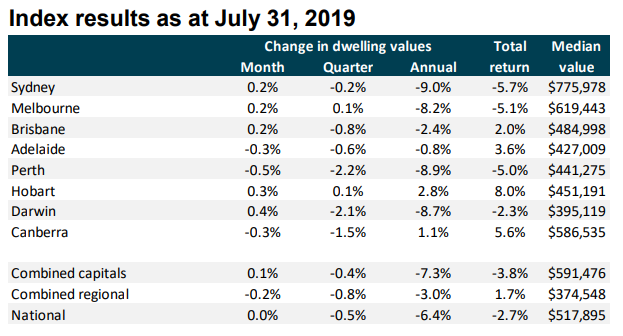

Following on from yesterday’s post on CoreLogic’s daily dwelling values index results for July, CoreLogic has released its full results, which also cover the smaller capitals and regional areas (see next table).

As you can see, Sydney (0.2%), Melbourne (0.2%), Brisbane (0.2%), Hobart (0.3%), and Darwin (0.4%), all registered rising dwelling values in July, whereas Adelaide (-0.3%), Perth (-0.5%) and Canberra (-0.3%) recorded falls.

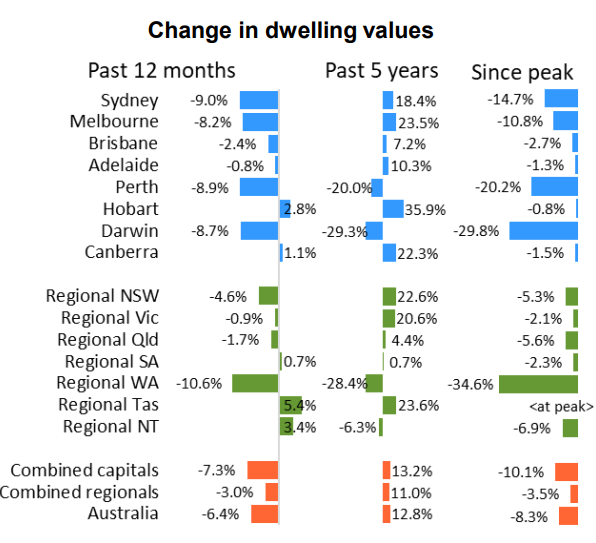

The below chart shows the change in dwelling values over various time periods:

Advertisement