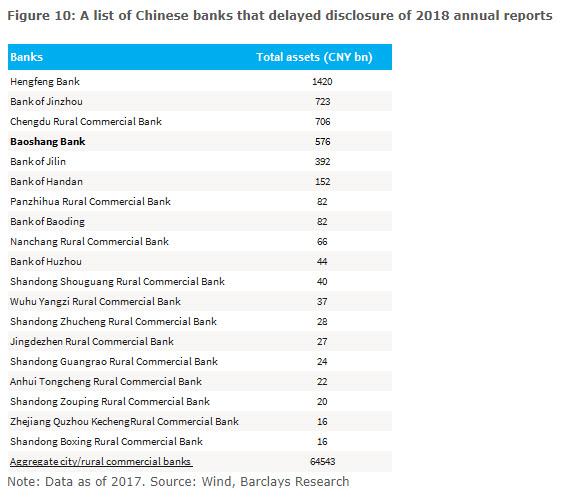

Last month, when reporting on the imminent failure of yet another Chinese bank in the inglorious aftermath of Baoshang Bank’s late May state takeover, we dusted off a list of deeply troubled Chinese financial institutions that had delayed their 2018 annual reports…

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.