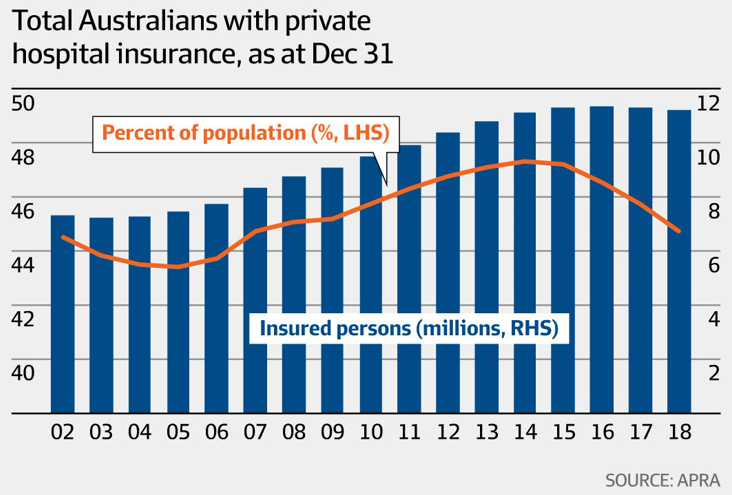

The percentage of Australians aged between 20 and 28 with private health insurance cover for hospitals fell by 6.9% (33,975 people) in 2018, according to data from the Australian Prudential Regulation Authority. The overall percentage of Australians with hospital cover at the end of 2018 was 44.6%, the lowest level since December 2006, whereas the percentage of over-90s with health cover rocketed. From The AFR:

It’s the fourth year in a row that APRA has reported a fall in rates of hospital cover, from its 2014 peak of 47.3 per cent. The rate is now at its lowest level since December 2006.

With the exception of 35 to 39 year olds, the percentage of every cohort up to age 64 with hospital cover fell, with 30 to 34 year olds seeing the second biggest drop, of 3.56 per cent.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.