Liberal MP, Jason Falinski, believes the overwhelming majority of MPs in Canberra do not want to lift Australia’s superannuation guarantee (compulsory superannuation) to 12%, as currently legislated. From The AFR:

[Falinski] told the Financial Services Council Summit in Sydney on Tuesday that behind closed doors support for a freeze was widespread, including among Labor MPs.

“It’s fair to say that in Canberra if you get most members of parliament, regardless of which side they sit [and] without a microphone around them, you wouldn’t find a lot of support for an increase in the super guarantee much over 10 per cent,” he said.

“The reason for that is report after report after report has demonstrated that we don’t have a system that is necessarily as efficient as it needs to be”…

“A prevailing view in Canberra, that putting more money into a system that refuses to respond to consumer needs is not something people would like.

Lifting the superannuation guarantee without first fixing the underlying design problems would be a recipe for disaster. All it would do is heighten inequities already entranced across the system, rob the federal budget of much needed tax revenue, and reduce workers’ take home pay (since compulsory superannuation is salary sacrificed by employees).

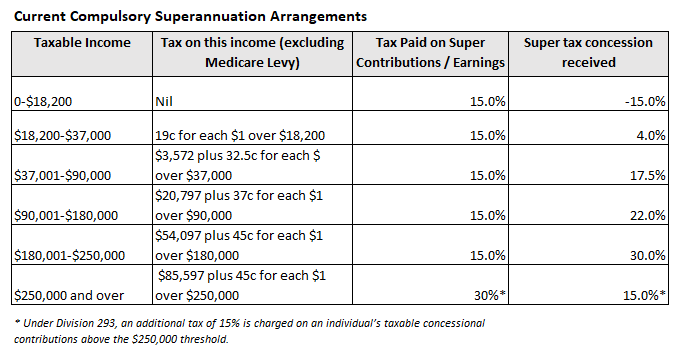

The key problem with Australia’s superannuation system is that the lion’s share of tax concessions on contributions / earnings flow to higher income earners – those whom are the least likely to be reliant on the Aged Pension – as illustrated in the next table:

This set-up ensures that superannuation is used as a tax shelter by higher-income earners, while not adequately reducing lower-income earners’ reliance on the Aged Pension. In turn, the cost to the federal budget from the superannuation guarantee outweighs any future savings from the Aged Pension, as modelled by the Henry Tax Review and the Grattan Institute.

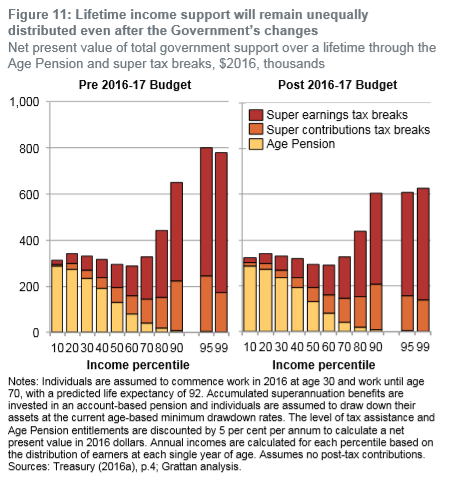

Division 293 remedies the concession imbalance for very high income earners above $250,000. But even then, the overwhelming majority of superannuation concessions still flow to higher income earners, whereas lower income earners continue to be disadvantaged by the system, as shown illustrated below:

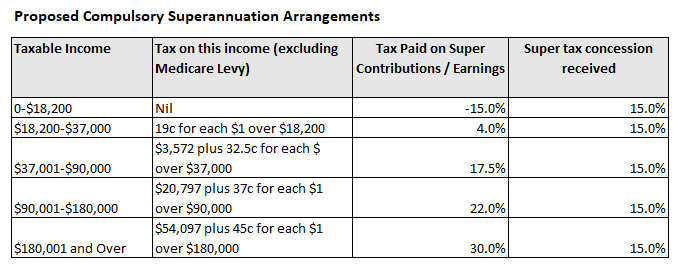

Therefore, making superannuation concessions more equitable is paramount before policy makers even consider raising the superannuation guarantee to 12%. This could be done by replacing the 15% flat tax on contributions / earnings with a flat 15% concession, as illustrated in the next table:

Under this proposal, everyone that contributes to superannuation would receive the same concession (15%). Accordingly, the superannuation system would be made progressive and lower income earners, in particular, would get a better deal.

It would also save the federal budget money, since the tax sheltering effect among high income earners would be reduced. Lower income earners would also retire with larger superannuation balances, thereby reducing pressure on the Aged Pension.

Sure, there are other reforms that could be done around excessive fees, contributions caps and the like, but they are secondary to fixing the inequitable concession system.

The key point is that policy makers must not raise the superannuation guarantee (compulsory super) from its current 9.5% to 12% without first reforming the way that contributions / earnings are taxed. They must fix this problem first, not add to the inequities.