By Chris Becker

European markets awaited the outcome of the UK Tory leadership and hence new PM outcome with the Euro tanking on the news that “Trump-lite” Johnson got the job, thus securing months of chaos until the end of October. This was overshadowed by positive news around the US-China trade war plus a new deal to raise the debt ceiling by the US Congress. Home sales data from the US was disappointing but that didn’t stop stocks climbing again and it should be a positive mood here in Asia today.

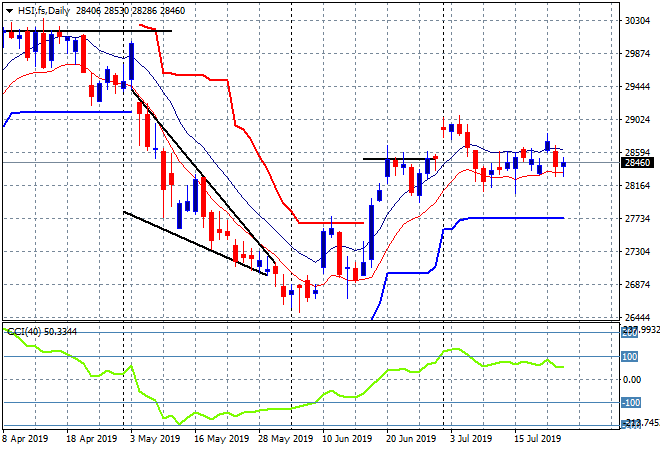

Looking at the action yesterday, where Chinese stocks have come back slightly with the Shanghai Composite lifting 0.4% to exactly 2900 points while the Hang Seng Index is up around 0.3% to 28446 points. This still keeps it just below the recent set of highs at 28500 as the market continues to track sideways here. The recent US/China trade news might give it a push higher in today’s session and momentum is still nominally positive: