Advertisement

Via the excellent Damien Boey at Credit Suisse:

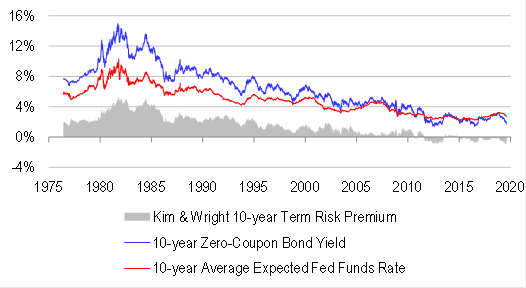

Over the past few weeks, the bond rally has taken us to uncharted territory. It is not so much that global bond yields are pushing record lows. It is not so much that a significant portion of investable government debt around the world is now offering negative yields. Rather, the key development is that so-called term risk premia across the world are at their most negative in recorded history. Recent market action has made a complete mockery of the very concept of term risk premia as either a speed limit indicator, or valuation tool for bonds.

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement