DXY was up Friday night and looks close to break out. EUR and CNY fell:

The Australian dollar lifted anyway on the risk rebound:

It was stronger than EMs too:

Advertisement

CFTC positioning became is now extended bearish at -61k contracts:

Gold eased:

Advertisement

Oil was stable:

Metals soft:

Miners too:

Advertisement

EM stocks firmed:

And junk:

Treasuries fell:

Advertisement

And bunds:

Plus Aussie:

Stocks roared:

Advertisement

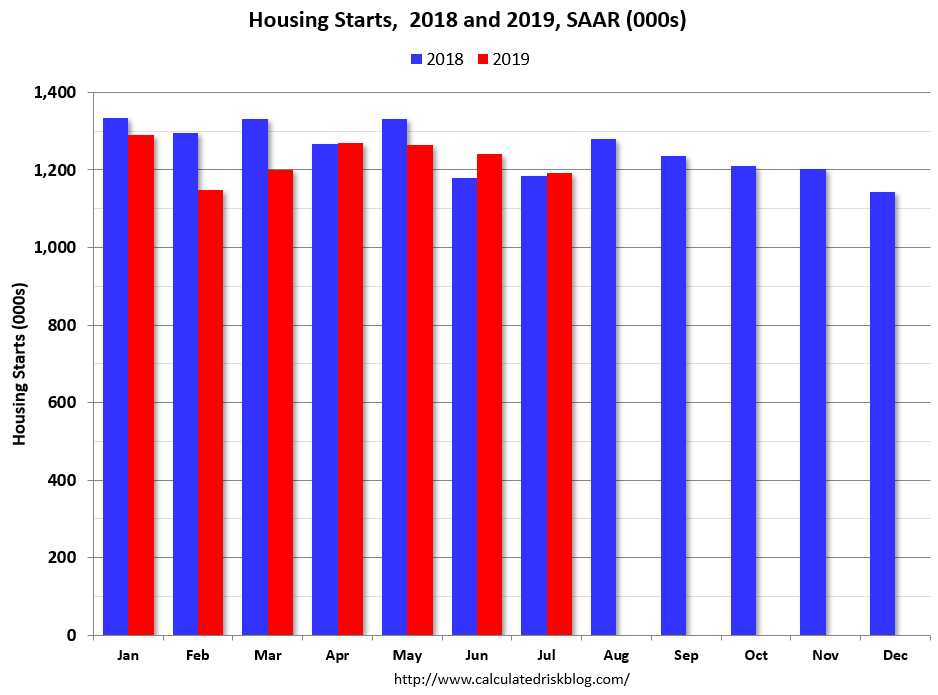

US data was again solid. Housing starts were up year on year:

Housing Starts:

Privately‐owned housing starts in July were at a seasonally adjusted annual rate of 1,191,000. This is 4.0 percent below the revised June estimate of 1,241,000, but is 0.6 percent above the July 2018 rate of 1,184,000. Single‐family housing starts in July were at a rate of 876,000; this is 1.3 percent above the revised June figure of 865,000. The July rate for units in buildings with five units or more was 303,000.

Building Permits:

Privately‐owned housing units authorized by building permits in July were at a seasonally adjusted annual rate of 1,336,000. This is 8.4 percent above the revised June rate of 1,232,000 and is 1.5 percent above the July 2018 rate of 1,316,000. Single‐family authorizations in July were at a rate of 838,000; this is 1.8 percent above the revised June figure of 823,000. Authorizations of units in buildings with five units or more were at a rate of 453,000 in July.

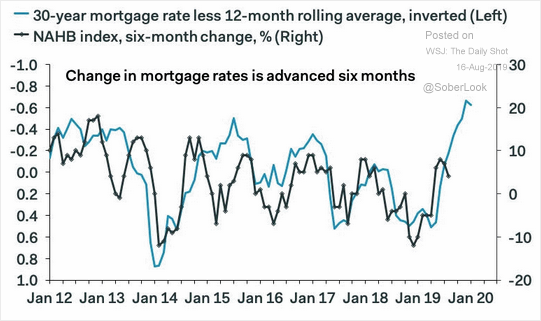

The big fall in the long bond is lifting housing (charts from WSJ Daily Shot):

Advertisement

While wages still strong with few layoffs:

