By Chris Becker

A stronger than expected 2Q GDP print on Friday night gave US stocks a big goosing, with new record highs, as the USD also put in a two month high with Euro at two year lows against King Dollar. The Fed looks set still to cut rates when it meets tomorrow – around 0.25% is priced in – despite the strong GDP print, which maybe overshadowed by a big week in US earnings reports.

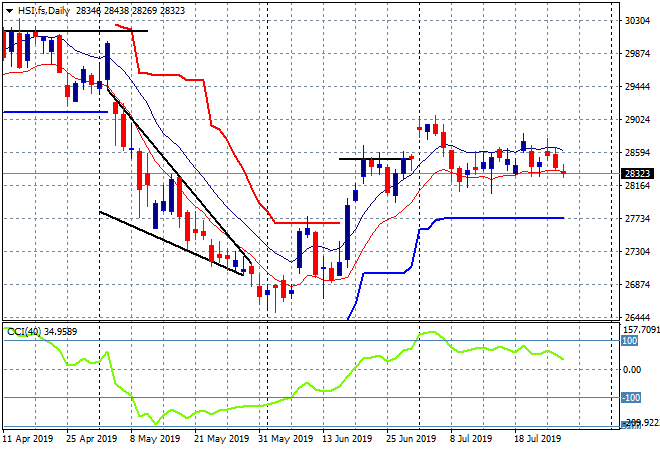

Looking at the action on Asian markets on Friday, where the Shanghai Composite lifted 0.25% but has been unable to finish the week above 3000 points while the Hang Seng Index fell sharply, down 0.7% to 28397 points. This put it back below the recent set of highs at 28500 as the market moves towards a more cautious mood and frustratingly sideways too with very easy to discern breakout and breakdown points at the 28700 and 28100 points respectively: