Earlier this month, Mercer senior actuary, David Knox, made the false claim that freezing the superannuation guarantee at 9.5% “will hurt average workers” and directly attacked analysis from the Grattan Institute supporting a freeze.

Today, the Grattan Institute has hit back, releasing a report debunking Mercer’s arguments. Below are the key points:

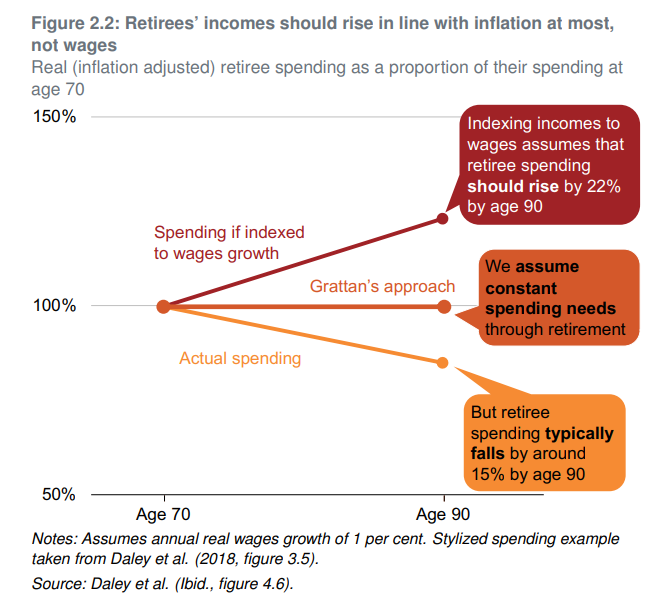

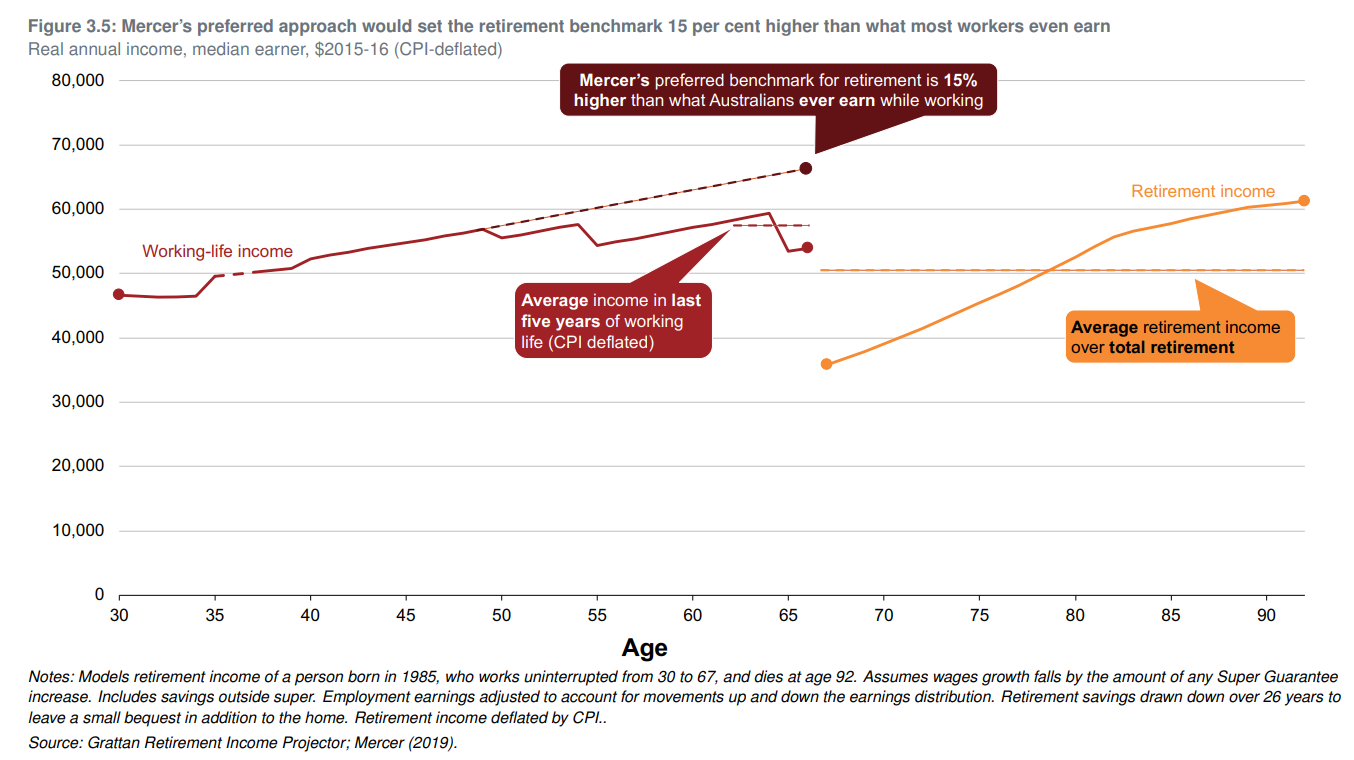

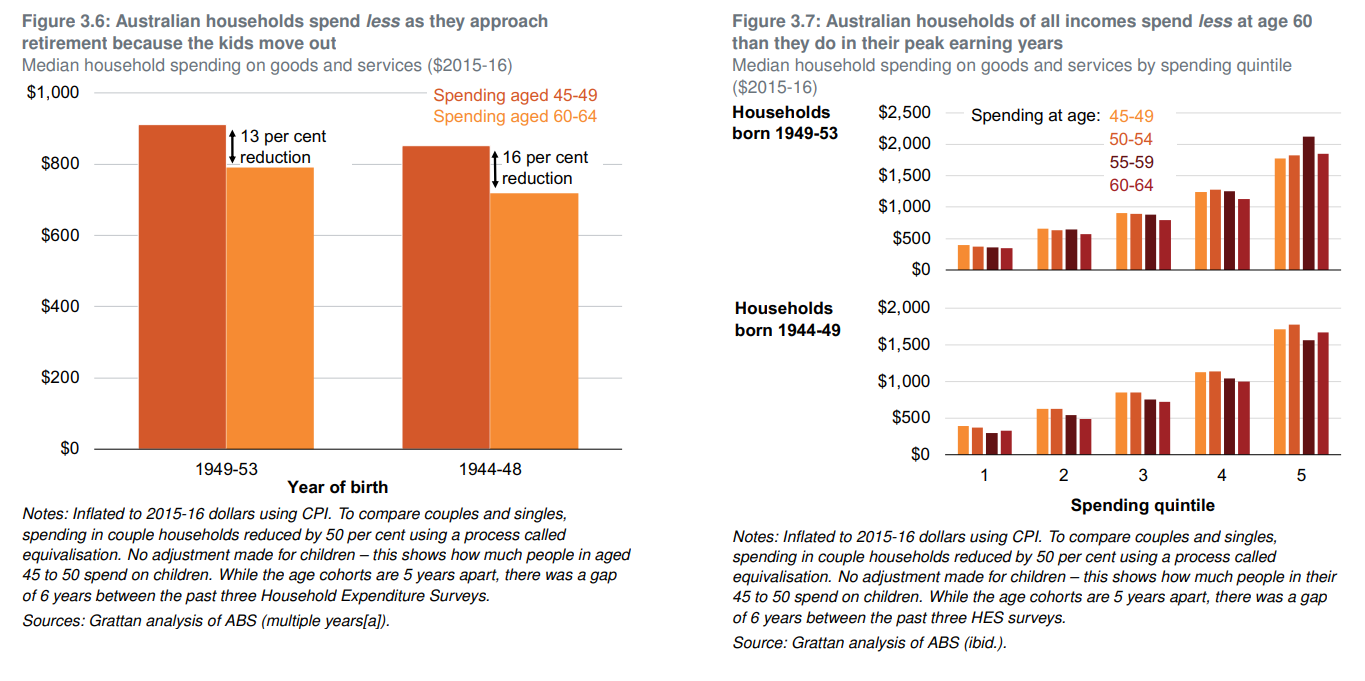

Mercer argues that retirement incomes should be assessed against the peak in earnings from ages 40 to 55, and then index that figure by wages, through to age 67. But Mercer’s benchmark for an adequate retirement income is 15 per cent higher than Australians ever earn while working. Mercer’s approach ignores the fact that most Australians aged 40-55 are still incurring the costs of raising dependent children, whereas in retirement they are not. Our analysis shows that spending by Australian households falls by around 15 per cent as they move from ages 45-49 to 60-64.

Some of Mercer’s other mistaken claims result from an unfortunate misreading of our approach. Mercer mistakenly concludes that we model a decline in working-age incomes in the lead up to retirement, when in fact incomes in our modelling peak just before retirement.

Advertisement

And Mercer’s preoccupation with ensuring all retirees, and especially wealthier retirees, are as well off in retirement as beforehand is a recipe for higher inheritances. Its approach would force low- and middle-income Australians to over-save for their retirement. Policymakers can only justify lowering someone’s living standards during their working life if they’re protecting them from even worse outcomes in retirement

And below is the report summary combined with key charts:

Grattan Institute research has shown that the conventional wisdom that most Australians don’t save enough for retirement is wrong. The vast majority of retirees today and in future are likely to be financially comfortable.

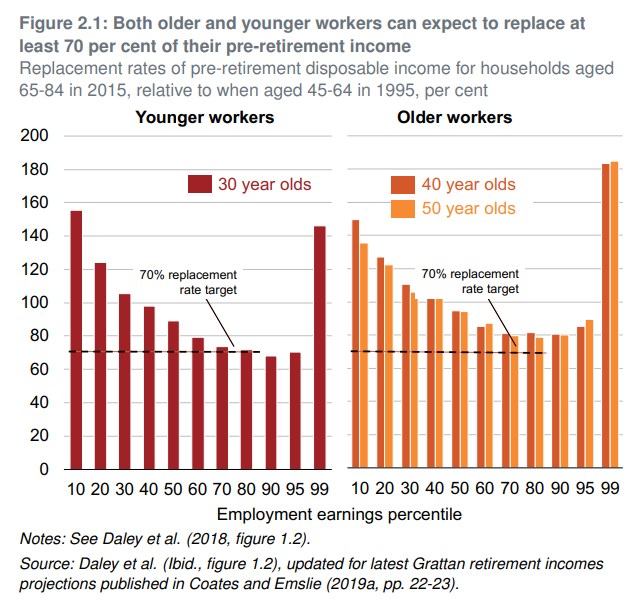

Our modelling shows that on reasonable assumptions, most workers today will also be comfortable when they retire. The median worker aged 30 can expect a retirement income of at least 89 per cent of their pre-retirement income – well above the 70 per cent benchmark used by the OECD and others, and more than enough to maintain pre-retirement living standards. And many low-income Australians will get a pay rise when they retire, through a combination of the Age Pension and their compulsory superannuation savings. Policymakers can only justify lowering someone’s living standards during their working life if they’re protecting them from even worse outcomes in retirement.

Grattan’s findings accord with past modelling by the Treasury, including that done for the Henry Tax Review. And they are consistent with recent retirement modelling by actuarial firm Rice Warner. In contrast, research by others in the superannuation industry that finds otherwise has overestimated retirees’ spending needs, or ignored non-super savings.

In a recent report, superannuation firm Mercer claimed Grattan’s retirement income research was ‘very misleading’ and was based on assumptions that were ‘not realistic’ for the average Australian. This Grattan policy paper shows that the Mercer critique of our work misses the mark.

Some of Mercer’s mistaken claims result from an unfortunate misreading of our approach. Others reflect an assumption that Australian workers should save enough to have a better living standard in retirement than they ever have while working. Mercer’s work falls into the same trap as so much other Australian research on retirement incomes: it makes assumptions about what retirees need without looking closely at what they spend, or what they earn while working. And Mercer’s preoccupation with ensuring all retirees, and especially wealthier retirees, are as well off in retirement as beforehand is a recipe for higher inheritances. Its approach would force low- and middle-income Australians to over-save for their retirement.

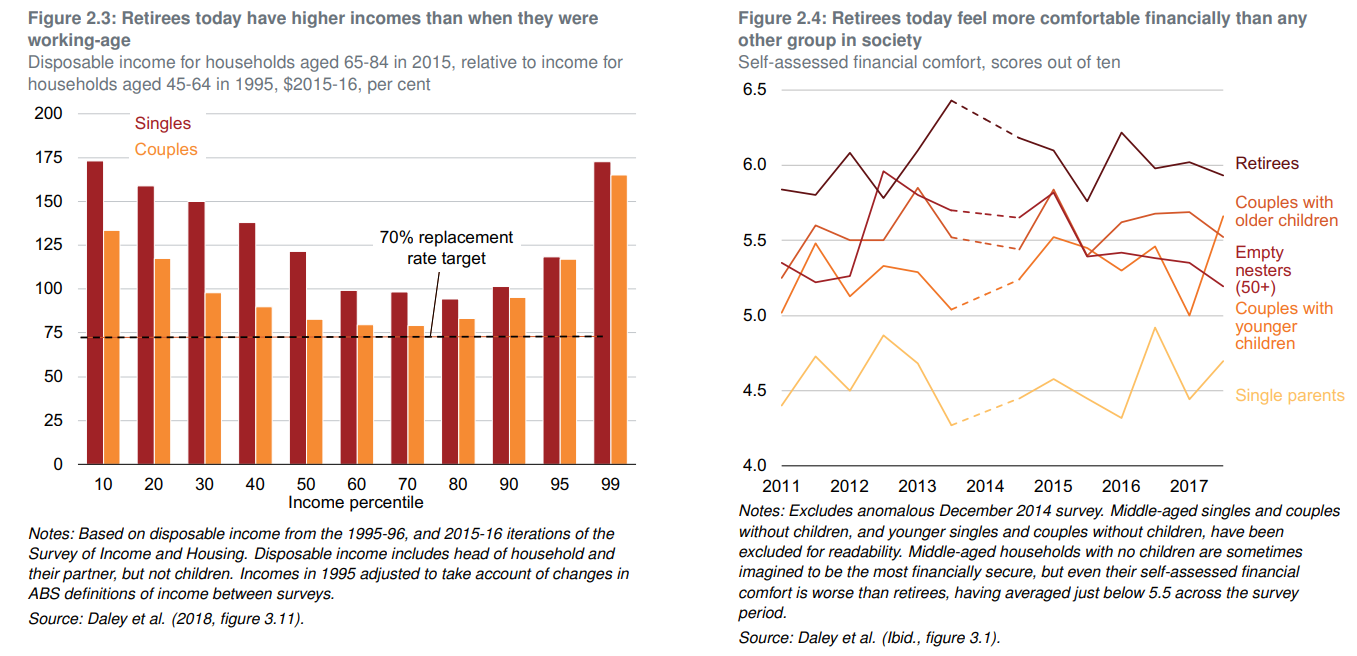

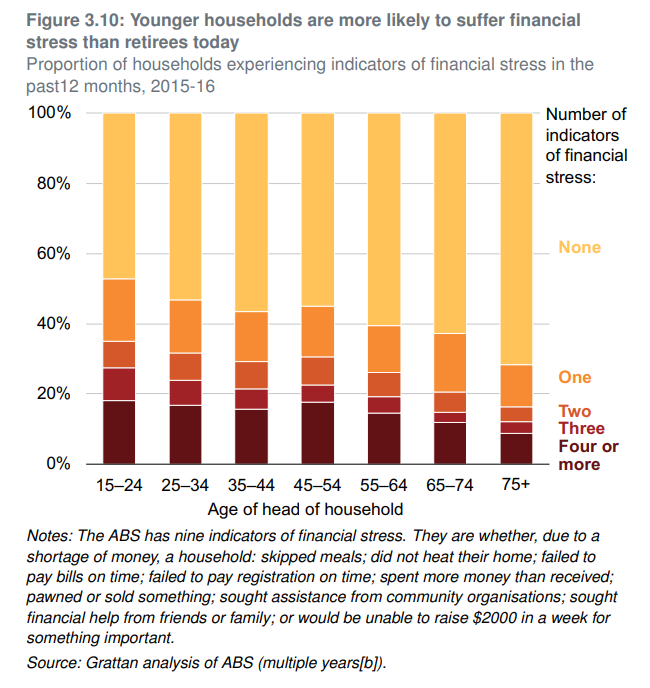

In contrast, our modelling is consistent with the lived experience of retirees today. Our Money in retirement report showed that most retirees today have a similar or higher living standard as they had while working. Most retirees today feel more comfortable financially than younger Australians who are still working. And retirees are less likely than working-age Australians to suffer financial stress such as not being able to pay a bill on time.

Retirement incomes policy needs to balance the trade-off between higher living standards when retired against lower living standards when working. And retirement modeling should reflect the reality of Australians’ spending needs, in retirement and beforehand. Unfortunately, Mercer’s critique of Grattan’s retirement research does neither.

Advertisement

Grattan’s research shows, once again, that higher compulsory superannuation contributions are not needed. Raising the superannuation Guarantee to 12% would cost workers and governments more today, would do little to boost the retirement incomes of low-and middle-income earners, and would lead to lower pensions for both current and future retirees.

Instead, Grattan recommends:

Relaxing the Age Pension asset test taper for people earning up to 1.5 times average earnings ($120,000 a year), which would cost the budget less than a third as much ($750 million a year compared to $2.5 billion a year); and

Boosting Commonwealth Rent Assistance by 40% (roughly $1,400 a year for singles) would lift many retirees who rent out of poverty and cost only $1.2 billion a year.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.