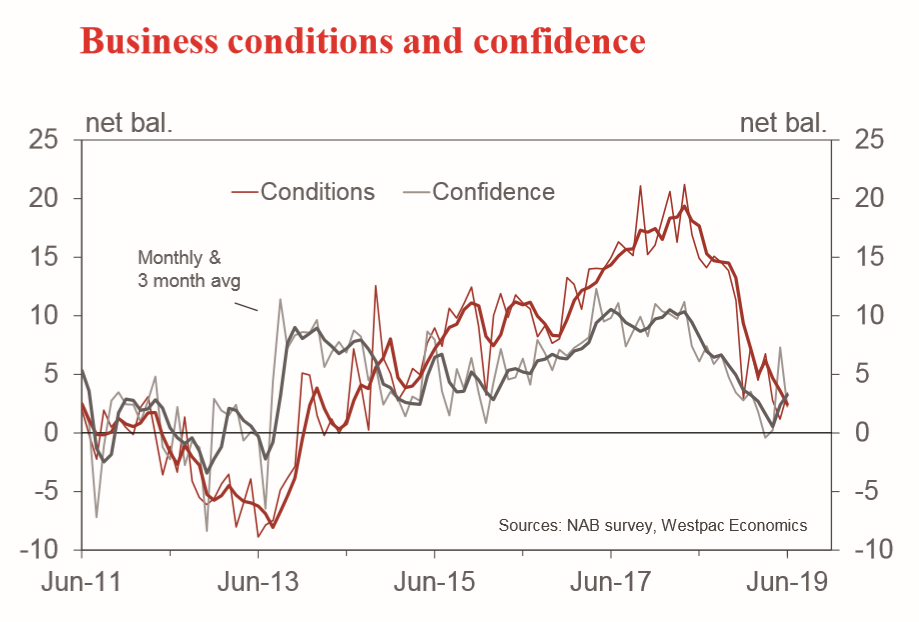

The NAB business survey for June revealed that the spike in business confidence in May (post the Federal election and with the RBA set to cut rates) was a one hit wonder.

The survey was conducted from June 18 to 28. Recall that the previous survey was conducted around the time of the May 18 Federal election (it was sent out on May 14 and interviewing was from May 20 to 24).

Business confidence fell 5pts to +2 in June, a below average reading. This largely reversed the 7pt spike in May.

At the time of the May survey we highlighted that: “The key question, will the jump in confidence be sustained?” The sharp and immediate reversal in confidence highlights that currently the business environment is a challenging one.

The March quarter National Accounts, released on June 5, was another weak report card. It revealed that annual output growth had slowed to the softest pace in a decade, at 1.8%, and that for the past three quarters annualised growth was an anaemic 1.2% annualised.

The business conditions index rose in June, up by 2pts to +3, also a below average reading.

For the June quarter, conditions averaged +2, representing a sharp loss of momentum from the +18 prevailing in mid-2018. The Q2 outcome is the weakest in five years, since mid-2014.

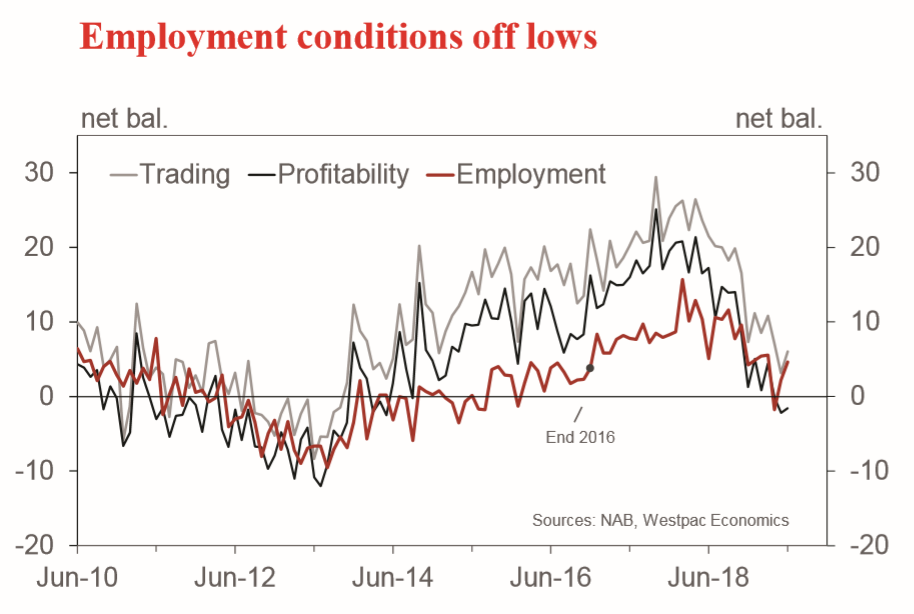

Trading conditions rose by 3pts to +6 and averaged +5 for the quarter, well down from +24 a year earlier. • Profitability is being squeezed in the current sluggish environment, with the index unchanged at -2.

Employment conditions, having slumped to -2 in April, moved a little higher, up 3pts to +5, which is an above average reading for the series.

The survey suggests that the current reading is consistent with near-term job gains of 20k per month – an outcome which would keep the unemployment rate broadly steady (assuming a flat participation rate). We expect jobs growth to slow given recent weakness in activity and in profits.

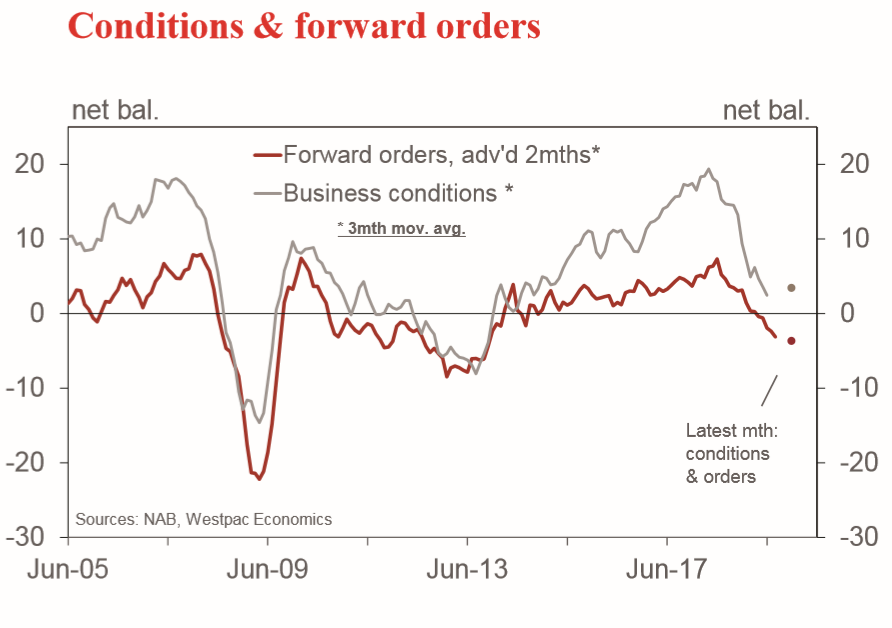

Forward orders were weak, unchanged at -4, suggesting that soft business conditions are likely to persist near-term.

Of interest is whether forward orders will jump in coming months, post the Federal election and with policy stimulus being deployed via RBA interest rate cuts and tax cuts.

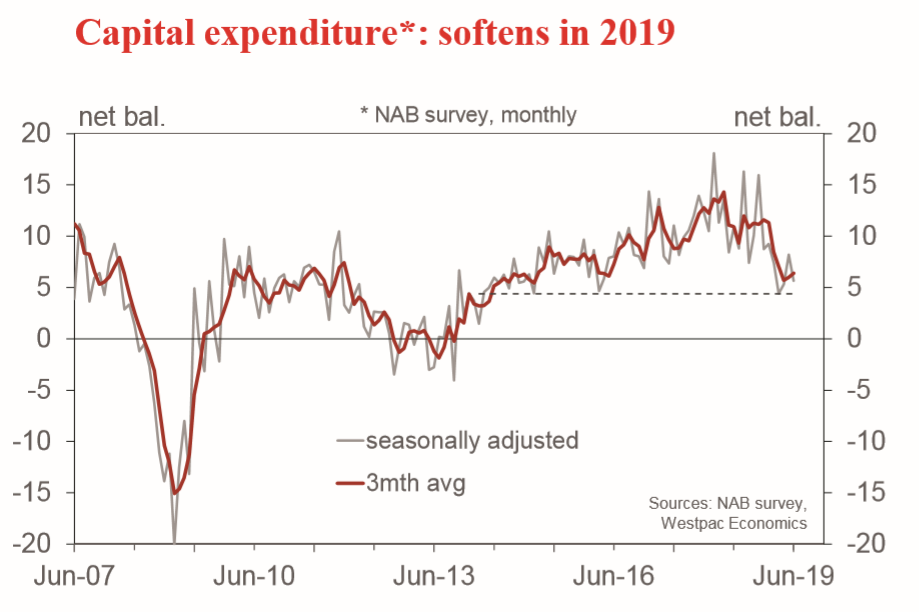

Capital expenditure has trended lower in 2019, as confirmed in the June survey update, see chart overleaf. The capacity utilisation rate jumped in the June survey – a result that appears to be inconsistent with the overall tone of the survey, pointing to the risk that this is reversed.

