Via the excellent Damien Boey at Credit Suisse:

Overnight, markets were spooked by deteriorating economic data and broad-based inversion of yield curves among the developed markets. The risk-off phase started with weak Chinese data, and was reinforced by weak European data. In 2Q:

- German real GDP shrunk by 0.1%, the second quarterly contraction within the space of a year. Year-ended growth slowed to 0.4% from 0.9%.

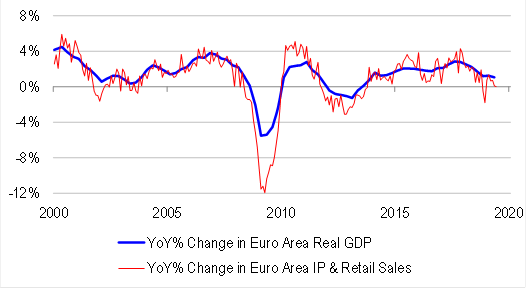

- European real GDP rose by a modest 0.2%, taking year-ended growth slightly lower to 1.1% from 1.2%.