DXY is till at breakout versus a weak EUR and CNY:

The King Dollar sat on the Australian dollar but it lifted versus other DMs:

EMs were stronger:

It’s BTFD for gold:

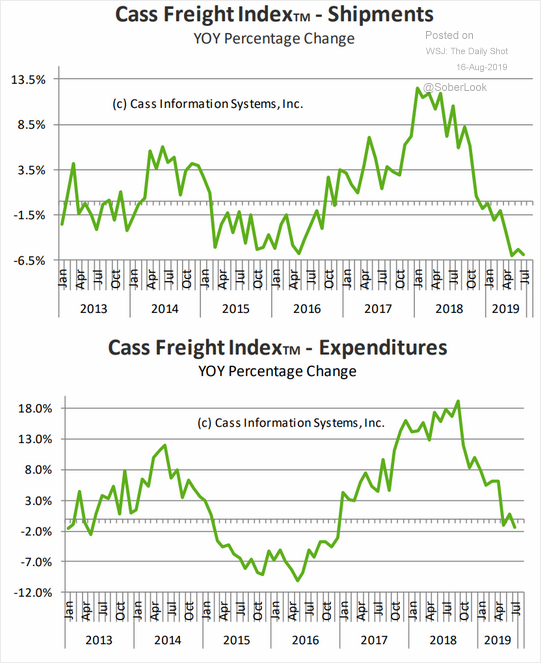

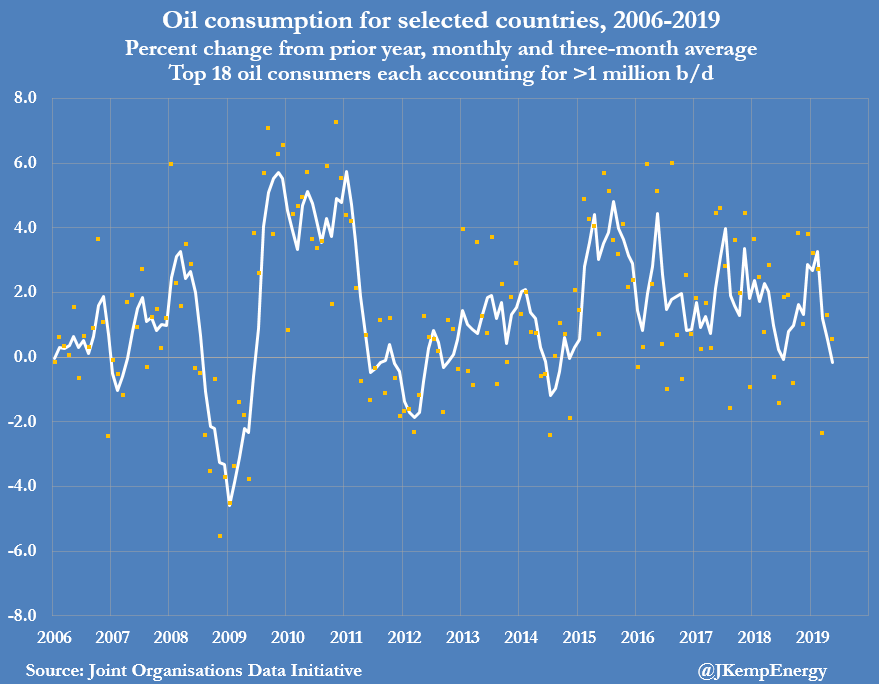

Oil was soft:

Metals mixed:

Miners weak:

EM stocks better:

And junk:

Treasuries were sold:

Bunds more so:

Aussie bonds were solid:

Stocks were strong just because:

The Fed minutes were out and showed no great desire to cut beyond a bit of insurance:

In their discussion of monetary policy decisions at this meeting, those participants who favored a reduction in the target range for the federal funds rate pointed to three broad categories of reasons for supporting that action.

• First, while the overall outlook remained favorable, there had been signs of deceleration in economic activity in recent quarters, particularly in business fixed investment and manufacturing. A pronounced slowing in economic growth in overseas economies—perhaps related in part to developments in, and uncertainties surrounding, international trade—appeared to be an important factor in this deceleration. More generally, such developments were among those that had led most participants over recent quarters to revise down their estimates of the policy rate path that would be appropriate to promote maximum employment and stable prices.

• Second, a policy easing at this meeting would be a prudent step from a risk-management perspective. Despite some encouraging signs over the intermeeting period, many of the risks and uncertainties surrounding the economic outlook that had been a source of concern in June had remained elevated, particularly those associated with the global economic outlook and international trade. On this point, a number of participants observed that policy authorities in many foreign countries had only limited policy space to support aggregate demand should the downside risks to global economic growth be realized.

• Third, there were concerns about the outlook for inflation. A number of participants observed that overall inflation had continued to run below the Committee’s 2 percent objective, as had inflation for items other than food and energy. Several of these participants commented that the fact that wage pressures had remained only moderate despite the low unemployment rate could be a sign that the longer-run normal level of the unemployment rate is appreciably lower than often assumed. Participants discussed indicators for longer-term inflation expectations and inflation compensation. A number of them concluded that the modest increase in market-based measures of inflation compensation over the intermeeting period likely reflected market participants’ expectation of more accommodative monetary policy in the near future; others observed that, while survey measures of inflation expectations were little changed from June, the level of expectations by at least some measures was low. Most participants judged that long-term inflation expectations either were already below the Committee’s 2 percent goal or could decline below the level consistent with that goal should there be a continuation of the pattern of inflation coming in persistently below 2 percent.A couple of participants indicated that they would have preferred a 50 basis point cut in the federal funds rate at this meeting rather than a 25 basis point reduction. They favored a stronger action to better address the stubbornly low inflation rates of the past several years, recognizing that the apparent low sensitivity of inflation to levels of resource utilization meant that a notably stronger real economy might be required to speed the return of inflation to the Committee’s inflation objective.

Several participants favored maintaining the same target range at this meeting, judging that the real economy continued to be in a good place, bolstered by confident consumers, a strong job market, and a low rate of unemployment. These participants acknowledged that there were lingering risks and uncertainties about the global economy in general, and about international trade in particular, but they viewed those risks as having diminished over the intermeeting period. In addition, they viewed the news on inflation over the intermeeting period as consistent with their forecasts that inflation would move up to the Committee’s 2 percent objective at an acceptable pace without an adjustment in policy at this meeting. Finally, a few participants expressed concerns that further monetary accommodation presented a risk to financial stability in certain sectors of the economy or that a reduction in the target range for the federal funds rate at this meeting could be misinterpreted as a negative signal about the state of the economy.

In their discussion of the outlook for monetary policy beyond this meeting, participants generally favored an approach in which policy would be guided by incoming information and its implications for the economic outlook and that avoided any appearance of following a preset course. Most participants viewed a proposed quarter-point policy easing at this meeting as part of a recalibration of the stance of policy, or mid-cycle adjustment, in response to the evolution of the economic outlook over recent months. A number of participants suggested that the nature of many of the risks they judged to be weighing on the economy, and the absence of clarity regarding when those risks might be resolved, highlighted the need for policymakers to remain flexible and focused on the implications of incoming data for the outlook.

No consensus there. More market tantrum needed before it goes any deeper than two cuts. I guess that’s for the future.

To wit, in Europe, via Bloomie:

The French government expects the U.K. to leave the European Union without a withdrawal agreement, an official in President Emmanuel Macron’s office said, meaning the immediate imposition of border controls after Brexit at the end of October.

A so-called no-deal Brexit is now the central scenario for France, the official said. The comments come after British Prime Minister Boris Johnson sent a letter to EU officials demanding the removal of the controversial Irish border backstop from the deal, something the bloc has repeatedly refused to do.

And trade, via CPC foghorn:

As for Washington’s threat to link trade talks with the situation in Hong Kong, what I heard on various occasions is scorn on this idea. China is making arrangements on scenario of no deal. The deterrence of the US not signing the deal on China is close to zero.

— Hu Xijin 胡锡进 (@HuXijin_GT) August 21, 2019

Plus:

And Hong Kong, also at Bloomie:

…the new reality for multinational businesses that have long grappled with a thorny question on China: What’s the price of access to Asia’s biggest economy? Beijing’s response to the protests, most notably its clampdown on Cathay Pacific Airways Ltd. this month, has provided one answer: compliance with the Communist Party’s worldview, from senior management on down.

“The Chinese government doesn’t see business as being separate from the state and it has made it clear that if you want to do business in China, you’d better toe the line,” said Steve Vickers, chief executive officer of political and corporate risk consultancy Steve Vickers & Associates, and the former head of the Royal Hong Kong Police Criminal Intelligence Bureau.

This will only accelerate supply chains exiting China as executives fear for their personal safety.

And oil:

These are my four triggers for a market shakeout:

- trade war worsening;

- Hong Kong end game;

- Brexit, and

- an oil crash triggering US debt stress.

Markets are toying with the idea that enough stimulus on deck to hold growth together but none of my shakeout triggers is improving.

Until they do, the Australian dollar is on a hiding to nothing.