Mush of the data for the evening was in US consumer and housing markets. Consumer confidence held up well against the volatility:

Advertisement

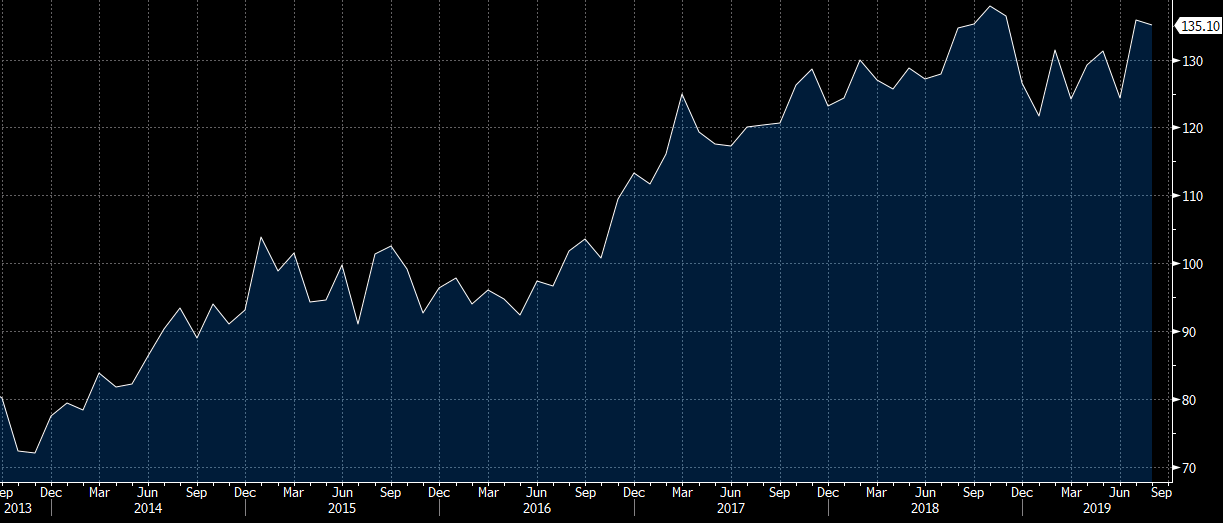

The Conference Board Consumer Confidence Index® declined marginally in August, following July’s rebound. The Index now stands at 135.1 (1985=100), down from 135.8 in July. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – increased from 170.9 to 177.2. The Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – declined from 112.4 last month to 107.0 this month.

“Consumer confidence was relatively unchanged in August, following July’s increase,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers’ assessment of current conditions improved further, and the Present Situation Index is now at its highest level in nearly 19 years (Nov. 2000, 179.7). Expectations cooled moderately, but overall remain strong. While other parts of the economy may show some weakening, consumers have remained confident and willing to spend. However, if the recent escalation in trade and tariff tensions persists, it could potentially dampen consumers’ optimism regarding the short-term economic outlook.”

Perhaps because property markets are too. House prices are rising around the pace of income, aided by the bond bid:

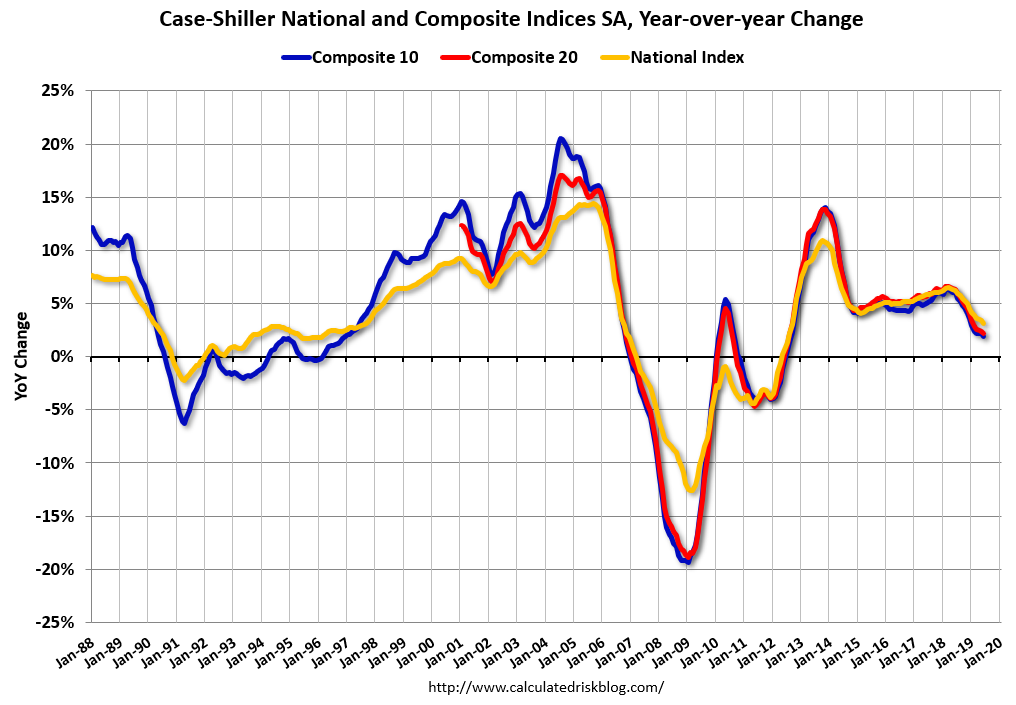

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.1% annual gain in June, down from 3.3% in the previous month. The 10-City Composite annual increase came in at 1.8%, down from 2.2% in the previous month. The 20-City Composite posted a 2.1% year-over-year gain, down from 2.4% in the previous month.

…Before seasonal adjustment, the National Index posted a month-over-month increase of 0.6% in June. The 10-City Composite posted a 0.2% increase and the 20-City Composite reported a 0.3% increase for the month. After seasonal adjustment, the National Index recorded a 0.2% month-over-month increase in June. The 10-City and the 20-City Composites did not report any gains. In June, 19 of 20 cities reported increases before seasonal adjustment, while 17 of 20 cities reported increases after seasonal adjustment.

“Home price gains continue to trend down, but may be leveling off to a sustainable level,” says Philip Murphy, Managing Director and Global Head of Index Governance at S&P Dow Jones Indices.

“The average YOY gain declined to 3.0% in June, down from 3.1% the prior month. However, fewer cities (12) experienced lower YOY price gains than in May (13).

Our estimate of the lag time between changes in interest rates and housing activity suggests the bulk of the boost is yet to come. … we update our outlook for the growth boost from housing via both the home building channel and the impact of refinancing, mortgage equity withdrawal, and housing wealth effects on consumer spending. Our model points to a healthy rebound to a 4% growth pace of residential investment in 2019H2 and an increase in the total contribution from housing to GDP growth from -0.05pp in H1 to +0.15pp in H2.

Advertisement

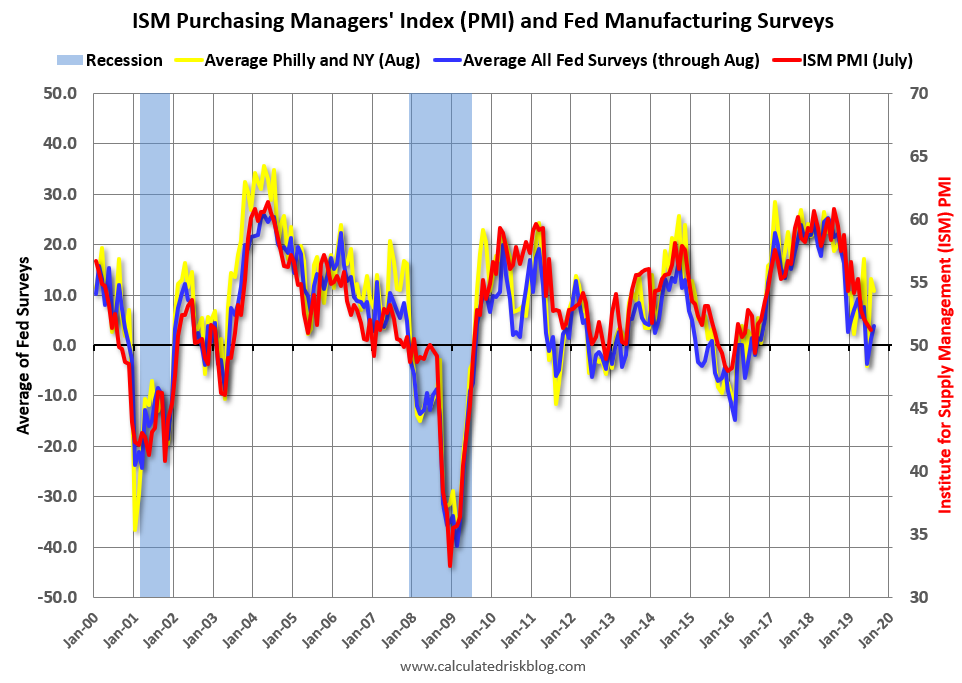

That makes sense so long as the global slowdown does not shock stocks. Finally, the regional Fed surveys are still OK, via Calculated Risk:

The New York and Philly Fed surveys are averaged together (yellow, through August), and five Fed surveys are averaged (blue, through August) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through July (right axis).

It’s all definitely slowed but isn’t collapsing by any stretch. And the bond bid has already injected huge stimulus.

Advertisement

It’s still wait and see for the Fed on anything more aggressive that insurance cuts. Adding to AUD downside risk. And given the most likely shock to really harm US growth will come from China’s direction, there’s a natural hedge in the AUD if the Fed is forced to slash and burn.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.