CoreLogic has released new data showing that despite heavy price falls across both Sydney and Melbourne, there was still very few sales priced below $400,000:

Throughout the 2018-19 financial year, 26.0% of all houses sold nationally were under $400,000 and 32.5% of all unit sales were under $400,000. Despite the weakening housing market the share of house sales under $400,000 was virtually unchanged from a year ago, down from 26.3% the previous year while the share of unit sales under $400,000 increased from 31.0% over the 2017-18 financial year.

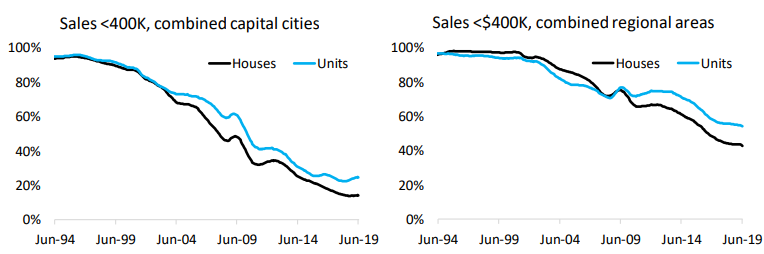

Across the combined capital cities, 13.9% of house sales over the 2018-19 financial year were under $400,000 and 24.6% of unit sales were under this price point. The share of house sales under $400,000 was virtually unchanged from the previous year, recorded at 13.8% while the share of unit sales was noticeably lower at 22.3%. Despite house and unit values falling -8.7% and -5.9% respectively over the year, it is interesting to note that the share of unit sales under $400,000 has increased much more for units than houses…

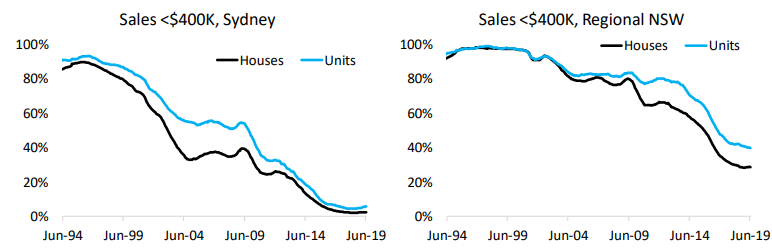

Over the 2018-19 financial year, 2.3% of all house sales in Sydney were below $400,000 compared to 2.0% over the previous financial year indicating a slight increase. It was a similar story for units with 5.7% of all sales below $400,000 over the past year compared to 4.4% a year earlier. Despite the recent declines in dwelling values in Sydney, there has not been any substantial increase in the share of sales below $400,000…

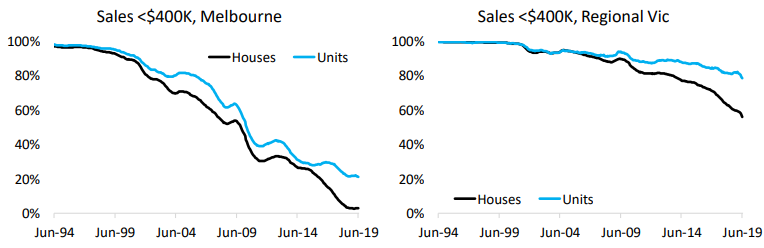

Although Melbourne dwelling value shave fallen throughout the 2018-19 financial year there has been a further decline in the share of houses and units selling below $400,000. The share of houses selling for less than $400,000 fell from 3.6% over the 2017-18 financial year to 2.9% over the 2018-19 financial year. It’s a similar story for units that recorded a fall in the share of sales under $400,000 from 21.9% to 21.2% over the past two financial years…

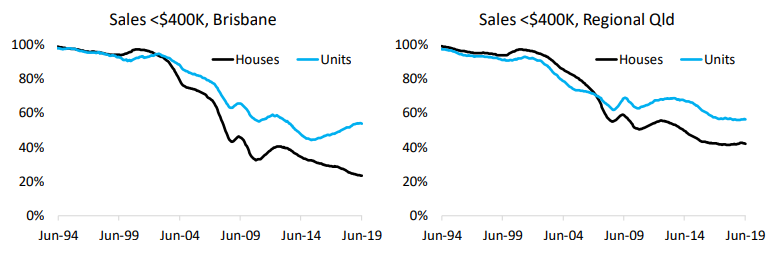

Although Brisbane dwelling values have recorded a moderate fall over the past year, the share of house sales under $400,000 has reduced while the share of units selling under that price point has increased. Over the most recent financial year, 23.2% of houses and 53.5% of units sold for less than $400,000. By comparison, over the 2017-18 financial year 25.0% of houses and 51.5% of units sold for less than

$400,000. The share of units selling under $400,000 was last as high as it is currently in 2012-13 financial year…

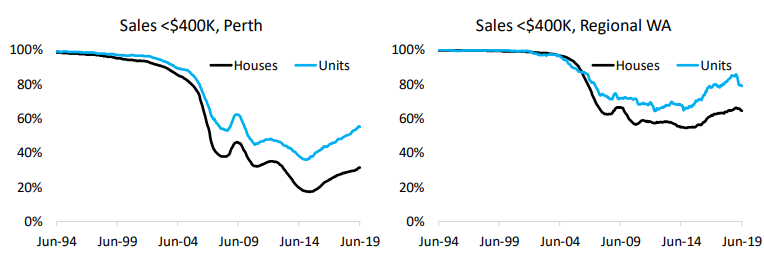

With ongoing value declines over recent years across Perth, the share of sales under $400,000 for houses and units has increased over the most recent financial year, rising to 31.2% of houses sold from 28.7% the previous year while for units the share has risen to 55.0% from 50.2%…

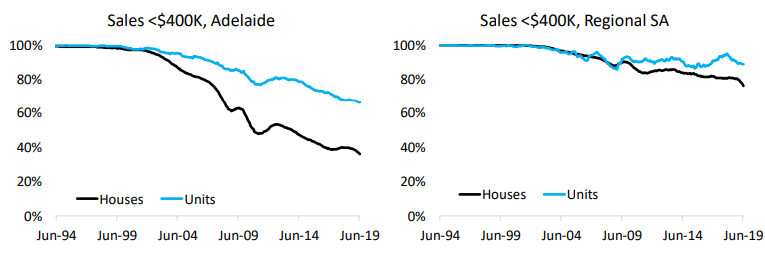

Over the 2018-19, financial year houses and units in Adelaide have recorded a reduced share of sales occurring under $400,000. For houses, the share of sales under $400,000 fell to 35.8% from 39.6% the previous financial year while for units the share fell from 67.9% to 66.1%. Although overall values have drifted slightly lower over the year, it hasn’t led to an increased share in sales under $400,000…

The next financial year could look very different to what we have seen over the 2018-19 financial year. We’re only in mid-August and we’ve already seen interest rates reduced twice, serviceability floors on mortgages reduced and some recent rises in dwelling values in the largest capital cities. While a significant rise in dwelling values isn’t expected, there is an expectation of a moderate increase in dwelling values, as a result the 2019-20 financial year is expected to see fewer sales under $400,000 than those recorded in 2018-19.

Interestingly, separate data from SQM Research shows that despite the heavy price falls, gross rental yields across both Sydney and Melbourne remain at ridiculously low levels:

Advertisement

This suggests that Sydney and Melbourne housing remains way overvalued and further heavy price falls are necessary to restore valuations back to sensible levels.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.