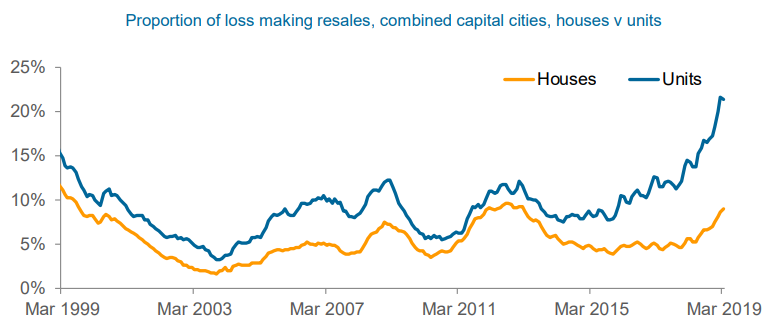

CoreLogic’s has released its latest Pain & Gain Report, which shows that more than one-in-five recent apartment buyers across Australia’s capital cities sold at a loss in the March quarter of 2019 – roughly double the level of three years ago:

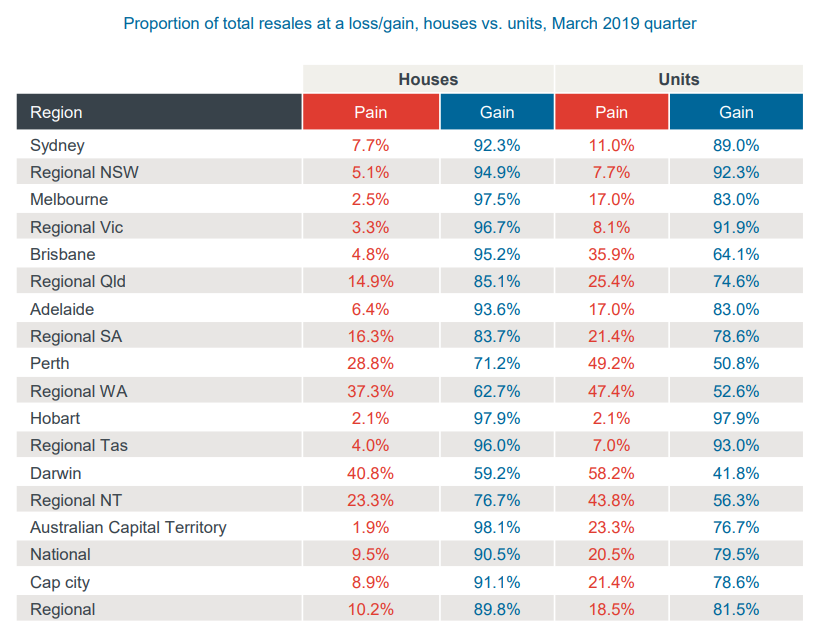

As shown in the below table, all mainland capitals experienced double-digit loss-making apartment sales in March, with Darwin (-58.2%) and Perth (-49.2%) faring worst and Sydney (-11.0%) faring best:

According to CoreLogic:

For capital city units, 78.6% resold at a profit over the quarter with the share down from 81.8% the previous quarter and 85.7% a year earlier. The 78.6% of units resold at a profit was slightly higher than the previous month, but prior to that, it was the lowest share since the 3 months to June 1997. With housing market conditions continuing to weaken since March 2019, we would expect the share of capital city houses and units reselling for a loss to continue rising…

Units sold at a loss over the quarter were typically held by their owners for 6.3 years.

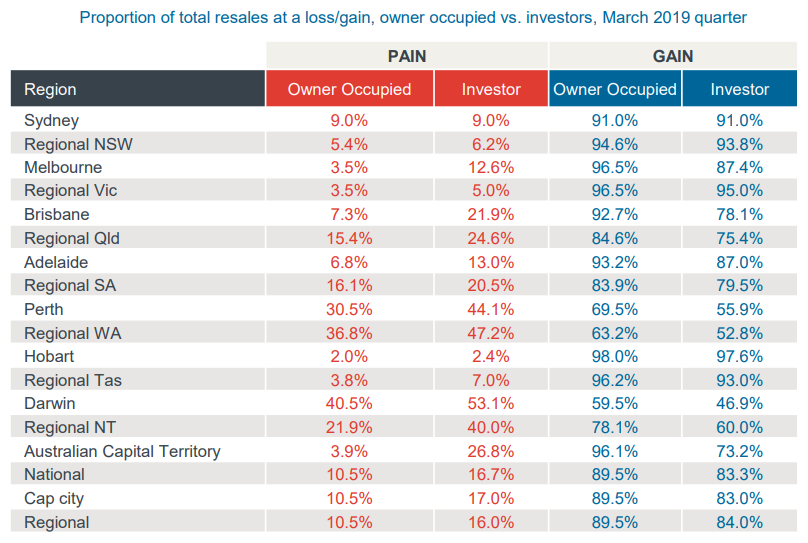

Not surprisingly, given their larger representation in the apartment market, investors experienced sharper losses than owner-occupiers – 17.0% versus 10.5% across the combined capitals in the March quarter:

With concerns around high-rise flammable cladding and structural defects proliferating, the poison of negative equity will likely spread across Australia’s apartment market.

Avoid this segment like the plague.