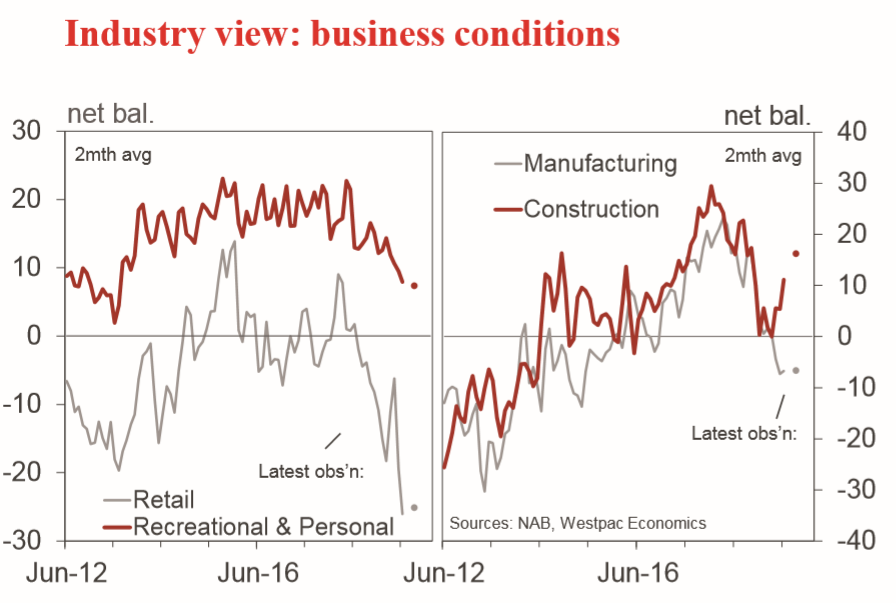

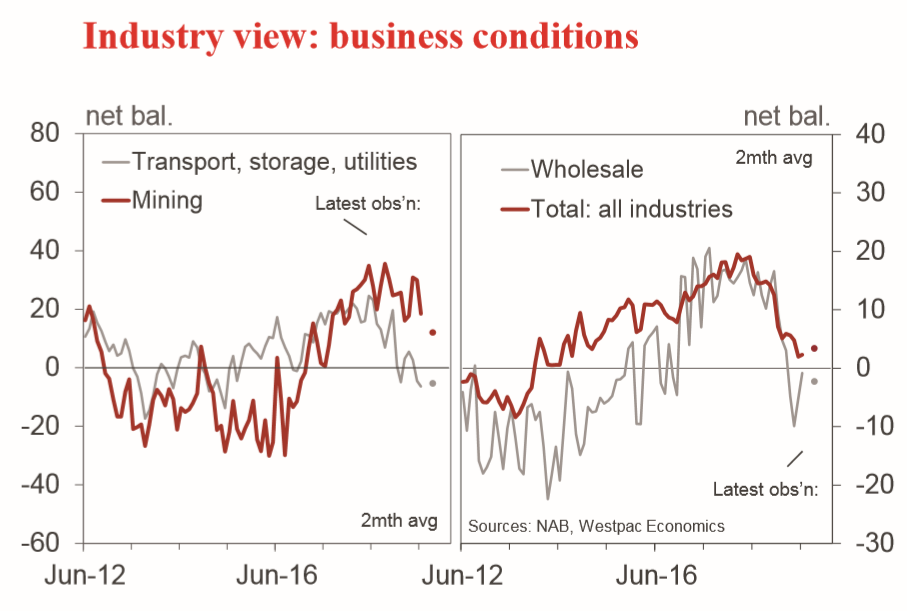

By industry, the trend deterioration in the consumer sectors continues, evidence that households remain under pressure (see chart overleaf). By contrast the ‘finance, property & business segment’ recorded a bounce in conditions as sentiment towards the established housing market improves.

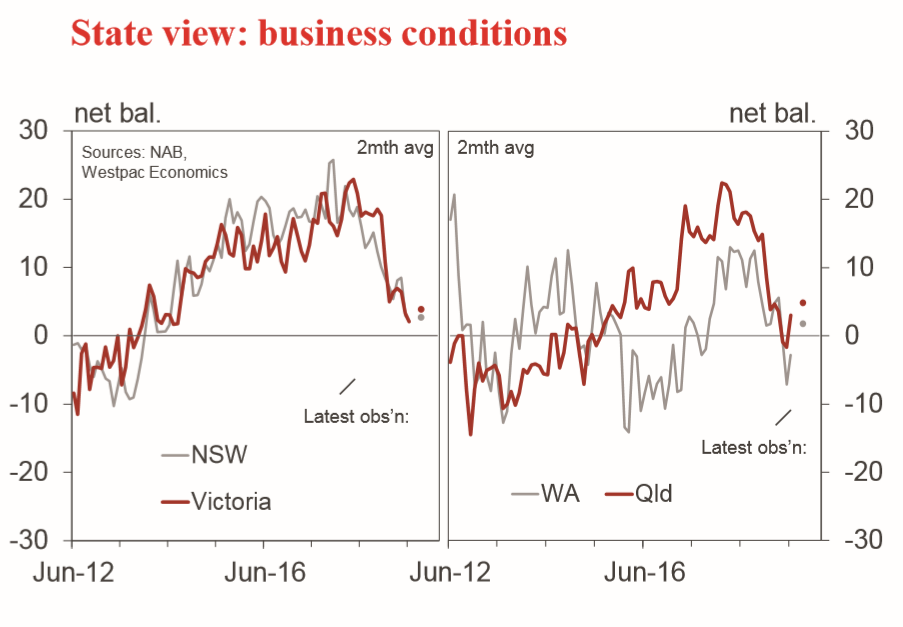

By state, business conditions across NSW and Victoria remained at below average levels, at +3 and +4 respectively, see chart overleaf. The housing downturn, which is set to continue in terms of building work, is having a material impact the two larger states.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.