The Grattan Institute has slammed the legislated increase in the superannuation guarantee (compulsory superannuation) to 12%, claiming it would rob middle income earners of around $30,000 (1%) of lifetime earnings. From The AFR:

“It’s hard to think of a policy less in the interests of working Australians than higher compulsory super contributions,” said Brendan Coates, the director of Grattan’s household finances program…

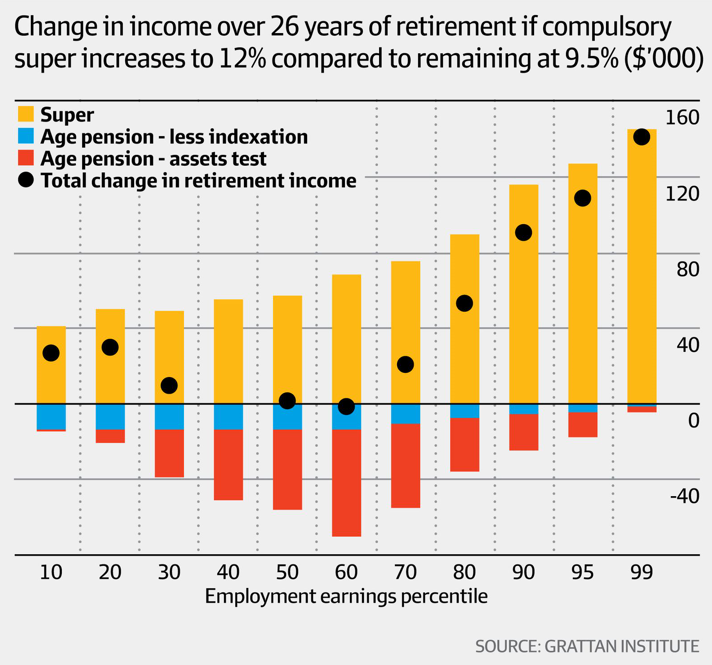

This is because each dollar they have in super will reduce how much they are entitled to receive in government-funded age pension payments.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.