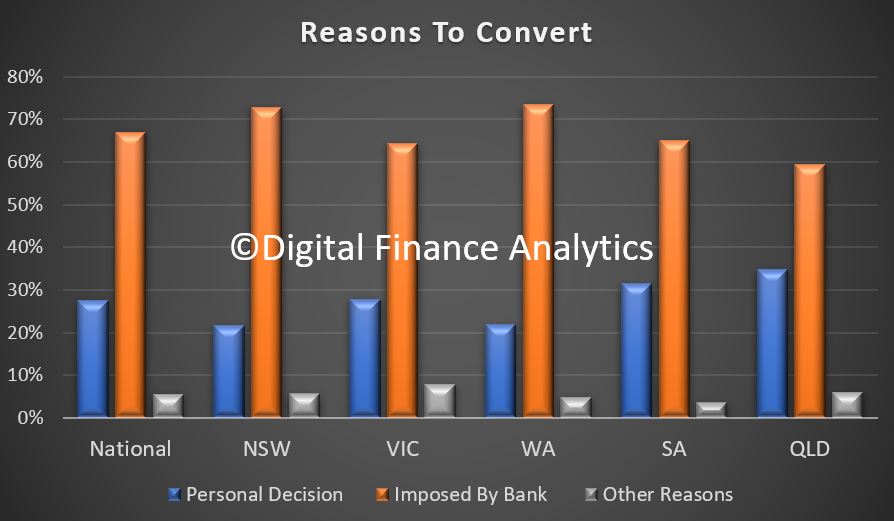

The reason why households are converting varies, with around 27% deciding to switch, while 67% were persuaded by their lender. There are state variations. NSW and WA had the highest proportion of “forced” moves.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.