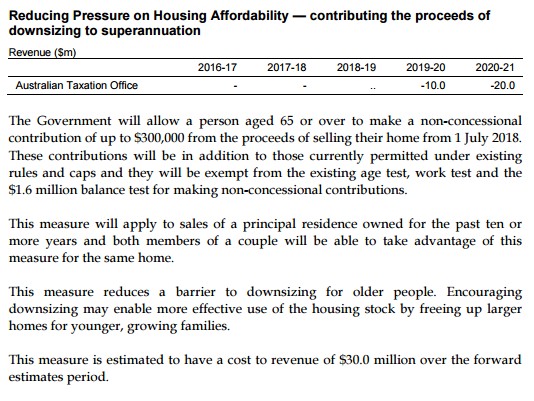

The 2017 Federal Budget included the below measure aimed at encouraging seniors to downsize from their large homes to free-up housing for Australian families:

Yesterday, National Seniors Australia called for the scheme to be expanded to the Aged Pension:

Ian Henschke, chief advocate of National Seniors Australia, suggests: “The strong take-up of this very conditional scheme tells you clearly the demand is there — what needs to happen now is a proper downsizing program that anybody — not just a lucky few — can access”…