Advertisement

by Chris Becker

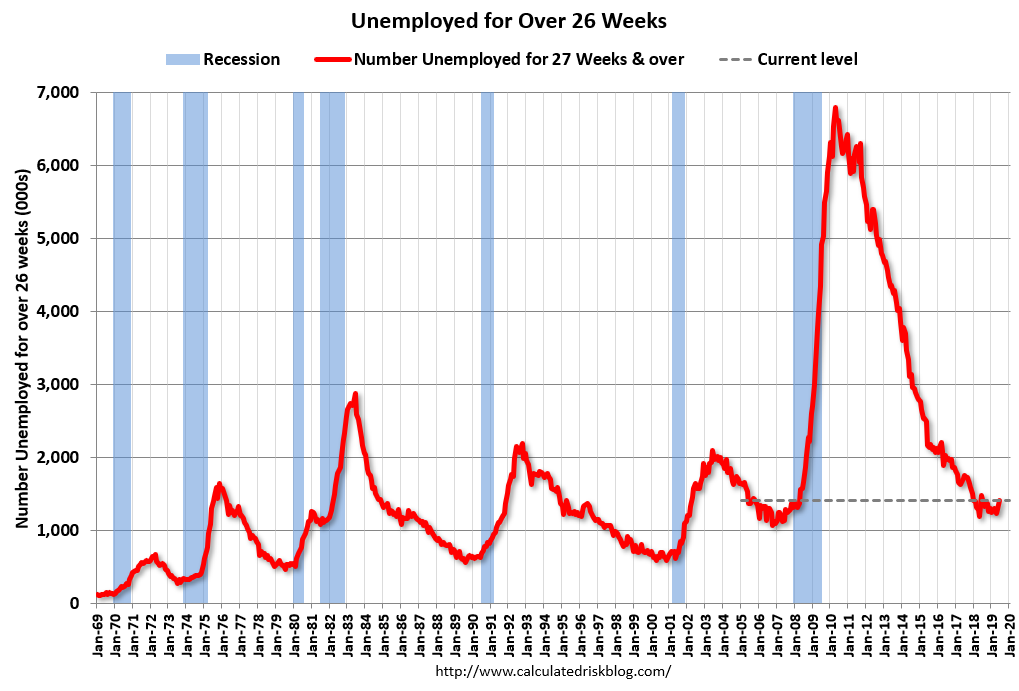

There are three indicators currently weighing on higher probability of a US recession, probably in early 2020. First, buried in Friday night’s unemployment print was the “unemployed for over 26 weeks (6 months) indicator, remaining stuck at a cyclical low:

Interestingly, it has taken large rounds of rate cuts, huge tax cuts and a burgeoning stock market to get to this level, with the recovery phase slowing down once Trump took office in 2016 and bottoming out in this calendar year. With the headline unemployment rate at a record low, there’s no more room to move and as every other cycle since 1968 shows, once this indicator bottoms out, a recession ensues.

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe