DXY fell sharply Friday night. EUR rebounded and CNY was belted:

The Australian dollar almost reached its 2019 flash crash low but rebounded:

EM forex is getting hosed:

CFTC positioning got shorter again:

Gold hit a new closing low, signalling possible further weakness for DXY:

Oil was firm:

Metals were belted:

Big miners were pulverised. GLEN was smashed with copper:

EM stocks were trashed:

Junk buckled:

Treasuries roared:

Bunds too:

And Aussie bonds:

Stocks were hit again:

The big release on the night was US jobs which were decent:

Total nonfarm payroll employment rose by 164,000 in July, and the unemployment rate was unchanged at 3.7 percent, the U.S. Bureau of Labor Statistics reported today. Notable job gains occurred in professional and technical services, health care, social assistance, and financial activities.

…The change in total nonfarm payroll employment for May was revised down by 10,000 from +72,000 to +62,000, and the change for June was revised down by 31,000 from +224,000 to +193,000. With these revisions, employment gains in May and June combined were 41,000 less than previously reported.

…In July, average hourly earnings for all employees on private nonfarm payrolls rose by 8 cents to $27.98, following an 8-cent gain in June. Over the past 12 months, average hourly earnings have increased by 3.2 percent.

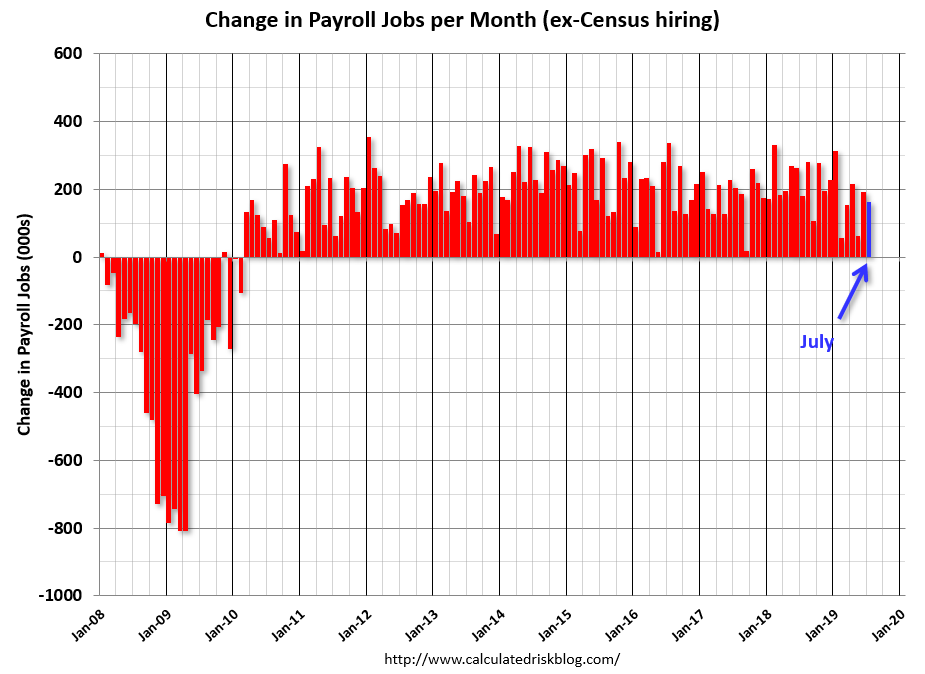

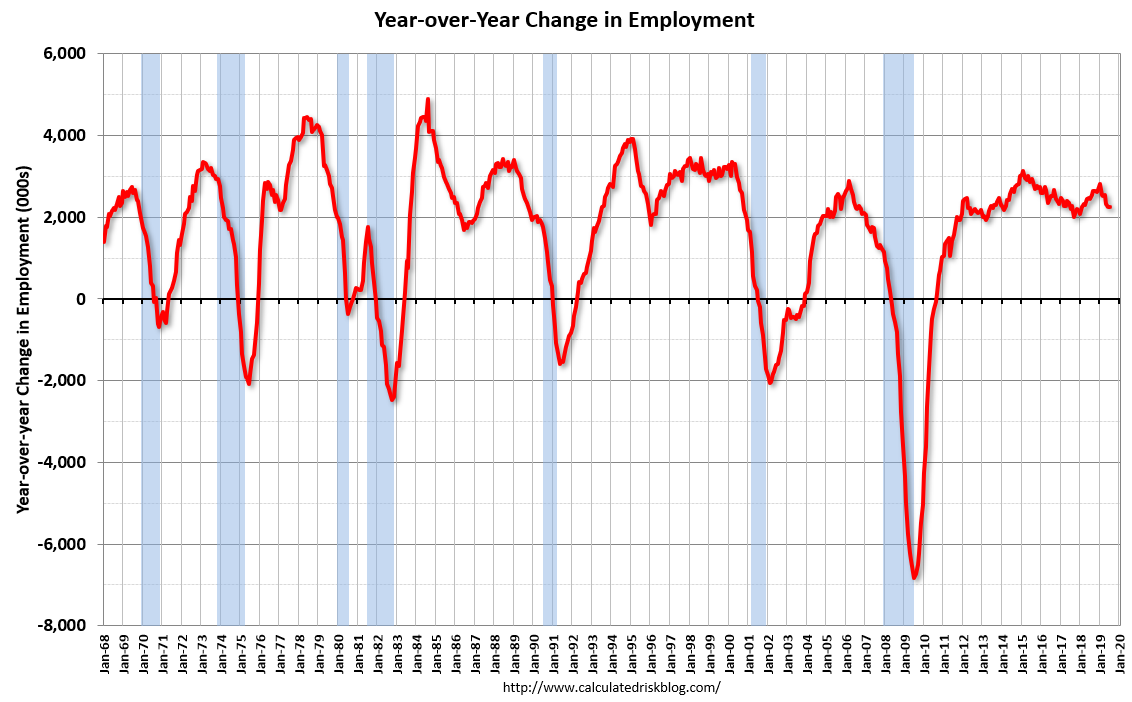

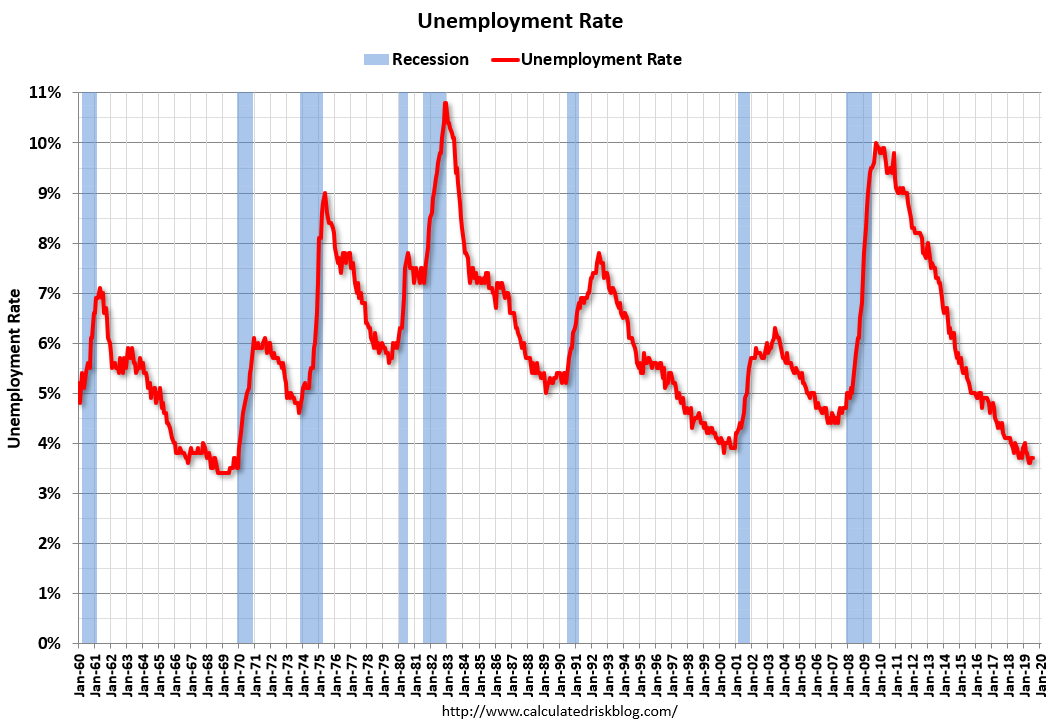

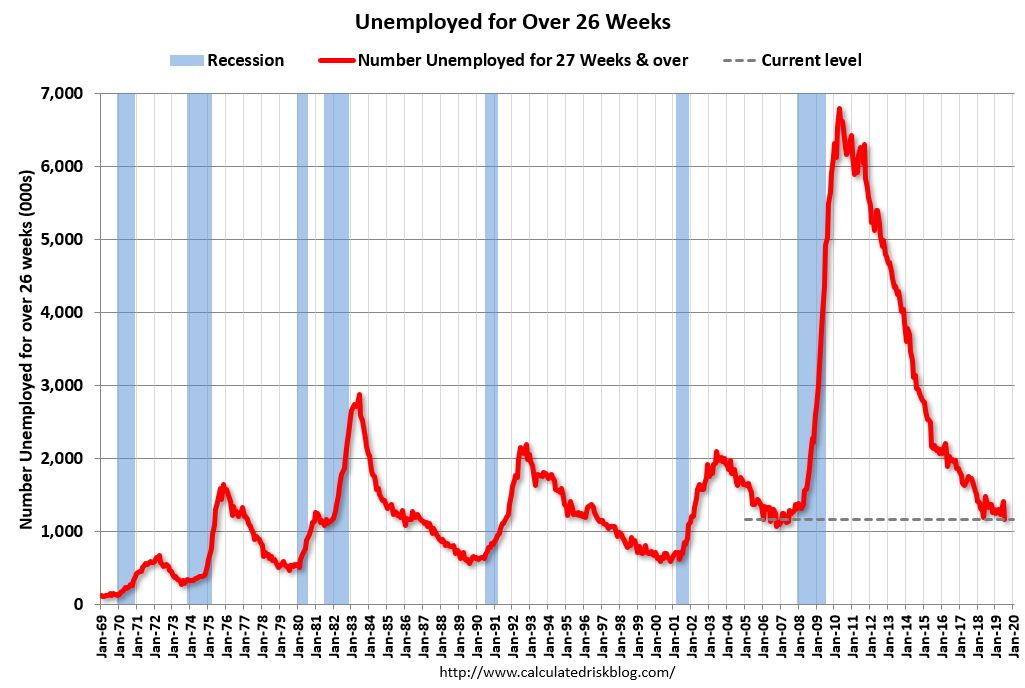

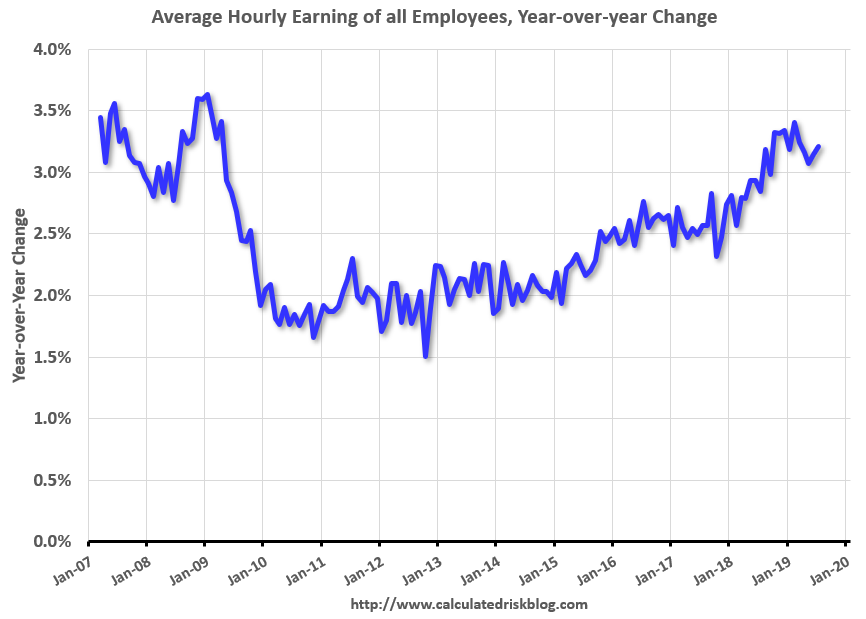

Headline was solid (charts from Calculated Risk):

Jobs growth is still good:

The unemployment rate very low:

With shadow slack still:

And solid wages growth:

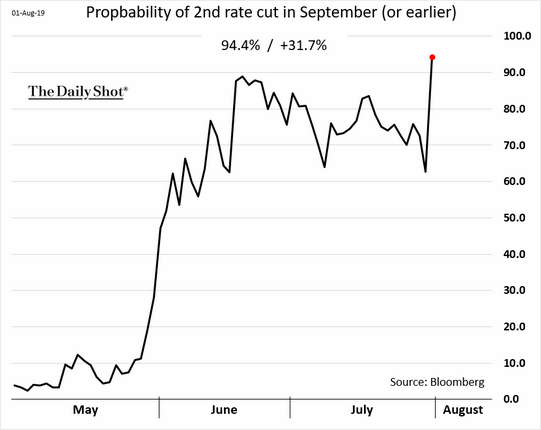

A decent report but markets have moved on. The Fed is perceived to be behind the curve:

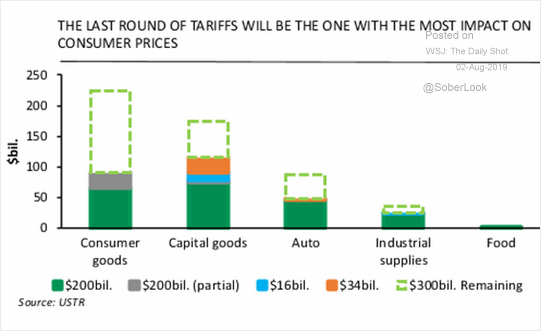

With the trade war raging:

Global growth fading:

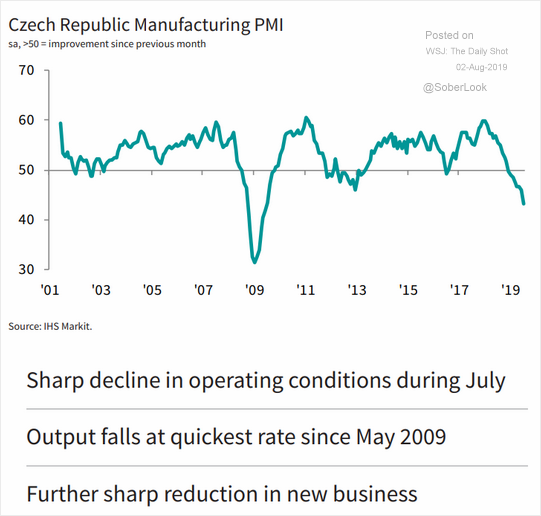

The European recession spreading to the periphery:

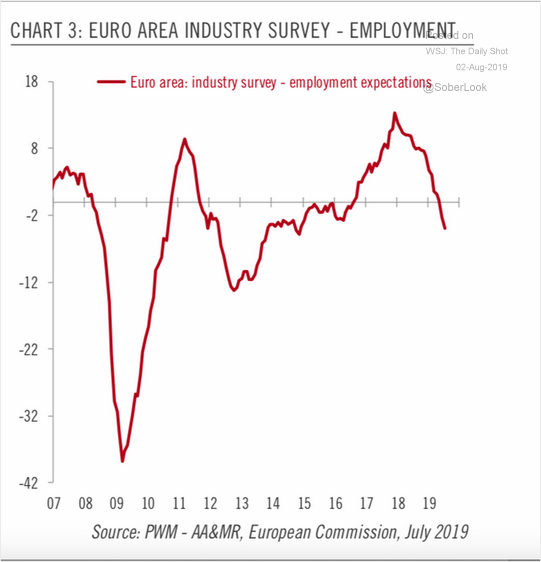

With jobs the next domino to fall:

There’s no end in sight to Australian dollar weakness as the world falls steadily apart.