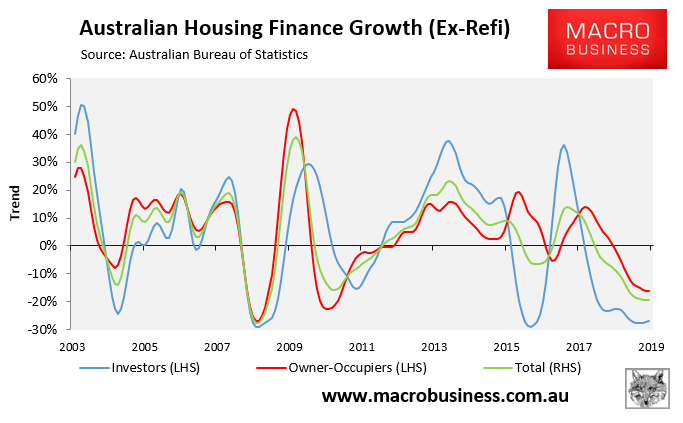

Yesterday’s Lending to households and businesses release from the ABS revealed that total mortgage lending (excluding refinancings) stabilised in May, but have tanked by 19% over the year in trend terms, driven by an epic 27% crash in investor commitments, whereas owner-occupied commitments also fell by 16%: