by Chris Becker

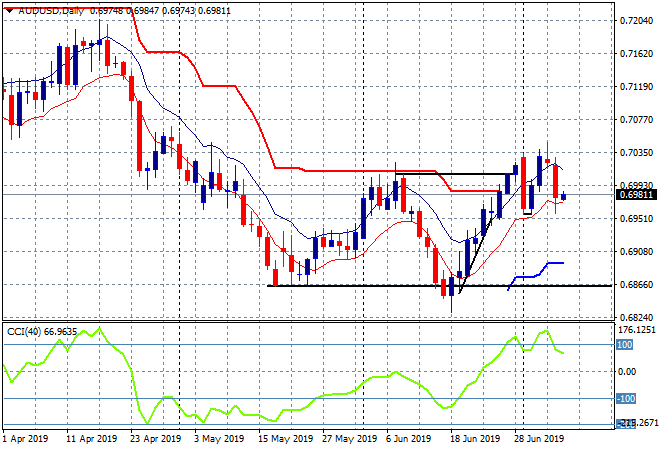

The Australian dollar took a nose dive on the US unemployment print on Friday, with the strong result (224K jobs created vs 164K expected) sending interest rate cut expectations by the Federal Reserve down, thus launching the USD higher against all the undollars.

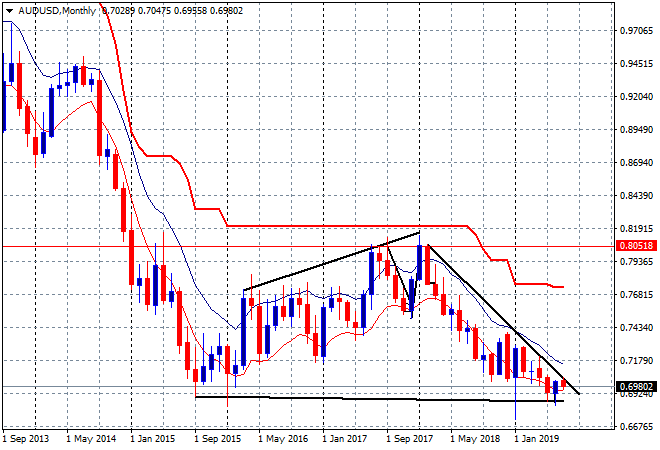

Now is this move just temporary, given the Pacific Peso has been on a tear since bottoming out at 68.50 in early June, as the market priced in the July RBA rate cut?

There is a cluster of daily high and lows since late June around the 70 handle, adding to the chaotic nature of the Aussie dollar, with the nomination of Christine Lagarde as the new head of the increasingly dovish ECB, plus Governor Kurodas firm insistence of keeping the easing handle to the floor at the BOJ not helping the RBA with the currency wars.

In fact, Morgan Stanley remain in a long Aussie bias, giving three reasons why the combined monetary and fiscal reasons both internal and external should keep the Pacific Peso elevated:

- The national banks’ regulator confirming easier mortgage rules (this was on Friday last week) Australia’s weak property market will receive a shot in the arm with lenders being able to use lower buffers for mortgage stress tests in loan assessments, which should allow home buyers to borrow more.

- AU$158bn tax stimulus provided by the Morrison government should also help the economy weather headwinds provided by slowing global trade and implicitly weaker external demand

- Easing mortgage lending rules and a fiscal stimulus should provide some relief for the RBA