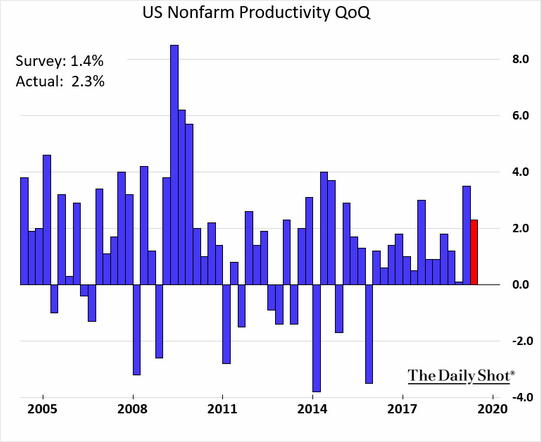

Which, along with good productivity:

Advertisement

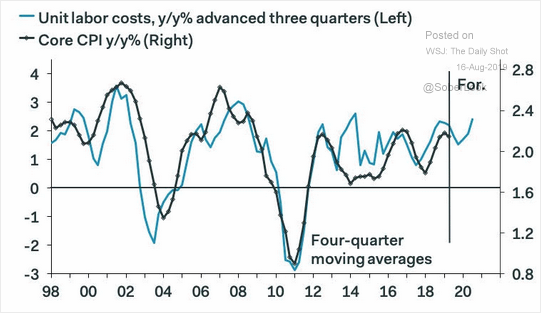

Is lifting wages:

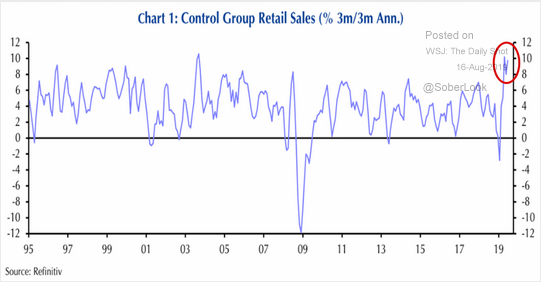

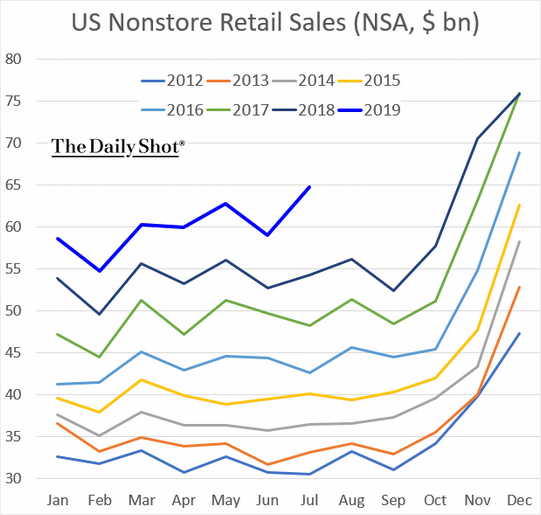

Helping retail:

Advertisement

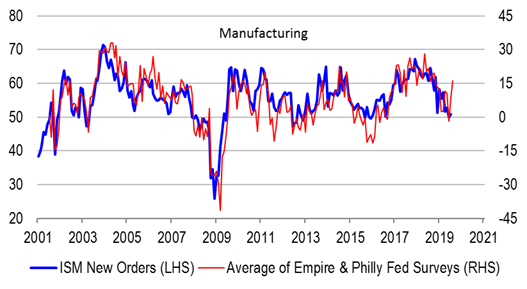

Which, in turn, is aiding industry:

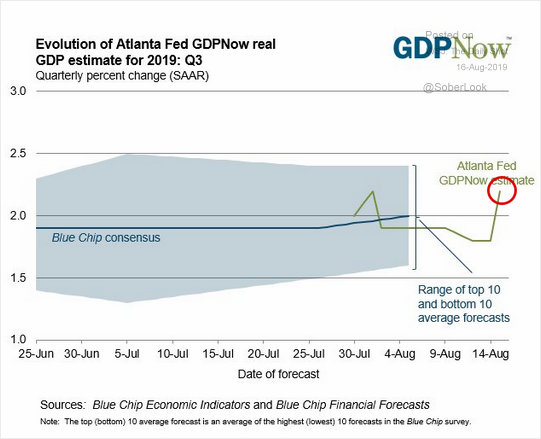

And GDP gains:

From Merrill Lynch:

Advertisement

The data boosted our 3Q GDP tracking estimate by 0.4pp to 2.1% qoq saar. 2Q was unchanged at 1.8%.

And Goldman Sachs:

We left our Q3 GDP tracking estimate unchanged on a rounded basis at +2.1% (qoq ar).

The US is holding up while China and Europe sink. This can only push DXY to break out as it delays Fed easing.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.