DXY was up last night. So was CNY but not EUR:

The Australian dollar was monstered across DMs:

EMs were even worse:

Gold hit new highs:

Oil was belted:

Metals hit:

Miners slammed:

EM stocks are at the brink:

EM junk is over it:

The Treasury curve cratered:

And bunds:

And Aussie:

Stocks were smashed:

Westpac has the wrap:

Event Wrap

Eurozone July industrial production missed weak expectations on m/m basis (-1.6%m/m, est. -1.5%m/m), but data revisions meant that there was a sharp miss in the annual level at -2.6%y/y (est. -1.5%), with Eurostat citing weak capital goods production and highlighting weak production in Germany. This overshadowed the as expected 2Q Eurozone GDP (+0.2%q/q, +1.1%y/y). However, 2Q employment growth was also weaker on an annual basis (+1.1%y/y, prior +1.3%y/y). National 2Q GDP in Germany (-0.1%q/q as est., +0.4%y/y vs est. +0.1%y/y) and Holland (+0.5%q/q, est. +0.3%q/q), solid French 2Q unemployment data (8.5% vs est. 8.6%) and final CPI for July (unchanged) had minimal market impact.

UK July inflation report was firmer than expected (headline CPI +2.1%y/y, est. 1.9%y/y; core CPI 1.9%y/y, est. 1.8%y/y, RPI as est. at 2.8%y/y) but by remaining close to BoE’s targeted 2% was not seen as disruptive.

FOMC member Bullard saw good macro outcomes for the US, including a near 50-year low on unemployment and low inflation, but wondered whether inflation could get stuck below target, noting Japan’s case where the policy interest rate hasn’t been above 0.5% over the last 20 years and inflation has been low or negative. He cited a range of policy tools, including negative interest rates. There will be little further Fed commentary ahead of next week’s Jackson Hole Symposium, where the topic is “Challenges to Monetary Policy.”

US President Trump again criticised the Fed for keeping interest rates too high: “…Our problem is with the Fed. Raised too much & too fast. Now too slow to cut…”

Event Outlook

Australia: Jul employment is expected to rise 14k and see the unemployment rate hold at 5.2% (note Jun was 5.24% at two decimal places). Westpac is forecasting a 5.3% unemployment rate with a smaller 5k increase in employment. RBA Deputy Governor Debelle speaks on “Risks to the Outlook” at the Risk Australia Conference, Sydney 9 am.

Japan: Jun industrial production data is released.

UK: Jul retail sales are seen to decline 0.2% after a 1.0% increase in Jun.

US: Jul retail sales are expected to rise 0.3% with control group sales up a solid 0.4%. Jul industrial production is anticipated to increase 0.1% following a flat read in Jun. Aug NAHB housing market index is released.

Data was not happy. Europe is at the brink. Industrial production sank 1.6%:

GDP is just holding positive at 0.2% but it’s still deteriorating:

German GDP contracted 0.1%.

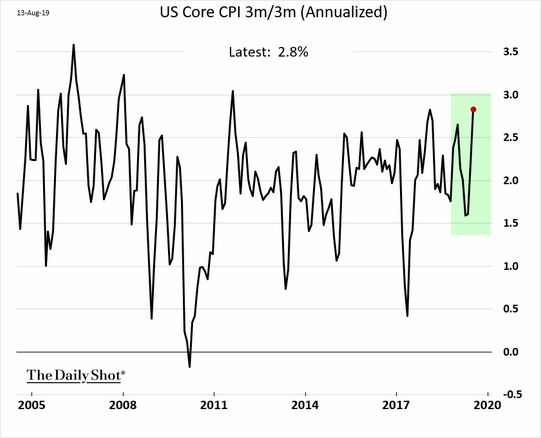

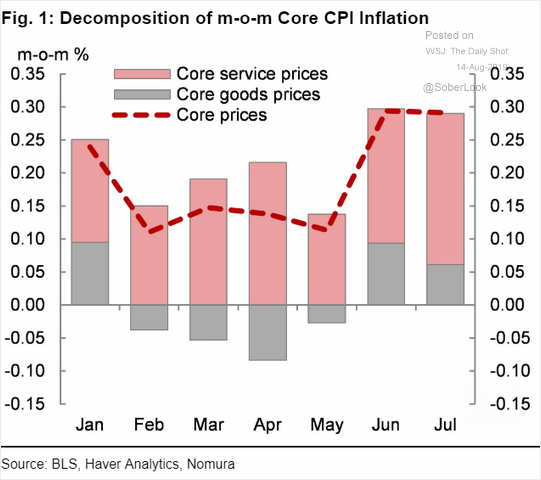

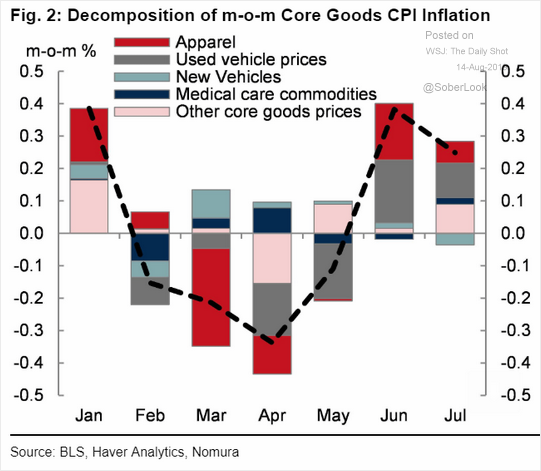

But the bigger issue is the EZ’s comparison with the US where tariff-inspired inflation is warming up.

The source is obvious in tradable goods:

With more to come:

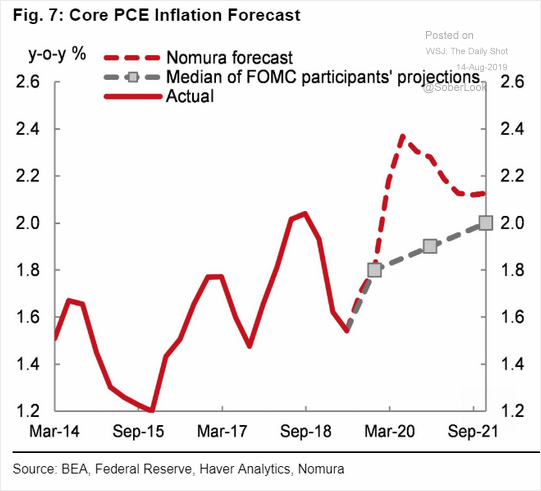

Notionally the Fed can look through this given it ought to be a one off lift, pig in the python style, so long as there is no wage push inflation response. But it’s still enough to spook markets. And the Fed does is in no hurry. Dove James Bullard was sanguine:

Federal Reserve Bank of St. Louis President James Bullard called current U.S. economic conditions “quite good” and said the goal of the central bank’s policy framework review should be to avoid a Japan-style deflationary trap.

“Unemployment is near a 50-year low. Inflation is low and stable,” Bullard said in an audio recording posted on the bank’s website Wednesday. “The economy’s not in recession, so it’s actually a good time to do strategic thinking for the future.”

The review has been underway for months and Bullard will host a Sept. 4 “Fed Listens” event at his bank to get community feedback.

Janet Yellen didn’t help:

Former Federal Reserve Chairman Janet Yellen said the markets may be wrong this time in trusting the yield curve inversion as a recession indicator.

“Historically, it has been a pretty good signal of recession, and it think that’s when markets pay attention to it, but I would really urge that on this occasion it may be a less good signal,” Yellen said on Fox Business Network. “The reason for that is there are a number of factors other than market expectations about the future path of interest rates that are pushing down long-term yields.”

Trump is tearing hair out:

We are winning, big time, against China. Companies & jobs are fleeing. Prices to us have not gone up, and in some cases, have come down. China is not our problem, though Hong Kong is not helping. Our problem is with the Fed. Raised too much & too fast. Now too slow to cut….

— Donald J. Trump (@realDonaldTrump) August 14, 2019

..Spread is way too much as other countries say THANK YOU to clueless Jay Powell and the Federal Reserve. Germany, and many others, are playing the game! CRAZY INVERTED YIELD CURVE! We should easily be reaping big Rewards & Gains, but the Fed is holding us back. We will Win!

— Donald J. Trump (@realDonaldTrump) August 14, 2019

And so the EUR sank and the US dollar rose which, as we know, is pure poison for emerging markets, commodities and global growth, especially in the middle of a Chimerican trade war.

Stocks will need to remind the Fed who is boss with good old fashioned puke.

More downside ahead for the Aussie dollar!